#FutureFresenius: Advancing patient care – Strategic course set to unlock full potential – Fresenius enters new era with simplified Group structure and therapy focus across 3 platforms – 2022 performance in line with expectations – 2023 outlook tough but realistic

- Fresenius has hit RESET and is now moving towards #FutureFresenius with a simplified structure, sharper focus and acceleration of performance

- Intention to deconsolidate Fresenius Medical Care by changing the legal form of FMC to a German Stock Corporation (“Aktiengesellschaft”) in simplified governance

- Focus on Operating Companies Fresenius Kabi and Fresenius Helios

- Active portfolio management for assets where Fresenius lacks best ownership

- New, more rigorous Fresenius Financial Framework with ambitious segment margin bands

- ~€1bn annual structural productivity improvement by 2025

- All initiatives pointed towards advancing patient care and becoming an industry-leading, therapy-focused healthcare company

If no timeframe is specified, information refers to Q4/2022.

1 Before special items, Q1/22 restated following remeasurement Humacyte investment

2 Net income attributable to shareholders of Fresenius SE & Co. KGaA

3 Excluding Ivenix and mAbxience acquisitions

For a detailed overview of special items please see the reconciliation tables on pages 22-25.

Fresenius is moving ahead on its pathway to #FutureFresenius. Through the planned deconsolidation of Fresenius Medical Care, the company will simplify its governance and group structure. The company will have a clear focus on therapy to advance patient care across the three platforms (Bio)Pharma, MedTech and Care Provision. Programs are in place to enhance profitability and for active portfolio management. Fresenius will increase the pace of annual structural productivity improvement to approximately 1 billion euros by 2025.

Intention to deconsolidate Fresenius Medical Care

The company plans to deconsolidate Fresenius Medical Care by changing Fresenius Medical Care’s legal form to a German Stock Corporation (“Aktiengesellschaft”). Subject to the necessary shareholder approvals and the registration with the commercial register, the conversion is expected to become effective by the end of the 2023 financial year at the latest. To this end, an Extraordinary General Meeting of Fresenius Medical Care is expected to be held in July to decide on the proposal to change the company into the legal form of an Aktiengesellschaft (“AG”). Following the planned change in its legal form, Fresenius Medical Care will no longer be part of the fully consolidated subsidiaries of Fresenius. Fresenius’ will continue to hold a 32 percent stake in the share capital of Fresenius Medical Care.

“After careful consideration and very constructive discussions with the Group’s key stakeholders, we are confident that the planned deconsolidation of Fresenius Medical Care is the best way forward to benefit both companies.” said Wolfgang Kirsch, Chairman of the Supervisory Board of Fresenius SE. “By converting Fresenius Medical Care to the legal form of an AG, both companies gain flexibility and can better advance their strategic priorities, positioning themselves in the best possible way for the future. Michael Sen and his management team, who have developed this new corporate structure, will lead Fresenius back to operational strength and sustainable growth. I am convinced that the new structure will enable Helen Giza as CEO to realize the full potential of Fresenius Medical Care, in which we continue to hold a significant stake.”

“This is an inflection point for Fresenius”, said Fresenius SE CEO Michael Sen. “I am pleased that our anchor shareholder, the Else Kröner-Fresenius Foundation, has expressed their support for our plans and I would like to thank them for their trust. The new structure will greatly benefit both companies: Fresenius Medical Care needs an operational turnaround, to improve its performance and focus on its core business. Fresenius needs to simplify its complex corporate structures and commit to its Operating Companies and to maximizing value from its investments.”

“Simplifying our governance structure is an important step towards more optionality for a successful future of Fresenius Medical Care”, said Helen Giza, CEO of Fresenius Medical Care. “The new legal form will give us the flexibility and autonomy to focus all our efforts to unlock value as the leading kidney care company.”

Focus on Operating Companies Fresenius Kabi and Fresenius Helios

The Operating Companies Fresenius Kabi and Fresenius Helios are at the center of the Group’s ambitions under #FutureFresenius. They are both geared for significant value creation and catering to system-critical areas of healthcare. Building on a resilient global generics business, Fresenius Kabi will expand along the growth vectors Nutrition, Biopharma and MedTech. Helios Germany and Quirónsalud are already the leading private hospital providers in Germany and Spain, caring for more than 24 million patients every year. Fresenius Helios intends to leverage its market position to actively shape industry trends across digitalization and integrated care.

For the Investment Companies Fresenius Medical Care and Fresenius Vamed, there will be a strong focus on active financial value management. Across the Group, refining the company’s operating model and advancing its ESG agenda and roadmap for the best of patients will be central elements of the further journey towards #FutureFresenius.

~€1bn annual structural productivity improvement by 2025

Structural productivity improvements are moving forward. The new target is to achieve annual structural cost savings of around €1 billion at EBIT level by 2025. In order to reach this goal, Fresenius is running targeted programs across all business segments and the Corporate Center, with the oversight and steering of the Group. Key elements include measures to optimize procurement, processes, sales and administrative costs, as well as divesting from non-core assets.

Thanks to its cost and efficiency program, the company has already realized €152 million in savings after taxes and non-controlling interests in fiscal year 2022, offset by €260 million in one-time costs. In line with previous practice, these expenses are classified as special items.

Fresenius Medical Care has increased the savings target for its FME25 transformation program from €500 million to €650 million by 2025 and now expects to invest up to €650 million in the same period1. By the end of 2022, Fresenius Medical Care delivered €131 million (on EBIT level) of sustainable savings under the FME25 program, exceeding the original target of €40 to 70 million for the same period.

1 Costs related to the FME25 program will be treated as a special item

New, more rigorous Fresenius Financial Framework

To enable and accelerate performance, the Management Board set up a new, more rigorous Fresenius Financial Framework. The framework sets ambitious EBIT margin bands for the segments. They serve as a benchmark when reviewing businesses, measuring performance and planning for the future.

At group level, Fresenius will measure its future performance based on return on invested capital (ROIC), a leverage target band and the cash conversion rate (CCR), among others.

New progressive dividend policy – Stable dividend proposed

With the new Fresenius Financial Framework, Fresenius aims to generate attractive and predictable dividend yields. In line with its new progressive dividend policy, the Company aims to increase the dividend in line with constant currency earnings per share1 growth but at least maintain the dividend at the prior-year’s level. Therefore, the Management Board of Fresenius will propose to the Supervisory Board a stable dividend at the prior year level of €0.92 per share for FY/22 (FY/21: €0.92).

1 Before Special items

FY/23 Group guidance

For 2023, Fresenius expects Group organic revenue1 to grow in a low- to mid-single-digit percentage range. Group constant currency EBIT2 is expected to remain broadly flat or decline up to a high-single-digit percentage rate.

Excluding Fresenius Medical Care constant currency EBIT3 is expected to remain broadly flat or decline up to a mid-single-digit percentage rate.

Fresenius expects the net debt/EBITDA4 ratio to be slightly above the 2022 level by the end of 2023 (December 31, 2022: 3.65x5), depending on divestment activities. The self-imposed target corridor for the leverage ratio remains unchanged at 3.0x to 3.5x.

1 FY/22 base: €40,840 million

2 FY/22 base: €3,727 million, before special items, excl. PRF; FY/23: before special items

3 FY/22 base: €2,187 million, before special items; FY/23: before special items

4 At LTM average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures; excluding further potential acquisitions; before special items; including lease liabilities

5 At LTM average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures; before special items; including lease liabilities

For a detailed overview of special items please see the reconciliation tables on pages 22-25.

Assumptions for guidance FY/23

For 2023, Fresenius assumes no further escalations of geopolitical tensions and challenges from COVID-19, and supply chain constraints continuing to ease.

Fresenius expects that the general cost inflation and labor shortages will have a more significant negative effect on its business than in 2022. This is due to the fact that H2/2022 showed stronger headwinds compared to H1/2022. Thus, Fresenius expects a marked annualization effect.

Fresenius will continue to closely monitor the potential further consequences of the overall heightened volatility and muted visibility, including balance sheet valuations.

For Fresenius Medical Care’s contribution to the Group’s financial figures, the assumptions for Fresenius Medical Care’s FY/23 guidance are also fully applicable to Fresenius Group’s FY/23 guidance. In 2022, Fresenius Medical Care’s EBIT was supported by €277 million of Provider Relief Funding from the U.S. government (at current currency). There is no additional governmental support assumed for 2023.

All of these assumptions are subject to considerable uncertainty.

4% revenue increase in constant currency

Group revenue increased by 7% (4% in constant currency) to €10,643 million (Q4/21: €9,966 million). Organic growth was 3%. Acquisitions/divestitures contributed net 1% to growth. Currency translation increased revenue growth by 3%. Excluding estimated COVID-19 effects1, Group revenue growth would have been 4% to 5% in constant currency (Q4/21: 5% to 6%).

In FY/22, Group revenue increased by 9% (4% in constant currency) to €40,840 million (FY/21: €37,520 million). Organic growth was 3%. Acquisitions/divestitures contributed net 1% to growth. Currency translation increased revenue growth by 5%. Excluding estimated COVID-19 effects1, Group revenue growth would have been 4% to 5% in constant currency (FY/21: 5% to 6%).

16% net income2,3,4 decline in constant currency

Group EBITDA before special items decreased by 2% (-7% in constant currency) to €1,802 million (Q4/212: €1,846 million). Reported Group EBITDA was €1,513 million (Q4/21: €1,868 million).

In FY/22, Group EBITDA before special items decreased by 1% (-6% in constant currency) at €6,808 million (FY/212: €6,854 million). Reported Group EBITDA was €6,294 million (FY/21: €6,825 million).

Group EBIT before special items decreased by 10% (-14% in constant currency) to €1,052 million (Q4/212: €1,166 million). The decrease was mainly driven by ongoing inflation leading to cost increases including personnel costs, material prices, logistics, and energy costs as well as negative one-offs at Fresenius Vamed and Fresenius Kabi. The EBIT margin before special items was 9.9% (Q4/212: 11.7%). Reported Group EBIT was €687 million (Q4/21: €1,123 million).

In FY/22, Group EBIT before special items decreased by 6% (-11% in constant currency) to €4,004 million (FY/212: €4,252 million). The EBIT margin before special items was 9.8% (FY/212: 11.3%). Reported Group EBIT was €3,321 million (FY/21: €4,158 million).

1 For estimated COVID-19 effects please see table on page 20.

2 Before special items

3 Net income attributable to shareholders of Fresenius SE & Co. KGaA

4 Excluding Ivenix and mAbxience acquisitions

For a detailed overview of special items please see the reconciliation tables on pages 22-25.

Group net interest before special items was -€157 million (Q4/211: -€120 million) mainly due to financing activities, rising interest rates and currency translation effects. Reported Group net interest was -€132 million (Q4/21: -€122 million). In FY/22, Group net interest before special items was -€533 million (FY/211: -€504 million). Reported Group net interest was -€507 million (FY/21: -€506 million).

Group tax rate before special items was 24.4% (Q4/21 : 23.2%) mainly due to an increase in the proportionate share of non-tax-deductible expenses compared to taxable income as well as tax law changes at Fresenius Medical Care. Reported Group tax rate was 27.4% (Q4/21: 24.2%). In FY/22, Group tax rate before special items was 23.7% (FY/211: 22.6%) while the reported Group tax rate was 24.8% (FY/2021: 22.8%).

Noncontrolling interests before special items were -€232 million (Q4/211: -€282 million) of which 97% were attributable to the noncontrolling interests in Fresenius Medical Care. Reported noncontrolling interests were -€148 million (Q4/21: -€260 million). In FY/22, Noncontrolling interests before special items were -€918 million (FY/211: -€1,033 million) of which 91% were attributable to the noncontrolling interests in Fresenius Medical Care. Reported noncontrolling interests were -€745 million (FY/21: -1,001 million).

Group net income2 before special items decreased by 15% (-19%/-16% in constant currency) to €445 million (Q4/211: €521 million). The decrease was driven by the challenging macroeconomic environment with increased uncertainties, general cost inflation, staff shortage, disruptions in supply chains, and increased energy costs. Moreover, rising interest costs and negative one-off items at Fresenius Vamed and Fresenius Kabi as well as a higher tax rate weighed on the net income development. Excluding estimated COVID-19 effects4, Group net income2 before special items was -19% to -15% in constant currency (Q4/21: 3% to 7%). Reported Group net income2 decreased to €255 million (Q4/21: €499 million).

In FY/22, Group net income2 before special items decreased by 7% (-12%/-10%3 in constant currency) to €1,729 million (FY/211: €1,867 million). Excluding estimated COVID-19 effects4, Group net income2 before special items was -16% to -12% in constant currency (FY/21: 6% to 10%). Reported Group net income2 decreased to €1,372 million (FY/21: €1,818 million).

1 Before special items

2 Net income attributable to shareholders of Fresenius SE & Co. KGaA

3 Excluding Ivenix and mAbxience acquisitions

4 For estimated COVID-19 effects please see table on page 20

For a detailed overview of special items please see the reconciliation tables on pages 22-25.

Earnings per share1 before special items decreased by 16% (-20% in constant currency) to €0.79 (Q4/21 : €0.94). Reported earnings per share1 were €0.45 (Q4/21: €0.90). In FY/22, earnings per share1 before special items decreased by 8% (-13% in constant currency) to €3.08 (FY/212: €3.35). Reported earnings per share1 were €2.44 (FY/21: €3.26).

1 Net income attributable to shareholders of Fresenius SE & Co. KGaA

2 Before special items

For a detailed overview of special items please see the reconciliation tables on pages 22-25.

Investments

Spending on property, plant and equipment was €713 million corresponding to 7% of revenue (Q4/21: €690 million; 7% of revenue). These investments served primarily for the modernization and expansion of dialysis clinics, production facilities as well as hospitals and day clinics. In FY/22, spending on property, plant and equipment was €1,886 million corresponding to 5% of revenue (FY/21: €2,032 million; 5% of revenue).

Total acquisition spending was €43 million (Q4/21: €278 million) mainly for dialysis clinics at Fresenius Medical Care. In FY/22, total acquisition spending was €1,579 million (FY/21: €1,085 million).

Cash flow development

Group operating cash flow increased to €1,824 million (Q4/21: €1,749 million) with a margin of 17.1% (Q4/21: 17.5%). The strong development was driven by better cash collections and improved working capital management. Free cash flow before acquisitions and dividends increased to €1,219 million (Q4/21: €1,075 million). Free cash flow after acquisitions and dividends increased to €1,107 million (Q4/21: €841 million).

In FY/22, Group operating cash flow decreased to €4,198 million (FY/21: €5,078 million) with a margin of 10.3% (FY/21: 13.5%). The decrease was mainly due to lower net income and higher inventories. Free cash flow before acquisitions and dividends decreased to €2,421 million (FY/21: €3,061 million). Free cash flow after acquisitions and dividends decreased to €701 million (FY/21: €1,193 million).

Solid balance sheet structure

Group total assets increased by 6% (4% in constant currency) to €76,415 million (Dec. 31, 2021: €71,962 million) given currency translation effects, acquisitions and the expansion of business activities. Current assets increased by 5% (4% in constant currency) to €18,279 million (Dec. 31, 2021: €17,461 million), mainly driven by the increase of inventories and other current assets. Non-current assets increased by 7% (4% in constant currency) to €58,136 million (Dec. 31, 2021: €54,501 million).

Total shareholders’ equity increased by 10% (7% in constant currency) to €32,218 million (Dec. 31, 2021: €29,288 million). The equity ratio was 42.2% (Dec. 31, 2021: 40.7%).

Group debt increased by 2% (1% in constant currency) at €27,763 million (Dec. 31, 2021: € 27,155 million). Group net debt increased by 3% (1% in constant currency) to € 25,014 million (Dec. 31, 2021: € 24,391 million).

As of December 31, 2022, the net debt/EBITDA ratio was 3.65x1,2 (Dec. 31, 2021: 3.51x1,2) mainly driven by lower EBITDA contribution as well as acquisition spending. The net debt/EBITDA as of December 31, 2022 excluding the closed acquisition of Ivenix and the completed acquisition of a majority stake in mAbxience was 3.581,2.

1 At LTM average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures

2 Before special items

For a detailed overview of special items please see the reconciliation tables on pages 22-25.

Business Segments

Fresenius Medical Care

(Financial data according to Fresenius Medical Care press release)

Fresenius Medical Care is the world's largest provider of products and services for individuals with renal diseases. As of December 31, 2022, Fresenius Medical Care was treating approximately 345,000 patients in 4,116 dialysis clinics. Along with its core business, the Renal Care Continuum, the company focuses on expanding in complementary areas and in the field of critical care. ,

- Fresenius Medical Care sets strategic focus and accelerates transformation

- Full year earnings in line with expectations: continued impact from higher labor costs and inflationary cost increases

- 2023 expected to be a transition year towards earnings growth recovery in 2024

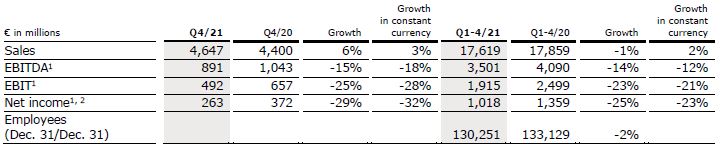

Revenue increased by 8% (2% in constant currency) to €4,997million (Q4/21: €4,647 million). Organic growth was 2%. Currency translation increased revenue growth by 6%. In FY/22, revenue increased by 10% (2% in constant currency) to €19,398 million (FY/21: €17,619 million). Organic growth was 2%. Currency translation increased revenue growth by 8%.

EBIT decreased by 22% (-28% in constant currency) to €352 million (Q4/21: €449 million) resulting in a margin of 7.0% (Q4/21: 9.7%). EBIT before special items increased by 1% (-8% in constant currency) to €495 million (Q4/21: €492 million), resulting in a margin1 of 9.9% (Q4/21: 10.6%). At constant currency, the decline was mainly due to supply chain and labor cost increases across all regions, the impact of U.S. Provider Relief funding from the U.S. government (PRF) received in the previous year’s quarter to compensate for certain COVID-19-related costs, and higher legal costs. This was partially offset by an unfavorable impact from the remeasurement of investments in the previous year and savings related to the FME25 program.

1 Before special items

2 Net income attributable to shareholders of Fresenius Medical Care AG & Co. KGaA

3 For further information, please see Fresenius Medical Care’s press release at www.freseniusmedicalcare.com.

For a detailed overview of special items please see the reconciliation tables on pages 22-25.

In FY/22, EBIT decreased by 18% (-25% in constant currency) to €1,512 million

(FY/21: €1,852 million) resulting in a margin of 7.8% (FY/21: 10.5%). At constant currency, the development was supported by €246 million (FY 2021: €63 million) of PRF to compensate for certain COVID-19-related costs. EBIT before special items decreased by 5% (-13% in constant currency) to €1,817 million (FY/21: €1,915 million), resulting in a margin of 9.4% (FY/21: 10.9 %).

Net income2 decreased by 39% (-47% in constant currency) to €139 million (Q4/21: €228 million). Net income2 before special items decreased by 4% (-14% in constant currency) to €253 million (Q4/21: €263 million). Besides the above-mentioned effects on operating income, the constant currency decline was mainly due to an increase in the proportionate share of non-tax-deductible expenses compared to taxable income as well as tax law changes.

In FY/22, net income2 decreased by 31% (-37% in constant currency) to €673 million (FY/21: €969 million). Net income2 before special items decreased by 10%

(-17% in constant currency) to €913 million (FY/21: €1,018 million).

Operating cash flow was €600 million (Q4/21: €669 million) with a margin of 12.0% (Q4/21: 14.4%). The decrease was mainly due to lower net income. In FY/22, operating cash flow was €2,167 million (FY/21: €2,489 million) with a margin of 11.2%

(FY/21: 14.1%).

For FY/23, Fresenius Medical Care expects revenue3 to grow at a low to mid-single digit percentage rate. In 2022, EBIT was supported by €277 million of PRF (at current currency). There is no additional governmental support assumed for 2023. To provide a comparable basis for the 2023 earnings outlook, the 2022 basis4 is adjusted accordingly. On this basis, EBIT is expected to remain flat or decline by up to a high single-digit percentage rate in 2023. In 2025, Fresenius Medical Care targets to achieve an improved operating income margin of 10-14%. Revenue and operating income, as referred to in the outlook, are both on a constant currency basis and excluding special items.

For further information, please see Fresenius Medical Care’s press release at www.freseniusmedicalcare.com.

1 Before special items

2 Net income attributable to shareholders of Fresenius Medical Care AG & Co. KGaA

3 FY/22 base: €19,398 million

4 FY/22 base: €1,540 million

Fresenius Kabi

Fresenius Kabi offers intravenously administered generic drugs, clinical nutrition and infusion therapies for seriously and chronically ill patients in the hospital and outpatient environments. The company is also a leading supplier of medical devices and transfusion technology products. In the biosimilars business, Fresenius Kabi develops products with a focus on oncology and autoimmune diseases.

- Strong organic revenue growth

- Biopharmaceuticals with continued dynamic growth trajectory

- EBIT impacted by a non-cash one time item related to in-process R&D in North America

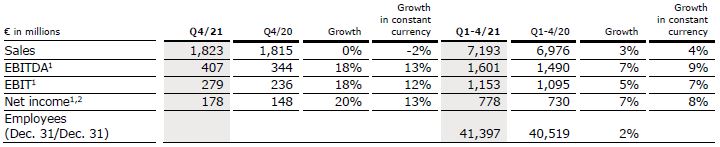

Revenue increased by 12% (8% in constant currency) to €2,036 million (Q4/21: €1,823 million). Organic growth was 7%. In FY/22, revenue increased by 9% (4% in constant currency) to €7,850 million (FY/21: €7,193 million). Organic growth was 3%. Positive currency translation effects of 4% in Q4/22 and 5% in FY/22 were mainly related to the U.S. dollar.

Revenue in North America increased by 14% (organic growth: 3%) to €669 million (Q4/21: €589 million). The significant revenue growth was mainly driven by positive currency translation effects and a solid development of the regular business. In FY/22, revenue in North America increased by 12% (organic growth: 0%) to €2,522 million (FY/21: €2,258 million).

Revenue in Europe increased by 9% (organic growth: 6%) to €724 million (Q4/21: €664 million) driven by a broad-based positive development, in particular at biopharmaceuticals. In FY/22, revenue in Europe increased by 6% (organic growth: 5%) to €2,691 million (FY/21: €2,544 million).

1 Before special items

2 Net income attributable to shareholders of Fresenius SE & Co. KGaA

3 Excluding Ivenix and mAbxience acquisitions

For a detailed overview of special items please see the reconciliation tables on pages 22-25.

Revenue in Asia-Pacific decreased by 2% (organic growth: -2%) to €389 million (Q4/21: €395 million). Organic growth was affected by COVID lockdowns and associated lower patient demand as well as price pressure from the NVBP (National Volume-Based Procurement) tenders in China. In FY/22, revenue in Asia-Pacific increased by 4% (organic growth: -2%) to €1,714 million (FY/21: €1,643 million).

Revenue in Latin America/Africa increased by 45% (organic growth: 41%) to €254 million (Q4/21: €175 million), due to a positive business development in both regions. In addition, the revenue development was positively impacted by hyperinflation in Brazil and Mexico. In FY/22, revenue in Latin America/Africa increased by 23% (organic growth: 18%) to €923 million (FY/21: €748 million).

Revenue in the Biopharmaceuticals business was €72 million. In FY/22, revenue in the Biopharmaceuticals business was €188 million (FY/21: €62 million).

EBIT1 decreased by 15% (-19%/-13% in constant currency) to €236 million (Q4/21: €279 million). EBIT development was impacted by non-cash one-time write offs, primarily related to a capitalized in-process R&D project in North America. Moreover, ongoing macroeconomic headwinds including inflationary cost increases, staff shortages and disrupted supply chains impacted the EBIT performance. In China COVID lockdowns and associated lower patient demand as well as price declines in connection with NVBP tenders weighed on profitability.

EBIT margin1 was 11.6% (Q4/21: 15.3%). Excluding the acquisitions of Ivenix and the majority stake in mAbxience, the constant currency EBIT margin1 was at 12.7%2 in Q4/22. In FY/22, EBIT1 decreased by 6% (-14%/-10%2 in constant currency) to €1,080 million (FY/21: €1,153 million) with an EBIT margin1 of 13.8%/14.4%2 (FY/21: 16.0%).

Net income1,3 increased by 16% (10% in constant currency) to €206 million (Q4/21: €178 million). In FY/22, net income1,3 remained stable (declined by -7% in constant currency) at €780 million (FY/21: €778 million).

1 Before special items

2 Excluding Ivenix and mAbxience acquisitions

3 Net income attributable to shareholders of Fresenius SE & Co. KGaA

For a detailed overview of special items please see the reconciliation tables on pages 22-25.

Operating cash flow decreased to €298 million (Q4/21: €335 million) with a margin of 14.6% (Q4/21: 18.4%) mainly driven by lower net income and higher inventories. In FY/22, operating cash flow decreased to €841 million (FY/21: €1,203 million) with a margin of 10.7% (FY/21: 16.7%).

For FY/23, Fresenius Kabi expects organic revenue1 growth in a low- to mid-single-digit percentage range. The EBIT margin2 is expected to be around one percentage point (pp) below the structural margin band of 14% to 17%.

1 FY/22 base: €7,850 million

2 FY/22 base: EBIT margin: 13.8%, before special items; FY/23 before special items

For a detailed overview of special items please see the reconciliation tables on pages 22-25.

Fresenius Helios

Fresenius Helios is Europe's leading private hospital operator. The company comprises Helios Germany, Helios Spain and Helios Fertility. Helios Germany operates 87 hospitals, around 240 outpatient centers, 21 occupational health centers and 6 prevention centers. Helios Spain operates 50 hospitals, around 100 outpatient centers and around 300 occupational risk prevention centers. In addition, the company is active in Latin America with 8 hospitals and as a provider of medical diagnostics. Helios Fertility offers a wide spectrum of state-of-the-art services in the field of fertility treatments.

- Fresenius Helios with strong organic revenue growth and healthy EBIT development

- Helios Germany with a return to a pre-COVID patient structure by year-end

- Helios Spain with very strong and consistent patient demand

- Helios Fertility with lower volumes driven by delayed treatments

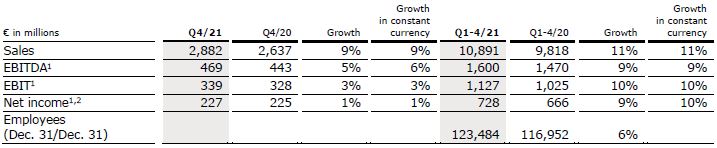

Revenue increased by 5% (5% in constant currency) to €3,031 million (Q4/21: €2,882 million). Organic growth was 5%. Acquisitions at Helios Spain and Helios Fertility contributed 1% to revenue growth. Divestments reduced revenue by 1%. In FY/22, revenue increased by 8% (7% in constant currency) to €11,716 million (FY/21: €10,891 million). Organic growth was 6%. Acquisitions contributed 2% to revenue growth. Divestments reduced revenue by 1%.

Revenue of Helios Germany was flat (organic growth: 0%) to €1,749 million (Q4/21: €1,745 million), mainly driven by increasing admissions and a return to a pre-COVID patient structure by year-end. In FY/22, revenue of Helios Germany increased by 4% (organic growth: 4%) to €7,021 million (FY/21: €6,733 million.

Revenue of Helios Spain increased by 12% (12% in constant currency) to €1,214 million (Q4/21: €1,084 million). Organic growth of 12% was driven by very strong and consistent patient demand. The clinics in Latin America also showed a good performance. In FY/22, revenue of Helios Spain increased by 10% (10% in constant currency) to €4,441 million (FY/21: €4,021 million). Organic growth was 9%.

Revenue of the Helios Fertility were €66 million (Q4/21: €51 million). In FY/22, revenue of the Helios Fertility were €250 million (FY/21: €133 million).

1 Before special items

2 Net income attributable to shareholders of Fresenius SE & Co. KGaA

For a detailed overview of special items please see the reconciliation tables on pages 22-25.

EBIT1 increased by 4% (5% in constant currency) at €354 million (Q4/21: €339 million) with an EBIT margin1 of 11.7% (Q4/21: 11.8%). In FY/22, EBIT1 increased by 5% (5% in constant currency) to €1,185 million (FY/21: 1,127 million) with an EBIT margin1 of 10.1% (FY/21: 10.3%).

EBIT1 of Helios Germany increased by 2% to €174 million (Q4/21: €171 million) with an EBIT margin1 of 9.9% (Q4/21: 9.8%). The increase of costs from the use of external staff mainly due to flu-related staff absenteeism continued to weigh on profitability. Inflationary cost effects had also a negative impact. In FY/22, EBIT1 of Helios Germany increased by 2% to €623 million (FY/21: €613 million) with an EBIT margin1 of 8.9% (FY/21: 9.1%).

EBIT1 of Helios Spain increased due to the strong revenue growth and despite cost inflation by 6% (7% in constant currency) to €172 million (Q4/21: €162 million). The EBIT margin1 was 14.2% (Q4/21: 14.9%). In FY/22, EBIT1 of Helios Spain increased by 8% (8% in constant currency) to €556 million (FY/21: €514 million). The EBIT margin1 was 12.5% (FY/21: 12.8%).

EBIT1 of Helios Fertility was €6 million (Q4/21: €5 million) with an EBIT margin1 of 9.1% (Q4/21: 9.8%). Lower volumes by delayed treatments driven by macroeconomic environment. In FY/22, EBIT1 of Helios Fertility was €21 million (FY/21: €19 million) with an EBIT margin1 of 8.4% (FY/21: 14.3%).

Net income1,2 increased by 4% (4% in constant currency) to €236 million (Q4/21: €227 million). In FY/22, net income1,2 increased by 5% (5% in constant currency) to €766 million (FY/21: €728 million).

Operating cash flow increased to €956 million (Q4/21: €609 million) with a margin of 31.5% (Q4/21: 21.1%) mainly due to an improved receivables management. In FY/22, operating cash flow increased to €1,367 million (FY/21: €1,204 million) with a margin of 11.7% (FY/21: 11,1%)

For FY/23, Fresenius Helios expects organic revenue growth in a mid-single-digit percentage range. The EBIT margin is expected to be within the structural margin band of 9% to 11%.

1 Before special items

2 Net income attributable to shareholders of Fresenius SE & Co. KGaA

3 FY/22 base: €11,716 million

4 FY/22 base: EBIT margin: 10.1%, before special items, FY/23 before special items

For a detailed overview of special items please see the reconciliation tables on pages 22-25.

Fresenius Vamed

Fresenius Vamed manages projects and provides services for hospitals and other health care facilities worldwide and is a leading post-acute care provider in Central Europe. The portfolio ranges along the entire value chain: from project development, planning, and turnkey construction, via maintenance and technical management to total operational management.

- Service business showing solid top-line performance, but one-time items and macro headwinds impact profitability

- Weak top-line performance driven by difficult economic environment and negative one-time items adversely impact earnings in project business

- Macro environment leading to negative one-time effects: Impairments due to reassessment and revaluation of claims and legal proceedings as well as certain business initiations that did not materialize as planned

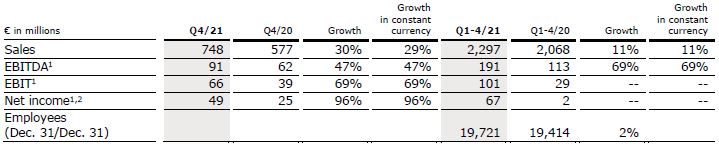

Revenue decreased by 5% (-5% in constant currency) to €712 million (Q4/21: €748 million). Organic growth was -5%. In FY/22, revenue increased by 3% (2% in constant currency) to €2,359 million (FY/21: €2,297 million). Organic growth was 2%.

Revenue in the service business increased by 7% (7% in constant currency) to €445 million (Q4/21: €415 million) due to increasing rehabilitation treatments given fewer capacity restrictions. Revenue in the project business decreased by 20% (-20% in constant currency) to €267 million (Q4/21: €333 million. The weak revenue performance is mainly attributable to the continuing difficult macroeconomic environment. In FY/22, revenue in the service business increased by 7% (6% in constant currency) to €1,685 million (FY/21: €1,580 million). Revenue in the project business decreased by 6% (-6% in constant currency) to €674 million (FY/21: €717 million).

1 Before special items

2 Net income attributable to shareholders of VAMED AG

For a detailed overview of special items please see the reconciliation tables on pages 22-25.

EBIT1 decreased by 114% to -€9 million (Q4/21: €66 million) with an EBIT margin1 of -1.3% (Q4/21: 8.8%). Main driver for the weak development is the macroeconomic backdrop which led to a lower than expected revenue development in the project business and to significant negative one-time effects in the form of impairments due to a reassessment and revaluation of claims and legal proceedings as well as certain business initiations that did not materialize as planned. In FY/22, EBIT1 decreased by 80% to €20 million (FY/21: €101 million) with an EBIT margin1 of 0.8% (FY/21: 4.4%).

Net income1,2 decreased by 129% to -€14 million (Q4/21: €49 million). In FY/22, Net income1,2 decreased by 99% to €1 million (FY/21: €67 million).

Order intake was €572 million (Q4/21: €319 million). In FY/22 order intake was €1,241 million (FY/21: €1,290 million). As of December 31, 2022, order backlog was at €3,689 million (December 31, 2021: €3,473 million).

Operating cash flow decreased to €12 million (Q4/21: €128 million) with a margin of 1.7% (Q4/21: 17.1%), due to higher receivables and payed traded acoounts payable. In FY/22, operating cash flow decreased to -€44 million (FY/21: €151 million) with a margin of -1.9% (FY/21: 6.6%).

For FY/2023, Fresenius Vamed expects organic revenue to grow in a low-to mid-single digit percentage range. The EBIT margin is expected to be clearly below the structural margin band of 4% to 6%.

1 Before special items

2 Net income attributable to shareholders of VAMED AG

3 FY/22 base: €2,359 million

4 FY/22 base: EBIT margin: 0.8%, before special items; FY/23 before special items

For a detailed overview of special items please see the reconciliation tables on pages 22-25.

For additional information on the performance indicators used please refer to our website https://www.fresenius.com/alternative-performance-measures.

This release contains forward-looking statements that are subject to various risks and uncertainties. Future results could differ materially from those described in these forward-looking statements due to certain factors, e.g. changes in business, economic and competitive conditions, regulatory reforms, results of clinical trials, foreign exchange rate fluctuations, uncertainties in litigation or investigative proceedings, the availability of financing and unforeseen impacts of international conflicts. Fresenius does not undertake any responsibility to update the forward-looking statements in this release.

- Healthy organic sales growth and ongoing margin pressure

- Fresenius Medical Care’s business development impacted by delayed effects from improvements in North American Services business in challenging environment

- Fresenius Kabi with healthy sales growth and sequential improvement

- Fresenius Helios with strong organic sales growth, solid EBIT in line with usual third quarter seasonality

- Fresenius Vamed impacted by macroeconomic headwinds and COVID-19

If no timeframe is specified, information refers to Q3/2022.

1 Before special items, Q1/22 restated following remeasurement Humacyte investment

2 Net income attributable to shareholders of Fresenius SE & Co. KGaA

3 Excluding Ivenix and mAbxience acquisitions

For a detailed overview of special items please see the reconciliation tables on pages 22-25 in the PDF.

Michael Sen, CEO of Fresenius said, “Over the past month, I’ve met with many of my Fresenius colleagues. Like me, they have tremendous passion and commitment to patients, physicians and health care professionals. What we do is life-saving.”

Sen continued, “Everyone at Fresenius knows we must improve on what we do. My priorities are clear: Reset the company aiming at becoming a stronger company and delivering value for our shareholders. Our businesses are growing yet in a more challenging environment. Now we sharpen our focus on structural productivity. More fundamentally, we have embarked on a top-to-bottom review of every business activity, looking at the entire corporate portfolio. The focus is on returns. This will not happen overnight, but we will move at a faster pace and more decisively than ever before. This will benefit all our stakeholders. This is #FutureFresenius.”

Sen concluded, “Fresenius is a strong company, with great products, great market positions. Now we have to make it stronger.”

FY/22 Group guidance

Since Fresenius Medical Care continues to operate in a challenging environment, the impacts of the Company’s focused efforts to improve North American Health Care Services operations are delayed against previous assumptions. Therefore, Fresenius Medical Care now assumes lower contributions in the financial year 2022.

Consequently, Fresenius Medical Care now expects net income (attributable to shareholders of Fresenius Medical Care AG & Co. KGaA) for the financial year 2022 to decline in the high teens to mid-twenties percentage range. The Company continues to anticipate revenue to grow at a low-single digit percentage range in the financial year 2022. These targets are in constant currency and exclude special items.

All other business segments of the Fresenius Group, in particular Vamed, are also affected by a challenging overall economic environment. Thus, there are increased uncertainties, inflation-related cost increases, staff shortages, disruptions in supply chains, and increased energy costs. This has a direct impact on customer and patient behavior.

However, as a consequence of the development at Fresenius Medical Care, Fresenius Vamed, and in view of increasing indications of a persistent unfavorable development of these and other factors for the further course of the financial year, the Management Board has changed its risk assessment and consequently also adjusted the Group outlook for FY/22.

At constant currency, the Company now anticipates Group net income1,2 to decline around ten percent (previously: decline in a low-to-mid single-digit percentage range). Group sales3 in constant currency continue to be expected to grow in a low-to-mid single-digit percentage range.

Without the closed acquisition of Ivenix and the completed acquisition of a majority stake in mAbxience as well as any further potential acquisitions, Fresenius expects the net debt/EBITDA4 ratio to be roughly on the same level as in Q3/22 (3.64x5) by the end of 2022 (December 31, 2021: 3.51x5).

1 Net income attributable to shareholders of Fresenius SE & Co. KGaA

2 FY/21 base: €1,867 million, before special items; FY/22: before special items

3 FY/21 base: €37,520 million

4 At LTM average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures; excluding further potential acquisitions; before special items; including lease liabilities

5 At LTM average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures;

before special items; including lease liabilities

For a detailed overview of special items please see the reconciliation tables on pages 22-25 in the PDF.

Assumptions for guidance FY/22

For 2022 and beyond, Fresenius expects that the current challenging market environment and the global macro-economic headwinds will remain. In particular, the general cost inflation, labor shortages, meaningful uncertainty with regard to the future development of energy prices, burdens from supply chain disruptions and ongoing impacts of the COVID-19 pandemic are expected to continue. The guidance does not consider a significant disruption of gas or electricity supplies in Europe.

Fresenius will continue to closely monitor the potential further consequences of the overall heightened volatility and muted visibility, including balance sheet valuations.

The war in Ukraine is directly and indirectly affecting Fresenius Group operations. The direct adverse effects of the war amounted to €24 million at net income1 level of Fresenius Group in Q1-3/22 and are treated as a special item.

An unlikely but possible significant deterioration of the situation triggering containment measures that could have a significant and direct impact on the health care sector without any appropriate compensation is not reflected in the Group’s FY/22 guidance.

For Fresenius Medical Care‘s contribution to the Group’s financial figures, the assumptions for Fresenius Medical Care's FY/22 guidance are also fully applicable to Fresenius Group's FY/22 guidance.

All of these assumptions are subject to considerable uncertainty.

The acquisitions of Ivenix and of the majority stake in mAbxience as well as any further potential acquisitions remain excluded from guidance.

1 Net income attributable to shareholders of Fresenius SE & Co. KGaA

5% sales increase in constant currency

Group sales increased by 12% (5% in constant currency) to €10,459 million (Q3/21: €9,324 million). Organic growth was 4%. Acquisitions/divestitures contributed net 1% to growth. Currency translation increased sales growth by 7%. Excluding estimated COVID-19 effects1, Group sales growth would have been 4% to 5% in constant currency (Q3/21: 7% to 8%).

In Q1-3/22, Group sales increased by 10% (4% in constant currency) to €30,197 million (Q1-3/21: €27,554 million). Organic growth was 3%. Acquisitions/divestitures contributed net 1% to growth. Currency translation increased sales growth by 6%. Excluding estimated COVID-19 effects1, Group sales growth would have been 3% to 4% in constant currency (Q1-3/21: 5% to 6%).

19% net income2,3,4 decline in constant currency

Group EBITDA before special items decreased by 2% (-10% in constant currency) to €1,662 million (Q3/212: €1,703 million). Reported Group EBITDA was €1,658 million (Q3/21: €1,667 million).

In Q1-3/22, Group EBITDA before special items remained nearly unchanged (-6% in constant currency) at €5,006 million (Q1-3/212: €5,008 million). Reported Group EBITDA was €4,781 million (Q1-3/21: €4,957 million).

Group EBIT before special items decreased by 9% (-17% in constant currency) to €949 million (Q3/212: €1,044 million). The decrease was mainly driven by higher labor costs at Fresenius Medical Care in the U.S., general cost inflation, revaluation of contract assets in the international service and project business at Fresenius Vamed as well as higher costs in the Corporate segment. The EBIT margin before special items was 9.1% (Q3/212: 11.2%). Reported Group EBIT was €887 million (Q3/21: €1,008 million).

In Q1-3/22, Group EBIT before special items decreased by 4% (-10% in constant currency) to €2,952 million (Q1-3/212: €3,086 million). The EBIT margin before special items was 9.8% (Q1-3/212: 11.2%). Reported Group EBIT was €2,634 million (Q1-3/21: €3,035 million).

1 For estimated COVID-19 effects please see table on page 20.

2 Before special items

3 Net income attributable to shareholders of Fresenius SE & Co. KGaA

4 Excluding Ivenix and mAbxience acquisitions

For a detailed overview of special items please see the reconciliation tables on pages 22-25 in the PDF.

Group net interest before special items was -€141 million (Q3/211: -€126 million) mainly due to currency translation effects and overall higher interest rates. Reported Group net interest decreased to -€141 million (Q3/21: -€126 million).

In Q1-3/22, Group net interest before special items improved to -€376 million (Q1-3/211: -€384 million). Reported Group net interest improved to -€375 million (Q1-3/21: -€384 million).

Group tax rate before special items was 25.0% (Q3/211: 22.9%) mainly due to an increase in the proportionate share of non-tax-deductible expenses compared to taxable income at Fresenius Medical Care. Reported Group tax rate was 26.1% (Q3/21: 22.8%). In Q1-3/22, Group tax rate before special items was 23.5% (Q1-3/211: 22.4%) while the reported Group tax rate was 24.1% (Q1-3/21: 22.3%).

Noncontrolling interests before special items were -€235 million (Q3/211: -€273 million) of which 90% were attributable to the noncontrolling interests in Fresenius Medical Care. Reported noncontrolling interests were -€230 million (Q3/21: -€268 million).

In Q1-3/22, Noncontrolling interests before special items were -€686 million (Q1-3/211: -€751 million) of which 89% were attributable to the noncontrolling interests in Fresenius Medical Care. Reported noncontrolling interests were -€597 million (Q1-3/21: -€741 million).

Group net income2 before special items decreased by 15% (-22%/-19%3 in constant currency) to €371 million (Q3/211: €435 million). The decrease was mainly driven by higher labor costs at Fresenius Medical Care in the U.S., general cost inflation, revaluation of contract assets in the international service and project business at Fresenius Vamed as well as higher costs in the Corporate/Other segment. Moreover, increased interest expenses and a higher tax rate had a negative effect on Group net income. Excluding estimated COVID-19 effects4, Group net income2 before special items was -26% to -22% in constant currency (Q3/21: 12% to 16%). Reported Group net income2 decreased to €321 million (Q3/21: €413 million).

In Q1-3/22, Group net income2 before special items decreased by 5% (-10%/-8%3 in constant currency) to €1,284 million (Q1-3/211: €1,346 million). Excluding estimated COVID-19 effects4, Group net income2 before special items was -15% to -11% in constant currency (Q1-3/21: 7% to 11%). Reported Group net income2 decreased to €1,117 million (Q1-3/21: €1,319 million).

1 Before special items

2 Net income attributable to shareholders of Fresenius SE & Co. KGaA

3 Excluding Ivenix and mAbxience acquisitions

4 For estimated COVID-19 effects please see table on page 20

For a detailed overview of special items please see the reconciliation tables on pages 22-25 in the PDF.

Earnings per share1 before special items decreased by 15% (-22% in constant currency) to €0.66 (Q3/212: €0.78). Reported earnings per share1 were €0.57 (Q3/21: €0.74).

In Q1-3/22, earnings per share1 before special items decreased by 5% (-10% in constant currency) to €2.29 (Q1-3/212: €2.41). Reported earnings per share1 were €1.99 (Q1-3/21: €2.36).

Continued investment in growth

Spending on property, plant and equipment was €416 million corresponding to 4% of sales (Q3/21: €449 million; 5% of sales). These investments served primarily for the modernization and expansion of dialysis clinics, production facilities as well as hospitals and day clinics. In Q1-3/22, spending on property, plant and equipment was €1,173 million corresponding to 4% of sales (Q1-3/21: €1,342 million; 5% of sales).

Total acquisition spending was €502 million (Q3/21: €167 million), mainly for the majority stake in mAbxience by Fresenius Kabi. In Q1-3/22, total acquisition spending was €955 million (Q1-3/21: €807 million).

Cash flow development

Group operating cash flow increased to €1,256 million (Q3/21: €1,226 million) with a margin of 12.0% (Q3/21: 13.1%). Free cash flow before acquisitions and dividends increased to €876 million (Q3/21: €793 million). Free cash flow after acquisitions and dividends decreased to €388 million (Q3/21: €594 million).

In Q1-3/22, Group operating cash flow decreased to €2,374 million (Q1-3/21: €3,329 million) with a margin of 7.9% (Q1-3/21: 12.1%). Free cash flow before acquisitions and dividends decreased to €1,202 million (Q1-3/21: €1,986 million). Free cash flow after acquisitions and dividends decreased to -€406 million (Q1-3/21: €352 million).

Solid balance sheet structure

Group total assets increased by 12% (4% in constant currency) to €80,328 million (Dec. 31, 2021: €71,962 million) given currency translation effects, acquisitions and the expansion of business activities. Current assets increased by 11% (6% in constant currency) to €19,443 million (Dec. 31, 2021: €17,461 million), mainly driven by the increase of trade accounts receivables and inventories. Non-current assets increased by 12% (4% in constant currency) to €60,885 million (Dec. 31, 2021: €54,501 million).

Total shareholders’ equity increased by 17% (6% in constant currency) to €34,156 million (Dec. 31, 2021: €29,288 million). The equity ratio was 42.5% (Dec. 31, 2021: 40.7%).

Group debt increased by 5% (1% in constant currency) at €28,607 million (Dec. 31, 2021: € 27,155 million). Group net debt increased by 9% (4% in constant currency) to € 26,479 million (Dec. 31, 2021: € 24,391 million).

As of September 30, 2022, the net debt/EBITDA ratio was 3.74x1,2 (Dec. 31, 2021: 3.51x1,2) mainly driven by lower EBITDA contribution as well as acquisition spending. The net debt/EBITDA as of September 30, 2022 excluding the closed acquisition of Ivenix and the completed acquisition of a majority stake in mAbxience was 3.641,2.

1 At LTM average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures

2 Before special items

For a detailed overview of special items please see the reconciliation tables on pages 22-25 in the PDF.

Business Segments

Fresenius Medical Care

(Financial data according to Fresenius Medical Care press release)

Fresenius Medical Care is the world's largest provider of products and services for individuals with renal diseases. As of September 30, 2022, Fresenius Medical Care was treating 344,593 patients in 4,153 dialysis clinics. Along with its core business, the Renal Care Continuum, the company focuses on expanding in complementary areas and in the field of critical care.

- Business development continues to be strongly impacted by uncertain inflationary macroeconomic environment

- Impacts of improvements in North American Health Care Services operations delayed

- COVID-19-related excess mortality in line with expectations

- Important step in value-based care achieved with closing of InterWell Health merger

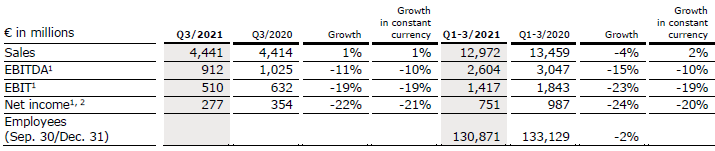

Sales increased by 15% (3% in constant currency) to €5,096 million (Q3/21: €4,441 million). Organic growth was 2%. Currency translation increased sales growth by 12%. In Q1-3/22, sales increased by 11% (2% in constant currency) to €14,401 million (Q1-3/21: €12,972 million). Organic growth was 1%. Currency translation increased sales growth by 9%.

EBIT decreased by 7% (-17% in constant currency) to €472 million (Q3/21: €505 million) resulting in a margin of 9.3% (Q3/21: 11.4%). EBIT before special items decreased by 8% (-18% in constant currency) to €470 million (Q3/21: €513 million), resulting in a margin1 of 9.2% (Q3/21: 11.6%). At constant currency, the decline was mainly due to higher labor costs as well as inflationary and supply chain cost increases. This was partially offset by €80 million (Q3 2021: €0.3 million) of Provider Relief Funding from the U.S. government to compensate for certain COVID-19-related costs. In Q1-3/22, EBIT decreased by 17% (-24% in constant currency) to €1,160 million (Q1-3/21: €1,403 million) resulting in a margin of 8.1% (Q1-3/21: 10.8%). EBIT before special items decreased by 7% (-14% in constant currency) to €1,322 million (Q1-3/21: €1,423 million), resulting in a margin1 of 9.2% (Q1-3/21: 11.0%).

Net income2 decreased by 16% (-24% in constant currency) to €230 million (Q3/21: €273 million). Net income2 before special items decreased by 17% (-25% in constant currency) to €231 million (Q3/21: €280 million). Besides the above-mentioned effects on operating income, the constant currency decline was mainly due to an increase in the proportionate share of non-tax-deductible expenses compared to taxable income.

In Q1-3/22, net income2 decreased by 28% (-34% in constant currency) to €535 million (Q1-3/21: €741 million). Net income2 before special items decreased by 13% (-18% in constant currency) to €660 million (Q1-3/21: €756 million).

Operating cash flow was €658 million (Q3/21: €692million) with a margin of 12.9% (Q3/21: 15.6%). The decrease was mainly due to lower net income. In Q1-3/22, operating cash flow was €1,568 million (Q1-3/21: €1,820 million) with a margin of 10.9% (Q1-3/21: 14.0%).

Based on the delayed impacts of improvements in North American Health Care Services operations, the continuously challenging and uncertain macroeconomic environment, and the results for the third quarter, which had a more pronounced support by one-time effects, Fresenius Medical Care, as a matter of caution, extends its 2022 guidance range for net income2,3 decline from a high-teens to a high-teens to mid-twenties percentage range. The Company confirms its target for revenue4 to grow at a low single digit percentage rate in full year 2022. Revenue and net income guidance are both on a constant currency basis and excluding special items5.

1 Before special items

2 Net income attributable to shareholders of Fresenius Medical Care AG & Co. KGaA

3 FY/21 base: €1,018 million, before special items; FY/22 before special items

4 FY/21 base: €17,619 million

5 These targets are based on the 2021 results excluding the costs related to FME25 of EUR 49 million (for Net Income). They are in constant currency and exclude special items. Special items include further costs related to FME25, the impact of the war in Ukraine, the impact of hyperinflation in Turkiye, the Humacyte investment remeasurement, the net gain related to InterWell Health and other effects that are unusual in nature and have not been foreseeable or not foreseeable in size or impact at the time of giving guidance.

For a detailed overview of special items please see the reconciliation tables on pages 22-25 in the PDF.

InterWell Health merger closed

With the closing of the three-way merger of Fresenius Health Partners, InterWell Health and Cricket Health, a premier value-based kidney care provider has been created in the U.S. This is an important step in the execution of Fresenius Medical Care’s strategy. The new company operates under the InterWell Health brand and will be fully consolidated by Fresenius Medical Care as the majority owner. The closing of the merger resulted in a net gain of €56 million (on EBIT level) in the third quarter, which is treated as a special item.

For further information, please see Fresenius Medical Care’s press release at www.freseniusmedicalcare.com.

Fresenius Kabi

Fresenius Kabi offers intravenously administered generic drugs, clinical nutrition and infusion therapies for seriously and chronically ill patients in the hospital and outpatient environments. The company is also a leading supplier of medical devices and transfusion technology products. In the biosimilars business, Fresenius Kabi develops products with a focus on oncology and autoimmune diseases.

1 Before special items

2 Net income attributable to shareholders of Fresenius SE & Co. KGaA

3 Excluding Ivenix and mAbxience acquisitions

For a detailed overview of special items please see the reconciliation tables on pages 22-25 in the PDF.

- Solid organic sales growth in all three growth vectors against already strong Q3/21

- Biopharmaceuticals continue strong trajectory in line with ambitious plan

- Growth in Europe and rest of the world outweighing pressures in North America

- Sequentially constant EBIT margin3 despite headwinds from cost increases

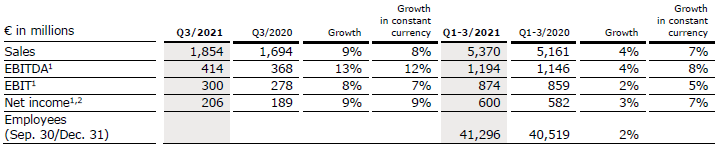

Sales increased by 12% (4% in constant currency) to €2,071 million (Q3/21: €1,854 million). Organic growth was 3%. In Q1-3/22, sales increased by 8% (2% in constant currency) to €5,814 million (Q1-3/21: €5,370 million). Organic growth was 2%. Positive currency translation effects of 8% in Q3/22 and 6% in Q1-3/22 were mainly related to the U.S. dollar and Chinese yuan.

Sales in North America increased by 13% (organic growth: -2%) to €668 million (Q3/21: €589 million). The significant sales growth was mainly driven by positive currency effects while organic growth continued to be impacted by ongoing competitive pressure and supply chain challenges. In Q1-3/22, sales in North America increased by 11% (organic growth: -1%) to €1,853 million (Q1-3/21: €1,669 million).

Sales in Europe increased by 8% (organic growth: 6%) to €669 million (Q3/21: €620 million) driven by a broad-based positive development, and biopharmaceuticals. In Q1-3/22, sales in Europe increased by 5% (organic growth: 4%) to €1,967 million (Q1-3/21: €1,880 million).

Sales in Asia-Pacific increased by 4% (organic growth: -4%) to €467 million (Q3/21: €447 million). Organic growth was affected by price pressure from the NVBP (National Volume-Based Procurement) tenders in China. In Q1-3/22, sales in Asia-Pacific increased by 6% (organic growth: -2%) to €1,325 million (Q1-3/21: €1,248 million).

Sales in Latin America/Africa increased by 35% (organic growth: 27%) to €267 million (Q3/21: €198 million), due to a positive business development in both regions. In Q1-3/22, sales in Latin America/Africa increased by 17% (organic growth: 11%) to €669 million (Q1-3/21: €573 million).

Sales in the Biopharmaceuticals business was €64 million. In Q1-3/22, sales in the Biopharmaceuticals business was €116 million.

EBIT1 decreased by 7% (-18%/-11% in constant currency) to €280 million (Q3/21: €300 million), mainly related to ongoing cost inflation, supply chain challenges as well as competitive pressure. EBIT margin1 was 13.5% (Q3/21: 16.2%). Excluding the acquisitions of Ivenix and the majority stake in mAbxience, the constant currency EBIT margin1 was sequentially stable at 14.6%2 in Q3/22 (Q2/22: 14.7%2) despite the mentioned headwinds. In Q1-3/22, EBIT1 decreased by 3% (-12%/-9%2 in constant currency) to €844 million (Q1-3/21: €874 million) with an EBIT margin1 of 14.5%/15.0%2 (Q1-3/21: 16.3%).

Net income1,3 decreased by 11% (-21% in constant currency) to €184 million (Q3/21: €206 million). In Q1-3/22, net income1,3 decreased by 4% (-13% in constant currency) to €574 million (Q1-3/21: €600 million).

1 Before special items

2 Excluding Ivenix and mAbxience acquisitions

3 Net income attributable to shareholders of Fresenius SE & Co. KGaA

For a detailed overview of special items please see the reconciliation tables on pages 22-25 in the PDF.

Operating cash flow decreased to €301 million (Q3/21: €393 million) with a margin of 14.5% (Q3/21: 21.2%), mainly driven by a working capital build-up from e.g. higher inventories. In Q1-3/22, operating cash flow decreased to €543 million (Q1-3/21: €868 million) with a margin of 9.3% (Q1-3/21: 16.2%).

For FY/22, Fresenius Kabi confirms its outlook and expects organic sales1 growth in a low-single-digit percentage range. Constant currency EBIT2 is expected to decline in a high-single- to low-double-digit percentage range. Both sales and EBIT outlook include expected COVID-19 effects. The financial effects from the acquisitions of Ivenix and the majority stake in mAbxience remain excluded from guidance.

1 FY/21 base: €7,193 million

2 FY/21 base: €1,153 million, before special items, FY/22 before special items,

excluding Ivenix and mAbxience acquisitions

For a detailed overview of special items please see the reconciliation tables on pages 22-25 in the PDF.

Fresenius Helios

Fresenius Helios is Europe's leading private hospital operator. The company comprises Helios Germany, Helios Spain and Helios Fertility. Helios Germany operates 87 hospitals, ~130 outpatient centers and 6 prevention centers. Helios Spain operates 50 hospitals, 101 outpatient centers and around 300 occupational risk prevention centers. In addition, the company is active in Latin America with 8 hospitals and as a provider of medical diagnostics. Helios Fertility offers a wide spectrum of state-of-the-art services in the field of fertility treatments.

- Fresenius Helios with strong organic sales growth; solid EBIT development in line with usual third quarter seasonality

- Helios Germany with gradually improving admissions

- Helios Spain with ongoing healthy activity levels

- Helios Fertility with lower volumes driven by delayed treatments

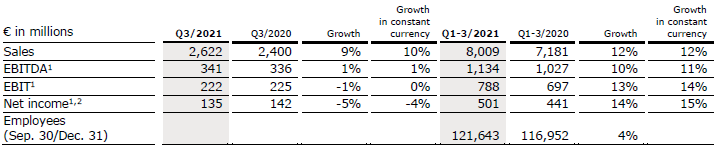

Sales increased by 8% (7% in constant currency) to €2,829 million (Q3/21: €2,622 million). Organic growth was 6%. Acquisitions, mainly at Helios Fertility, contributed 2% to sales growth. Divestments reduced sales by 1%. In Q1-3/22, sales increased by 8% (8% in constant currency) to €8,685 million (Q1-3/21: €8,009 million). Organic growth was 6%. Acquisitions contributed 2% to sales growth.

Sales of Helios Germany increased by 6% (organic growth: 5%) to €1,731 million (Q3/21: €1,640 million), mainly driven by gradually increasing admissions, which are however still below pre-pandemic levels. Acquisitions contributed 1% to sales growth. In Q1-3/22, sales of Helios Germany increased by 6% (organic growth: 5%) to €5,272 million (Q1-3/21: €4,988 million). Acquisitions contributed 1% to sales growth.

Sales of Helios Spain increased by 10% (9% in constant currency) to €1,037 million (Q3/21: €941 million). Organic growth of 8% was driven by the continuous high level of treatment activity. The clinics in Latin America also showed a good performance. Acquisitions contributed 1% to sales growth. In Q1-3/22, sales of Helios Spain increased by 10% (9% in constant currency) to €3,227 million (Q1-3/21: €2,937 million). Organic growth was 9%.

Sales of the Helios Fertility were €62 million (Q3/21: €40 million). In Q1-3/22, sales of the Helios Fertility were €184 million.

EBIT1 remained stable (-1% in constant currency) at €222 million (Q3/21: €222 million) with an EBIT margin1 of 7.8% (Q3/21: 8.5%). In Q1-3/22, EBIT1 increased by 5% (5% in constant currency) to €831 million (Q1-3/21: 788 million) with an EBIT margin1 of 9.6% (Q1-3/21: 9.8%).

EBIT1 of Helios Germany increased by 1% to €141 million (Q3/21: €140 million) with an EBIT margin1 of 8.1% (Q3/21: 8.5%). The increase of costs from the use of external staff due to COVID-19 related staff absenteeism continued to weigh on profitability. Inflationary cost effects had only a small negative impact. In Q1-3/22, EBIT1 of Helios Germany increased by 2% to €449 million (Q1-3/21: €442 million) with an EBIT margin1 of 8.5% (Q1-3/21: 8.9%).

EBIT1 of Helios Spain increased by 5% (3% in constant currency) to €83 million (Q3/21: €79 million) despite increased cost inflation. The EBIT margin1 was 8.0% (Q3/21: 8.4%). In Q1-3/22, EBIT1 of Helios Spain increased by 9% (9% in constant currency) to €384 million (Q1-3/21: €352 million). The EBIT margin1 was 11.9% (Q1-3/21: 12.0%).

EBIT1 of Helios Fertility was €4 million with an EBIT margin1 of 6.5% (Q3/21: €9 million). Lower volumes by delayed treatments driven by macroeconomic environment. Prior year quarter was inflated by a positive special item. In Q1-3/22, EBIT1 of Helios Fertility was €15 million (Q1-3/21: €14 million) with an EBIT margin1 of 8.2%.

Net income1,2 increased by 2% (1% in constant currency) to €138 million (Q3/21: €135 million). In Q1-3/22, net income1,2 increased by 6% (5% in constant currency) to €530 million (Q1-3/21: €501 million).

Operating cash flow increased to €353 million (Q3/21: €157 million) with a margin of 12.5% (Q3/21: 6.0%) mainly due to an improved receivables management in Spain. In Q1-3/22, operating cash flow decreased to €411 million (Q1-3/21: €595 million) with a margin of 4.7% (Q1-3/21: 7.4%)

For FY/22, Fresenius Helios confirms its outlook and expects organic sales3 growth in a low- to mid-single-digit percentage range and constant currency EBIT4 growth in a mid-single-digit percentage range. Both sales and EBIT outlook include expected COVID-19 effects.

1 Before special items

2 Net income attributable to shareholders of Fresenius SE & Co. KGaA

3 FY/21 base: €10,891 million

4 FY/21 base: €1,127 million, before special items, FY/22 before special items

For a detailed overview of special items please see the reconciliation tables on pages 22-25 in the PDF.

Fresenius Vamed

Fresenius Vamed manages projects and provides services for hospitals and other health care facilities worldwide and is a leading post-acute care provider in Central Europe. The portfolio ranges along the entire value chain: from project development, planning, and turnkey construction, via maintenance and technical management to total operational management.

- Service business with solid top-line performance, but higher than estimated COVID-19 impact in rehabilitation business impacts earnings

- Despite improved top-line development, macro challenges remain a headwind in the project business

- Revaluation of contractual assets in the international service and project business weighed on EBIT development

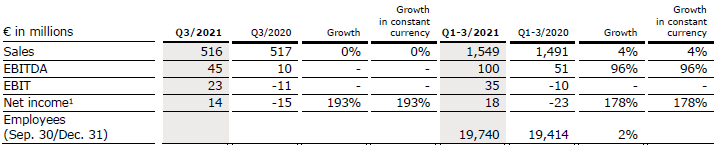

Sales increased by 11% (10% in constant currency) to €572 million (Q3/21: €516 million). Organic growth was 10%. In Q1-3/22, sales increased by 6% (6% in constant currency) to €1,647 million (Q1-3/21: €1,549 million). Organic growth was 6%.

Sales in the service business increased by 2% (1% in constant currency) to €418 million (Q3/21: €410 million) due to increasing rehabilitation treatments given fewer capacity restrictions. Sales in the project business increased by 45% (45% in constant currency) to €154 million (Q3/21: €106 million. In Q1-3/22, sales in the service business increased by 6% (5% in constant currency) to €1,240 million (Q1-3/21: €1,165 million). Sales in the project business increased by 6% (6% in constant currency) to €407 million (Q1-3/21: €384 million).

EBIT1 decreased by 57% to €10 million (Q3/21: €23 million) with an EBIT margin1 of 1.7% (Q3/21: 4.5%) driven by macroeconomic headwinds, ongoing COVID impacts, cost inflation as well as the revaluation of contractual assets in the international service and project business. In Q1-3/22, EBIT1 decreased by 17% to €29 million (Q1-3/21: €35 million) with an EBIT margin1 of 1.8% (Q1-3/21: 2.3%).

Net income1,2 decreased by 64% to €5 million (Q3/21: €14 million). In Q1-3/22, Net income1,2 decreased by 17% to €15 million (Q1-3/21: €18 million).

Order intake was €153 million (Q3/21: €120 million). In Q1-3/22 order intake was €669 million (Q1-3/21: €971 million). As of September 30, 2022, order backlog was at €3,726 million (December 31, 2021: €3,473 million).

Operating cash flow decreased to -€18 million (Q3/21: €9 million) with a margin of -3.1% (Q3/21: 1.7%), due to working capital build-ups. In Q1-3/22, operating cash flow decreased to -€56 million (Q1-3/21: €23 million) with a margin of -3.4% (Q1-3/21: 1.5%).

Fresenius Vamed adjusts its outlook for FY/22 and now expects organic sales3 to grow in a mid-single digit percentage range (previously: high-single to low-double-digit percentage range). Constant currency EBIT4 is expected to be around €100 million (previously: return to absolute pre-COVID-19 levels (FY/19: €134 million). Both sales and EBIT outlook include expected COVID-19 effects.

1 Before special items

2 Net income attributable to shareholders of VAMED AG

3 FY/21 base: €2,297 million

4 FY/21 base: €101 million, before special items; FY/22 before special items

For a detailed overview of special items please see the reconciliation tables on pages 22-25 in the PDF.

This release contains forward-looking statements that are subject to various risks and uncertainties. Future results could differ materially from those described in these forward-looking statements due to certain factors, e.g. changes in business, economic and competitive conditions, regulatory reforms, results of clinical trials, foreign exchange rate fluctuations, uncertainties in litigation or investigative proceedings, the availability of financing and unforeseen impacts of international conflicts. Fresenius does not undertake any responsibility to update the forward-looking statements in this release.

- Business development marked by significantly worsening headwinds at Fresenius Medical Care and increased macroeconomic challenges

- Fresenius Medical Care Business development impacted by unprecedented U.S. labor market situation and worsening macroeconomic environment

- Fresenius Kabi with solid organic sales growth despite tough prior-year-quarter

- Fresenius Helios with continued good admissions growth in Germany and Spain

- Fresenius Vamed still impacted by ongoing headwinds; service business supported by increasing elective treatment activity

- Cost and efficiency program evolving according to plan

- Starting date for Dr. Carla Kriwet as CEO of Fresenius Medical Care advanced to October 1, 2022

If no timeframe is specified, information refers to Q2/2022.

1 Before special items, Q1/22 restated following remeasurement Humacyte investment

2 Net income attributable to shareholders of Fresenius SE & Co. KGaA

3 Excluding Ivenix acquisition

For a detailed overview of special items please see the reconciliation tables on pages 21-24 in the PDF.

FY/22 Group guidance revised

Fresenius Medical Care’s financial performance in Q2/22 was significantly impacted by worsened labor shortages and related meaningfully increased wage inflation in the U.S. The further deterioration of the macro-economic environment resulted in accelerated non-wage inflation, particularly higher supply chain costs.

Against this backdrop and growing indications for a persistent unfavorable development of these and other factors, Fresenius Medical Care has revised its outlook for FY/22.

All other Fresenius Group segments confirm their respective outlook for FY/22 for both revenue and EBIT.

However, as a consequence of the development at Fresenius Medical Care, and despite all other Fresenius Group segments confirming their respective outlook for both revenue and EBIT, Fresenius now also revises its Group outlook for FY/22. As announced on July 27, 2022, at constant currency, the Company now anticipates Group sales1 to grow in a low-to-mid single-digit percentage range (previously: mid-single digit percentage range) and Group net income2,3 to decline in a low-to-mid single-digit percentage range (previously: increase in a low-single-digit percentage range).

Without the already closed acquisitions of Ivenix and the already completed acquisition of a majority stake in mAbxience as well as any further potential acquisitions, Fresenius expects the net debt/EBITDA4 ratio (December 31, 2021: 3.51x5) to be slightly above the top end of the self-imposed target corridor of 3.0x to 3.5x by the end of 2022.

1 FY/21 base: €37,520 million

2 Net income attributable to shareholders of Fresenius SE & Co. KGaA

3 FY/21 base: €1,867 million; before special items; FY/22: before special items

4 At LTM average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures; excluding further potential acquisitions; before special items; including lease liabilities

5 At LTM average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures; before special items; including lease liabilities

For a detailed overview of special items please see the reconciliation tables on pages 21-24 in the PDF.

Assumptions for guidance FY/22

Due to the meaningfully increased uncertainty and volatility related to the war in Ukraine, the ongoing impacts of the COVID-19 pandemic, and a rapidly worsening global macro-economic development, Fresenius now expects significantly more pronounced headwinds in 2022 from supply chain disruptions and cost inflation, including energy prices. Furthermore, Fresenius expects significant negative effects from ongoing labor shortages and associated wage inflation, especially at Fresenius Medical Care in the U.S.

The war in Ukraine is directly and indirectly affecting Fresenius Group operations. The direct adverse effects of the war amounted to €20 million at net income level of Fresenius Group in H1/22 and are treated as a special item. Fresenius will continue to closely monitor the potential further consequences of the war, including balance sheet valuations. The guidance does not consider a significant disruption of gas or electricity supplies in Europe.

COVID-19 will continue to impact Fresenius Group operations in 2022. An unlikely but possible significant deterioration of the situation triggering containment measures that could have a significant and direct impact on the health care sector without any appropriate compensation is not reflected in the Group’s FY/22 guidance.

Furthermore, the updated assumptions for Fresenius Medical Care's FY/22 guidance are also fully applicable to Fresenius Group's FY/22 guidance. All of these assumptions are subject to considerable uncertainty. The acquisitions of Ivenix and of the majority stake in mAbxience as well as any further potential acquisitions remain excluded from guidance.

Group medium-term targets

As a result of the updated expectations for FY/22, Fresenius now believes its medium-term net income1 target is no longer achievable. Fresenius had expected Group organic net income1 growth to be at the bottom end of the 5% to 9% compounded annual growth rate (CAGR) range for 2020 to 2023. At the same time, Fresenius specifies its Group organic sales growth target to reach the low-end of the targeted 4% to 7% compounded annual growth rate (CAGR) range for 2020 to 2023.

1 Net income attributable to shareholders of Fresenius SE & Co. KGaA

Cost and efficiency program

The Group’s cost and efficiency program is running according to plan and Fresenius confirms its increased savings targets provided in February 2022 of at least €150 million p.a. after tax and minority interest in 2023. For the years thereafter, a further significant increase in sustainable cost savings is expected.

Management Board change at Fresenius Medical Care

Dr. Carla Kriwet will now join Fresenius Medical Care as CEO on October 1, 2022, earlier than previously announced and Rice Powell will step down as CEO effective September 30, 2022.

3% sales increase in constant currency

Group sales increased by 8% (3% in constant currency) to €10,018 million (Q2/21: €9,246 million). Organic growth was 2%. Acquisitions/divestitures contributed net 1% to growth. Currency translation increased sales growth by 5%. Excluding estimated COVID-19 effects , Group sales growth would have been 2% to 3% in constant currency (Q2/21: 6% to 7%).

In H1/22, Group sales increased by 8% (4% in constant currency) to €19,738 million (H1/21: €18,230 million). Organic growth was 3%. Acquisitions/divestitures contributed net 1% to growth. Currency translation increased sales growth by 4%. Excluding estimated COVID-19 effects1, Group sales growth would have been 4% to 5% in constant currency (H1/21: 5% to 6%).

9% net income2,3,4 decline in constant currency

Group EBITDA before special items remained stable (-6% in constant currency) at €1,682 million (Q2/212: €1,674 million). Reported Group EBITDA was €1,528 million (Q2/21: €1,662 million).

In H1/22, Group EBITDA before special items increased by 1% (-4% in constant currency) to €3,344 million (H1/212: €3,305 million). Reported Group EBITDA was €3,123 million (H1/21: €3,290 million).

Group EBIT before special items decreased by 3% (-9% in constant currency) to €1,003 million (Q2/212: €1,033 million). The decrease was mainly driven by worsened labor shortages and related meaningfully increased wage inflation at Fresenius Medical Care in the U.S. as well as elevated material and logistic costs. The EBIT margin before special items was 10.0% (Q2/212: 11.2%). Reported Group EBIT was €845 million (Q2/21: €1,021 million).