• Guidance for 2021 confirmed

• Fresenius Medical Care delivers solid first quarter

• Fresenius Kabi shows strong performance in Emerging Markets whilst headwinds continue to impact North American business

• Helios Germany continues to be compensated by government for foregone elective treatments; Helios Spain delivers significant sales and earnings growth given recovery of treatment activity

• Fresenius Vamed continues to suffer from COVID-19 related project delays; technical high-end service business remains robust

• Preparation of Group-wide initiatives to improve efficiency and profitability progressing

If no timeframe is specified, information refers to Q1/2021. In Q1/2021 no special items incurred.

1 Before special items

2 Net income attributable to shareholders of Fresenius SE & Co. KGaA

For a detailed overview of special items please see the reconciliation table in the PDF document.

Stephan Sturm, CEO of Fresenius, said: “In view of the adversity and uncertainties that COVID-19 continues to bring, we are satisfied with our start in 2021. We achieved continued organic growth, although the pandemic had a lesser impact on the prior-year quarter. That makes me optimistic that we can reach our targets. The progress being made with vaccinations worldwide is another reason for confidence, even though it is too early to sound the all-clear. In the coming months, we will still be dealing with the pandemic’s many and wide-ranging effects. As before, we will do this with full responsibility for the patients entrusted to us. At the same time, we are moving ahead with our planning for cost and efficiency measures. These measures will create a strong foundation for accelerated and sustainable growth against the backdrop of long-term growth trends supporting our core businesses. Growth that contributes to ever better medicine for ever more people.”

COVID-19 assumptions for guidance FY/21

Q1/21 was characterized by a regionally varying development of the COVID-19 pandemic. Given continued high infection numbers as well as an increasing number of virus mutations, large-scale constraints of public and private life have been re-enacted in various countries. Vaccination programs are progressing worldwide at, however, varying pace.

COVID-19 will continue to impact Fresenius’ operations in 2021. Current burdens and constraints caused by COVID-19 are expected to recede only in H2/21. The expected improvement in the Group’s relevant business environment from H2/21 is heavily dependent on continuously increasing levels of vaccination coverage in Fresenius’ relevant markets. These assumptions are subject to considerable uncertainty.

A deterioration of the situation requiring further containment measures in one or more of Fresenius’ major markets, although becoming somewhat less likely does remain a risk. Any resulting significant and direct impact on the health care sector without any appropriate compensation is not reflected in the Group’s FY/21 guidance.

FY/21 Group guidance confirmed

For FY/21, Fresenius continues to project sales growth1 in a low-to-mid single-digit percentage range and at least broadly stable net income2,3 year-over-year, both in constant currency. Implicitly, net income2 for the Group excluding Fresenius Medical Care is expected to grow in a mid-to-high single-digit percentage range in constant currency.

Fresenius projects net debt/EBITDA4 to be around the top-end of the self-imposed target corridor of 3.0x to 3.5x by the end of FY/21.

To sustainably enhance profitability, Fresenius is preparing group-wide strategic efficiency initiatives. These initiatives are expected to consist of operational excellence and cost-saving measures, targeted strengthening of future growth areas and portfolio optimizations. They are targeted to result in cost savings of at least €100 million p.a. after tax and minority interest in 2023 with some further potential to increase thereafter. Achieving these sustainable efficiencies will require significant up-front expenses. On average for the years 2021 to 2023, those expenses are expected to be in the order of magnitude of €100 million p.a. after tax and minority interest. They will be classified as special items.

1 FY/20 base: €36,277 million

2 Net income attributable to shareholders of Fresenius SE & Co. KGaA

3 FY/20 base: €1,796 million, before special items; FY/21: before special items

4 At LTM average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures; excluding further potential acquisitions; before special items

For a detailed overview of special items please see the reconciliation table in the PDF document.

3% sales increase in constant currency

Group sales decreased by 2% (increased by 3% in constant currency) to €8,984 million (Q1/20: €9,135 million). Organic growth was 2%. Acquisitions/divestitures contributed net 1% to growth. Currency translation reduced sales growth by 5%. Excluding estimated COVID-19 effects1, Group sales growth would have been 4% to 5% in constant currency (Q1/20: 7% to 8%).

2% net income2,3 decrease in constant currency

Group EBITDA before special items and reported Group EBITDA decreased by 7% (-2% in constant currency) to €1,628 million (Q1/20: €1,755 million).

Group EBIT before special items and reported Group EBIT decreased by 11% (-6% in constant currency) to €1,006 million (Q1/20: €1,125 million). The constant currency decrease is primarily due to COVID-19 related headwinds. Both the EBIT margin before special items and the reported EBIT margin were 11.2% (Q1/20: 12.3%).

Group net interest before special items improved to -€137 million (Q1/202: -€174 million) mainly due to successful refinancing activities, lower interest rates as well as currency translation effects. Reported Group net interest also improved to -€137 million (Q1/20: -€182 million).

Both the Group tax rate before special items and the reported tax rate were 22.8% (Q1/20: 22.6%).

Both Noncontrolling interests before special items and reported noncontrolling interests were -€236 million (Q1/20: -€271 million) of which 95% were attributable to the noncontrolling interests in Fresenius Medical Care.

1 For estimated COVID-19 effects in Q1/21 and Q1/20 please see table in the PDF document.

2 Before special items

3 Net income attributable to shareholders of Fresenius SE & Co. KGaA

For a detailed overview of special items please see the reconciliation table in the PDF document.

Group net income1 before special items decreased by 6% (-2% in constant currency) to €435 million (Q1/202: €465 million). The absolute negative COVID-19 effect was more pronounced in Q1/21 compared to the prior-year quarter. Excluding estimated COVID-19 effects3, Group net income1 before special items would have grown 0% to 4% in constant currency (Q1/20: 6% to 10%). Reported Group net income1 decreased to €435 million (Q1/20: €459 million).

Earnings per share1 before special items decreased by 6% (-2% in constant currency) to €0.78 (Q1/202: €0.83). Reported earnings per share1 were also €0.78 (Q1/20: €0.82).

Continued investment in growth

Spending on property, plant and equipment was €384 million corresponding to 4% of sales (Q1/20: €547 million; 6% of sales). These investments served primarily for the modernization and expansion of dialysis clinics, production facilities as well as hospitals and day clinics.

Total acquisition spending was €149 million (Q1/20: €412 million), mainly for the acquisition of dialysis clinics at Fresenius Medical Care.

Cash flow development

Group operating cash flow decreased to €652 million (Q1/20: €878 million) with a margin of 7.3% (Q1/20: 9.6%), driven by a seasonal fluctuation in Fresenius Medical Care's invoicing and working capital movements in North America. Free cash flow before acquisitions and dividends decreased to €241 million (Q1/20: €305 million). Free cash flow after acquisitions and dividends increased to €117 million (Q1/20: -€40 million).

1 Net income attributable to shareholders of Fresenius SE & Co. KGaA

2 Before special items

3 For estimated COVID-19 effects in Q1/21 and Q1/20 please see table in the PDF document.

For a detailed overview of special items please see the reconciliation table in the PDF document.

Solid balance sheet structure

Group total assets increased by 3% (1% in constant currency) to €68,966 million (Dec. 31, 2020: €66,646 million) given currency translation effects and the expansion of business activities. Current assets increased by 6% (4% in constant currency) to €16,693 million (Dec. 31, 2020: €15,772 million), mainly driven by the increase of trade accounts receivables. Non-current assets increased by 3% (0% in constant currency) to €52,273 million (Dec. 31, 2020: €50,874 million).

Total shareholders’ equity increased by 6% (3% in constant currency) to €27,514 million (Dec. 31, 2020: €26,023 million). The equity ratio was 39.9% (Dec. 31, 2020: 39.0%).

Group debt increased by 2% (1% in constant currency) to €26,508 million (Dec. 31, 2020: € 25,913 million). Group net debt increased by 2% (1% in constant currency) to € 24,631 million (Dec. 31, 2020: € 24,076 million).

As of March 31, 2021, the net debt/EBITDA ratio increased to 3.52x1,2 (Dec. 31, 2020: 3.44x1,2) driven by COVID-19 effects weighing on EBITDA as well as increased net debt.

1 At LTM average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures

2 Before special items

For a detailed overview of special items please see the reconciliation table in the PDF document.

Business Segments

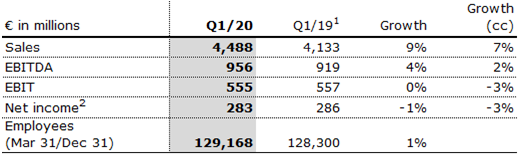

Fresenius Medical Care (Financial data according to Fresenius Medical Care press release)

Fresenius Medical Care is the world's largest provider of products and services for individuals with renal diseases. As of March 31, 2021, Fresenius Medical Care was treating 344,476 patients in 4,110 dialysis clinics. Along with its core business, the Renal Care Continuum, the company focuses on expanding in complementary areas and in the field of critical care.

• Organic treatment growth impacted by COVID-19 pandemic as expected

• Reported revenue and earnings continued to be adversely affected by exchange rate effects

• Earnings development supported by phasing and expected lower SG&A expense anticipated to reverse throughout the year

• Financial targets for FY 2021 confirmed

Sales of Fresenius Medical Care decreased by 6% (increased by 1% in constant currency) to €4,210 million (Q1/20: €4,488 million). Thus, currency translation had a negative effect of 7%. Organic growth was 1%.

EBIT decreased by 15% (-8% in constant currency) to €474 million (Q1/20: €555 million) resulting in a margin of 11.3% (Q1/20: 12.4%). The decrease was mainly driven by effects from COVID-19 across all regions, higher personnel expenses and a significant negative exchange rate effect. Additionally, EBIT was negatively affected by a positive prior-year effect from the divestiture of cardiovascular clinics and a prior-year partial reversal of a revenue recognition adjustment. These negative effects were partially offset by an improved payor mix mainly driven by Medicare Advantage and expected lower SG&A expenses, which are anticipated to reverse in the remainder of the year.

1 Net income attributable to shareholders of Fresenius Medical Care AG & Co. KGaA

Net income1 decreased by 12% (-6% in constant currency) to €249 million (Q1/20: €283 million). Besides the above-mentioned operating earnings effects, net income was supported by a 27% decrease of net interest expense to €76 million (Q1/20: €104 million).

The first quarter 2020 included negative COVID-19 effects that reversed in Q2 2020, including the compensation received under the CARES Act, and therewith increase the base for the second quarter 2021. These base effects impact the phasing of net income growth in 2021.

Operating cash flow was €208 million (Q1/20: €584 million) with a margin of 4.9% (Q1/20: 13.0%). The decline was driven by the seasonality in invoicing and periodic delays in payment of public health care organizations.

For FY/21, Fresenius Medical Care confirms its outlook as outlined on February 23, 2021. The Company expects revenue2 to grow at a low-to-mid single-digit percentage range and net income1,3 to decline at a high-teens to mid-twenties percentage range against the 2020 base4.

For further information, please see Fresenius Medical Care’s press release at www.freseniusmedicalcare.com.

1 Net income attributable to shareholders of Fresenius Medical Care AG & Co. KGaA

2 FY/20 base: €17,859 million

3 FY/20 base: €1,359 million, before special items; FY/21: before special items

4 These targets are based on the 2020 results excluding the impairment of goodwill and trade names in the Latin America Segment of €195 million. They are inclusive of anticipated COVID-19 effects, in constant currency and exclude special items. Special items include costs related to FME25 and other effects that are unusual in nature and have not been foreseeable or not foreseeable in size or impact at the time of giving guidance.

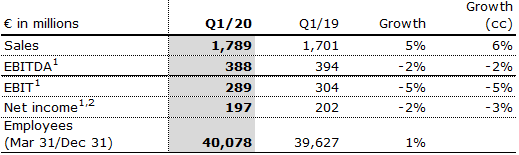

Fresenius Kabi

Fresenius Kabi offers intravenously administered generic drugs, clinical nutrition and infusion therapies for seriously and chronically ill patients in the hospital and outpatient environments. The company is also a leading supplier of medical devices and transfusion technology products. In the biosimilars business, Fresenius Kabi develops products with a focus on oncology and autoimmune diseases.

• North America performance impacted by COVID-19 and temporary manufacturing issues

• Solid performance in Europe masked by prior-year COVID-19 related demand spike

• Emerging Markets showed strong sales and earnings growth; China with excellent performance given dynamic recovery of elective treatment activity

Sales decreased by 2% (increased by 4% in constant currency) to €1,761 million (Q1/20: €1,789 million). Organic growth was 3%. Negative currency translation effects of 6% were mainly related to weakness of the US dollar, the Brazilian real and the Argentinian peso.

Sales in North America decreased by 17% (organic growth: -9%) to €558 million (Q1/20: €669 million). The decrease was driven by fewer elective treatments, competitive pressure, missing sales from a customer in Chapter 11 as well as temporary manufacturing issues which outweighed extra demand for COVID-19 related products.

Sales in Europe decreased by 1% (organic growth: -1%) to €626 million (Q1/20: €631 million) mainly related to the strong demand for COVID-19 related drugs in the prior year quarter.

Sales in Asia-Pacific increased by 23% (organic growth: 26%) to €392 million (Q1/20: €319 million). The growth is mainly due to a dynamic recovery of elective procedures and a meaningful COVID-19 impact lowering the prior year basis in China as well as a growing recovery in other Asian markets.

1 Before special items

2 Net income attributable to shareholders of Fresenius SE & Co. KGaA

Sales in Latin America/Africa increased by 9% (organic growth: 28%) to €185 million (Q1/20: €170 million) due to ongoing COVID-19 related extra demand.

EBIT1 decreased by 4% (increased by 2% in constant currency) to €276 million (Q1/20: €289 million) with an EBIT margin of 15.7% (Q1/20:16.2%). The increase in constant currency was tempered by underutilized production capacities in the US, competitive pressure coupled with selective supply constraints due to temporary manufacturing issues and the missing contribution from sales to a customer now in Chapter 11. EBIT was supported by positive COVID-19 effects, lower corporate costs due to travel restrictions and phasing of projects.

Net income1,2 decreased by 4% (increased by 3% in constant currency) to €190 million (Q1/201: €197 million).

Operating cash flow increased to €278 million (Q1/20: €174 million) with a margin of 15.8% (Q1/20: 9.7%) mainly due to working capital improvements driven by cash collections.

For FY/21, Fresenius Kabi confirms its outlook and expects organic sales3 growth in a low-to-mid single-digit percentage range. Constant currency EBIT4 is expected to show a stable development up to low single-digit percentage growth. Both sales and EBIT outlook include expected COVID-19 effects.

1 Before special items

2 Net income attributable to shareholders of Fresenius SE & Co. KGaA

3 FY/20 base: €6,976 million

4 FY/20 base: €1,095 million, before special items; FY/21: before special items

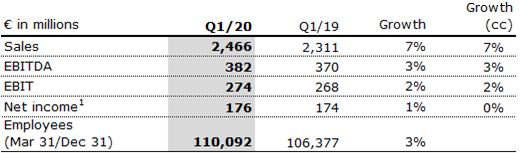

Fresenius Helios

Fresenius Helios is Europe's leading private hospital operator. The company comprises Helios Germany and Helios Spain. Helios Germany operates 89 hospitals, ~130 outpatient centers and 6 prevention centers. Helios Spain operates 47 hospitals, 74 outpatient centers and around 300 occupational risk prevention centers. In addition, the company is active in Latin America with 6 hospitals and as a provider of medical diagnostics.

• Helios Spain delivers significant organic sales and earnings growth given recovery of treatment activity

• Helios Germany continues to be compensated by government for foregone elective treatments

• Growth additionally fueled by contributions from acquisitions in Germany and Latin America

Sales increased by 7% (8% in constant currency) to €2,649 million (Q1/20: €2,466 million). Organic growth was 4%. Acquisitions contributed 4% to sales growth.

Sales of Helios Germany increased by 4% (organic growth: 0%) to €1,673 million (Q1/20: €1,603 million). COVID-19 effects were mitigated by government compensation in regions with high COVID-19 incidences. The hospital acquisitions from the Order of Malta contributed 4% to sales growth.

Sales of Helios Spain increased by 13% (14% in constant currency) to €976 million (Q1/20: €863 million). Organic growth of 11% was driven by a strong recovery of elective procedures, a consistently high level of outpatient treatments and strong demand for occupational risk prevention (ORP) services. In addition, the hospitals in Latin America showed a strong performance. The hospital acquisitions in Colombia contributed 3% to sales growth.

EBIT of Fresenius Helios decreased by 2% (-1% in constant currency) to €268 million (Q1/20: €274 million) with an EBIT margin of 10.1% (Q1/20: 11.1%).

1 Net income attributable to shareholders of Fresenius SE & Co. KGaA

EBIT of Helios Germany decreased by 9% to €150 million (Q1/20: €165 million) with an EBIT margin of 9.0% (Q1/20: 10.3%). Government compensation broadly mitigated COVID-19 effects. The decrease was primarily caused by the impact of the carve-out of nursing expenses from the overall DRGs and the positive development of January and February last year.

EBIT of Helios Spain increased by 13% (14% in constant currency) to €126 million (Q1/20: €112 million) with an EBIT margin of 12.9% (Q1/20: 13.0%). Healthy organic sales growth led to a meaningfully improved coverage of the fixed cost base. The hospital acquisitions in Colombia made an additional contribution.

Net income1 decreased by 2% (-1% in constant currency) to €173 million (Q1/20: €176 million).

Operating cash flow increased to €215 million (Q1/20: €145 million) with a margin of 8.1% (Q1/20: 5.9%), mainly due to working capital improvements driven by cash collections.

For FY/21, Fresenius Helios confirms its outlook and expects organic sales2 growth in a low-to-mid single-digit percentage range and constant currency EBIT3 growth in a mid-to-high single-digit percentage range. Both sales and EBIT outlook include expected COVID-19 effects.

1 Net income attributable to shareholders of Fresenius SE & Co. KGaA

2 FY/20 base: €9,818 million

3 FY/20 base: €1,025 million; FY/21 before special items

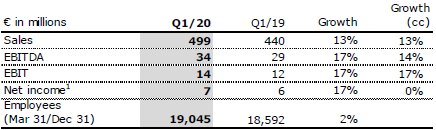

Fresenius Vamed

Fresenius Vamed manages projects and provides services for hospitals and other health care facilities worldwide and is a leading post-acute care provider in Central Europe. The portfolio ranges along the entire value chain: from project development, planning, and turnkey construction, via maintenance and technical management to total operational management.

• Continued significant negative COVID-19 impact

• Project business marked by COVID-19 related delays, cancellations and global supply chain restraints

• Rehabilitation business remains impacted by fewer elective surgeries

• Technical high-end service business remains robust

Sales decreased by 4% (-4% in constant currency) to €477 million (Q1/20: €499 million). Organic growth was -4%.

Sales in the service business increased by 2% (2% in constant currency) to €363 million (Q1/20: €357 million). Sales in the project business decreased by 20% (-20% in constant currency) to €114 million (Q1/20: €142 million), driven by postponements and cancellations of projects.

EBIT decreased by 129% (-129% in constant currency) to -€4 million (Q1/20: €14 million) with an EBIT margin of -0.8% (Q1/20: 2.8%). Large parts of the post-acute care clinic capacities were left partially empty given a generally lower intake of elective surgery patients from acute-care hospitals. Health-authority-induced restrictions or even closures of facilities also had a negative effect. In the project business, project delays and global supply chain restraints triggered incremental expenses.

1 Net income attributable to shareholders of VAMED AG

Net income1 decreased to -€7 million (Q1/20: €7 million).

Order intake was €138 million (Q1/20: €124 million). As of March 31, 2021, order backlog was at €3,082 million (December 31, 2020: €3,055 million). Order intake continued to be marked by COVID-19 related cancellations and project delays.

Operating cash flow decreased to -€44 million (Q1/20: -€20 million) with a margin of -9.2% (Q1/20: -4.0%), mainly related to the lower net income contribution.

For FY/21, Fresenius Vamed confirms its outlook and expects organic sales2 growth in a mid-to-high single-digit percentage range and EBIT3 to grow to a high double-digit Euro million amount. Both sales and EBIT outlook include expected negative COVID-19 effects.

1 Net income attributable to shareholders of VAMED AG

2 FY/20 base: €2,068 million

3 FY/20 base: €29 million; FY/21 before special items

Conference Call

As part of the publication of the results for Q1/2021, a conference call will be held on May 6, 2021 at 1:30 p.m. CEDT (7:30 a.m. EDT). All investors are cordially invited to follow the conference call in a live broadcast over the Internet at www.fresenius.com/investors. Following the call, a replay will be available on our website.

For additional information on the performance indicators used please refer to our website https://www.fresenius.com/alternative-performance-measures.

This release contains forward-looking statements that are subject to various risks and uncertainties. Future results could differ materially from those described in these forward-looking statements due to certain factors, e.g. changes in business, economic and competitive conditions, regulatory reforms, results of clinical trials, foreign exchange rate fluctuations, uncertainties in litigation or investigative proceedings, and the availability of financing. Fresenius does not undertake any responsibility to update the forward-looking statements in this release.

- Preliminary guidance for 2021 confirmed

- Strategic roadmap for accelerated growth through 2023 and beyond

- Group-wide initiatives to improve efficiency and profitability in preparation

- Medium-term growth targets confirmed

- 28th consecutive dividend increase proposed

If no timeframe is specified, information refers to Q4/2020 2020 and 2019 according to IFRS 16

1 Before special items

2 Net income attributable to shareholders of Fresenius SE & Co. KGaA

For a detailed overview of special items please see the reconciliation tables in the PDF document.

Stephan Sturm, CEO of Fresenius, said:” The pandemic year 2020 showed emphatically the importance of forward-thinking, effective and efficient healthcare. Fresenius is making a vital contribution here, in many different areas of medicine. This year, the pandemic will again present us with a number of challenges, making it even more important that we increase efficiency in order to improve our cost base. Beyond our established businesses, we will also expand in important growth areas including biosimilars, digital healthcare, home dialysis and fertility medicine. By doing so, we are laying the foundations for more dynamic growth in the coming years. Even though the pandemic and its consequences are keeping us busy right now, we are already looking ahead and setting the course for the medicine of the future. In this way, we are also securing our company’s sustainable economic success.”

FY/21 Group guidance

For FY/21, Fresenius projects sales growth1 in a low to mid-single-digit percentage range and at least broadly stable net income2,3 year-over-year, both in constant currency. Implicitly, net income2 for the Group excluding Fresenius Medical Care is expected to grow in a mid-to high single digit percentage range in constant currency. Fresenius projects net debt/EBITDA4 to be around the top-end of the self-imposed target corridor of 3.0x to 3.5x by the end of FY/21.

COVID-19 assumptions for guidance FY/21

COVID-19 will continue to impact Fresenius’ operations in 2021. Current burdens and constraints caused by COVID-19 are expected to recede only in H2/21. The expected improvement in the Group’s relevant business environment from H2/21 is heavily dependent on continuously increasing levels of vaccination coverage in Fresenius’ relevant markets. These assumptions are subject to considerable uncertainty.

Fresenius closely monitors the development of COVID-19 case numbers, and the associated various containment measures being enacted in many of the Company’s relevant markets. A possible significant deterioration of the situation associated with further containment measures that could have a significant and direct impact on the health care sector without any appropriate compensation is not reflected in the Group’s FY/21 guidance.

1 FY/20 base: €36,277 million

2 Net income attributable to shareholders of Fresenius SE & Co. KGaA

3 FY/20 base: €1,796 million; before special items; FY/21: before special items

4 At LTM average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures; excluding further potential acquisitions; before special items

For a detailed overview of special items please see the reconciliation tables in the PDF document.

Efficiency and cost saving programs

COVID-19 has led and will lead to a shortfall relative to our original expectations in FY/20 and FY/21 as well as to ongoing incremental uncertainty. Fresenius is hence planning to launch group-wide strategic efficiency initiatives to further safeguard the confirmed medium-term targets and sustainably enhance profitability. These initiatives are expected to consist of operational excellence and cost-saving measures, targeted strengthening of future growth areas and portfolio optimizations. The operational excellence and cost-saving measures are targeted to result in cost savings of at least €100 million p.a. after tax and minority interest in 2023 with some further potential to increase thereafter. We anticipate that achieving these sustainable efficiencies will require significant up-front expenses. On average for the years 2021 to 2023, those expenses are expected to be in the order of magnitude of €100 million p.a. after tax and minority interest. They will be classified as special items. Further information will be provided during our Q1 earnings call on May 6, 2021.

Growth targets for 2020 – 2023 confirmed

Fresenius continues to expect Group sales to grow organically with a compounded annual growth rate (CAGR) of 4% to 7% during 2020 to 2023. Group net income1,2 is projected to increase organically with a CAGR of 5% to 9% during 2020 to 2023. Fresenius expects its sales growth and efficiency improvement initiatives as well as Fresenius Kabi’s biosimilars business to drive an acceleration of Group earnings growth over that period. Small and medium-sized acquisitions are expected to contribute an incremental CAGR of approx. 1%-point to both sales and net income growth.

28th consecutive dividend increase proposed

The Management Board of Fresenius will propose to the Supervisory Board a dividend increase of 5% to €0.88 per share for FY/20 (FY/19: €0.84). Provided the proposal is approved by the Supervisory Board and the Annual General Meeting, this will be the 28th consecutive dividend increase.

1 Net income attributable to shareholders of Fresenius SE & Co. KGaA

2 Before special items

For a detailed overview of special items please see the reconciliation tables in the PDF document.

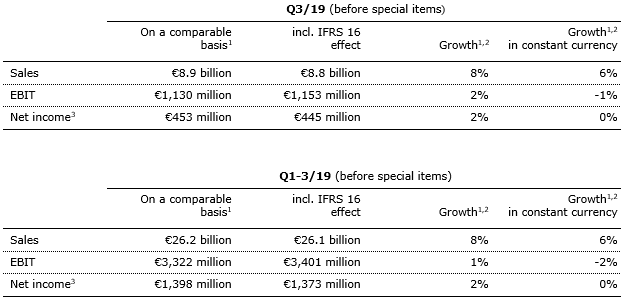

5% sales growth in constant currency

Group sales remained on prior year’s level (increased by 5% in constant currency) at €9,304 million (Q4/19: €9,311 million). Organic growth was 2%. Acquisitions/ divestitures contributed net 3% to growth. Currency translation reduced sales growth by 5%. Excluding estimated COVID-19 effects1, Group sales growth would have been 7% to 8% in constant currency.

In FY/20, Group sales increased by 2% (5% in constant currency) to €36,277 million (FY/19: €35,409 million). Organic growth was 3%. Acquisitions/divestitures contributed net 2% to sales growth. Currency translation reduced sales growth by 3%. Excluding estimated COVID-19 effects1, Group sales growth would have been 7% to 8% in constant currency.

2% net income2,3 growth in constant currency

Group EBITDA before special items decreased by 3% (increased by 3% in constant currency) to €1,886 million (Q4/192: €1,937 million). Reported Group EBITDA was €1,854 million (Q4/19: €1,937 million).

In FY/20, Group EBITDA before special items remained on prior year’s level (increased by 2% in constant currency) at €7,132 million (FY/192: €7,104 million). Reported Group EBITDA was €7,100 million (FY/19: €7,083 million).

Group EBIT before special items decreased by 3% (increased by 2% in constant currency) to €1,251 million (Q4/192: €1,287 million). The constant currency increase is due to the positive development at Fresenius Medical Care and Fresenius Helios. Missing contributions from elective procedures, volume headwinds leading to underutilized production capacities, headwinds at Fresenius Kabi North America, COVID-19 related project delays at Fresenius Vamed as well as Group-wide incremental COVID-19 related expenses weighed on EBIT. The EBIT margin before special items was 13.4% (Q4/192: 13.8%). Reported Group EBIT was €1,024 million (Q4/19: €1,269 million). In FY/20, Group EBIT before special items decreased by 2% (0% in constant currency) to €4,612 million (FY/192: €4,688 million). The EBIT margin before special items was 12.7% (FY/192: 13.2%). Higher levels of investments in recent years triggered incremental depreciation charges. Reported Group EBIT was €4,385 million (FY/19: €4,631 million).

Group net interest before special items improved to -€159 million (Q4/192: -€182 million) mainly due to successful refinancing activities, lower interest rates as well as currency translation effects. Reported Group net interest improved to -€156 million (Q4/19: -€184 million).

1 For estimated COVID-19 effects in Q4/20 and FY/20 please see table on page 18 in the PDF document.

2 Before special items

3 Net income attributable to shareholders of Fresenius SE & Co. KGaA

For a detailed overview of special items please see the reconciliation tables in the PDF document.

In FY/20, Group net interest before special items improved to -€654 million (FY/191: - €714 million) while reported Group net interest improved to -€659 million (FY/19: -€719 million).

The Group tax rate before special items was 24.1% (Q4/191: 23.8%) and the reported Group tax rate was 29.4% (Q4/19: 23.0%). The increase is due to a not tax deductible €195 million impairment of goodwill and tradenames in the Latin America segment at Fresenius Medical Care. In FY/20, the Group tax rate before special items was 23.1% (FY/191: 23.3%) and the reported Group tax rate was 24.2% (FY/19: 22.6%).

Noncontrolling interests before special items were €335 million (Q4/191: €336 million) of which 93% were attributable to the noncontrolling interests in Fresenius Medical Care. Reported noncontrolling interests were €203 million (Q4/19 reported: €320 million). In FY/20, noncontrolling interests before special items were €1,248 million (FY/191: €1,170 million) of which 96% were attributable to the noncontrolling interests in Fresenius Medical Care. Reported noncontrolling interests were €1,116 million (FY/19 reported: €1,146 million).

Group net income2 before special items decreased by 2% (increased by 2% in constant currency) to €494 million (Q4/19: €506 million). Excluding estimated COVID-19 effects3, Group net income2 before special items would have grown 3% to 7% in constant currency. Reported Group net income2 decreased to €410 million (Q4/19: €515 million). The decrease is mainly due to an impairment of goodwill and tradenames in the Latin America segment at Fresenius Medical Care and the increased valuation of the biosimilars contingent purchase price liabilities at Fresenius Kabi. In FY/20, Group net income2 before special items decreased by 4% (-3% in constant currency) to €1,796 million (FY/191: €1,879 million). Excluding estimated COVID-19 effects3, Group net income2 before special items would have grown 2% to 6% in constant currency. Reported Group net income2 decreased to €1,707 million (FY/19: €1,883 million).

Earnings per share2 before special items decreased by 2% (increased by 2% in constant currency) to €0.88 (Q4/191: €0.90). Reported earnings per share2 were €0.73 (Q4/19: €0.92). In FY/20, earnings per share2 before special items decreased by 4% (-3% in constant currency) to €3.22 (FY/191: €3.37). Reported earnings per share2 were €3.06 (FY/191: €3.38).

1 Before special items

2 Net income attributable to shareholders of Fresenius SE & Co. KGaA

3 For estimated COVID-19 effects in Q4/20 and FY/20 please see table on page 18 in the PDF document.

For a detailed overview of special items please see the reconciliation tables in the PDF document.

Continued investment in growth

Spending on property, plant and equipment was €856 million corresponding to 9% of sales (Q4/19: €871 million; 9% of sales). These investments served primarily for the modernization and expansion of dialysis clinics, production facilities as well as hospitals and day clinics. Despite the COVID-19 pandemic, Fresenius has been largely able to continue its investment programs. In FY/20, spending on property, plant and equipment was €2,398 million corresponding to 7% of sales (FY/19: €2,463 million; 7% of sales).

Total acquisition spending was €251 million (Q4/19: €331 million). In FY/20, total acquisition spending was €902 million, mainly for the purchase of hospitals by Fresenius Helios in Germany and Colombia (FY/19: €2,623 million, mainly for the acquisition of NxStage by Fresenius Medical Care).

Good cash flow development

Group operating cash flow increased to €1,390 million (Q4/19: €1,286 million) with a margin of 14.9% (Q4/19: 13.8%). Free cash flow before acquisitions and dividends increased to €590 million (Q4/19: €442 million). Free cash flow after acquisitions and dividends increased to €329 million (Q4/19: €89 million).

In FY/20, Group operating cash flow increased to €6,549 million (FY/19: €4,263 million) with a margin of 18.1% (FY/19: 12.0%). The increase was largely driven by Fresenius Medical Care due to the U.S. federal relief funding and advanced payments under the Coronavirus Aid, Relief and Economic Security Act (CARES Act) as well as by the shorter payment periods of the COVID-19 governmental compensation and reimbursement scheme for Helios Germany. Also excluding these COVID-19 effects, Group operating cash flow would have grown year-over-year. Free cash flow before acquisitions and dividends increased to €4,183 million (FY/19: €1,830 million). Free cash flow after acquisitions and dividends increased to €2,478 million (FY/19: -€1,545 million, driven by Fresenius Medical Care’s acquisition of NxStage).

Solid balance sheet structure

Group total assets decreased by 1% (increased by 5% in constant currency) to €66,646 million (Dec. 31, 2019: €67,006 million). The decrease is mainly due to currency translation effects outweighing the expansion of business activities. Current assets increased by 3% (10% in constant currency) to €15,772 million (Dec. 31, 2019: €15,264 million), mainly driven by the increase of cash and cash equivalents. Non-current assets decreased by 2% (increased by 3% in constant currency) to €50,874 million (Dec. 31, 2019: €51,742 million).

Total shareholders’ equity decreased by 2% (increased by 6% in constant currency) to €26,023 million (Dec. 31, 2019: €26,580 million). The equity ratio was 39.0% (Dec. 31, 2019: 39.7%).

Group debt decreased by 5% (-2% in constant currency) to €25,913 million (Dec. 31, 2019: € 27,258 million). Group net debt decreased by 6% (-4% in constant currency) to € 24,076 million (Dec. 31, 2019: € 25,604 million), driven by the exceptional cash flow development.

As of December 31, 2020, the net debt/EBITDA ratio improved to 3.44x1,2 (Dec. 31, 2019: 3.61x1,2) driven by the exceptional cash flow development, despite COVID-19 effects weighing on EBITDA.

1 At LTM average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures

2 Before special items

For a detailed overview of special items please see the reconciliation tables on pages 20-22 in the PDF document.

Business Segments

Fresenius Medical Care (Financial data according to Fresenius Medical Care press release)

Fresenius Medical Care is the world's largest provider of products and services for individuals with renal diseases. As of December 31, 2020, Fresenius Medical Care was treating 346,553 patients in 4,092 dialysis clinics. Along with its core business, the Renal Care Continuum, the company focuses on expanding in complementary areas and in the field of critical care.

- 2020 financial targets achieved: 5% revenue and 12% net income growth

- Reported earnings in Q4 negatively impacted by impairment in the Latin America region and accelerated excess mortality due to COVID-19

- Growth in home dialysis on track

Sales of Fresenius Medical Care decreased by 4% (increased by 4% in constant currency) to €4,400 million (Q4/19: €4,580 million). Thus, currency translation had a negative effect of 8%. Organic growth was 1%. Acquisitions/divestitures contributed net 3% to growth. In FY/20, Fresenius Medical Care increased sales by 2% (5% in constant currency) to €17,859 million (FY/19: €17,477 million). Thus, currency translation had a negative effect of 3%. Organic growth was 3%. Acquisitions/divestitures contributed net 2% to growth.

Reported EBIT decreased by 25% (-18% in constant currency) to €462 million (Q4/19: €616 million). The decrease was mainly due to a macro-economic driven impairment of goodwill and tradenames in the Latin America segment, unfavorable COVID-19 effects and a lower reimbursement for calcimimetics. The reported EBIT margin was 10.5% (Q4/19: 13.5%). EBIT on an adjusted basis decreased by 1% (increased by 5% in constant currency) to €657 million (Q4/19: €663 million). The EBIT margin on an adjusted basis was 14.9% (Q4/19: 14.5%).

In FY/20, reported EBIT increased by 2% (4% in constant currency) to €2,304 million (FY/19: €2,270 million). The reported EBIT margin was 12.9% (FY/19: 13.0%). EBIT on an adjusted basis increased by 6% (8% in constant currency) to €2,499 million (FY/19: €2,356 million). The EBIT margin on an adjusted basis was 14.0% (FY/19: 13.5%).

1 Before special items

2 Net income attributable to shareholders of Fresenius Medical Care AG & Co. KGaA

For a detailed overview of special items please see the reconciliation tables on pages 20-22 in the PDF document.

Reported net income1 decreased by 48% (-43% in constant currency) to €177 million (Q4/19: €343 million) and increased on an adjusted basis by 1% (6% in constant currency) to €372 million (Q4/19: €368 million). In FY/20, reported net income1 decreased by 3% (-1% in constant currency) to €1,164 million (FY/19: €1,200 million) and increased on an adjusted basis by 10% (12% in constant currency) to €1,359 million (FY/19: €1,236 million).

Operating cash flow was €584 million (Q4/19: €771 million) with a margin of 13.3% (Q4/19: 16.8%). In FY/20, operating cash flow was €4,233 million (FY/19: €2,567 million) with a margin of 23.7% (FY/19: 14.7%). The increase was largely driven by the U.S. federal relief funding and advanced payments under the CARES Act and other COVID-19 relief, as well as working capital improvements driven by cash collections.

For FY/21, Fresenius Medical Care expects revenue2 to grow at a low- to mid-single digit percentage range and net income1,3 to decline at a high-teens to mid-twenties percentage range against the higher than expected 2020 base4.

For further information, also on the FME25 program, please see Fresenius Medical Care’s press release at www.freseniusmedicalcare.com.

1 Net income attributable to shareholders of Fresenius Medical Care AG & Co. KGaA

2 FY/20 base: €17,859 million

3 FY/20 base: €1,359 million, before special items; FY/21: before special items

4 These targets are based on the 2020 results excluding the impairment of goodwill and trade names in the Latin America Segment of €195 million. They are inclusive of anticipated COVID-19 effects, in constant currency and exclude special items. Special items include costs related to FME25 and other effects that are unusual in nature and have not been foreseeable or not foreseeable in size or impact at the time of giving guidance.

For a detailed overview of special items please see the reconciliation tables on pages 20-22 in the PDF document.

Fresenius Kabi

Fresenius Kabi offers intravenously administered generic drugs, clinical nutrition and infusion therapies for seriously and chronically ill patients in the hospital and outpatient environments. The company is also a leading supplier of medical devices and transfusion technology products. In the biosimilars business, Fresenius Kabi develops products with a focus on oncology and autoimmune diseases.

- In North America fewer elective treatments, competitive pressure and temporary manufacturing issues outweighed extra demand for COVID-19 related products

- Europe showed strong organic sales growth in Q4 primarily based on extra demand for COVID-19 related products; China with healthy organic growth

- Strong EBIT growth in Emerging Markets with positive development in China only partially compensates EBIT decrease in North America

Sales increased by 3% (8% in constant currency) to €1,815 million (Q4/19: €1,766 million). Organic growth was 7%. Negative currency translation effects of 5% were mainly related to weakness of the US dollar, the Brazilian real and the Argentinian peso. Estimated COVID-19 effects made a slight positive contribution to sales growth. In FY/20, sales increased by 1% (4% in constant currency) to €6,976 million (FY/19: €6,919 million). Organic growth was 4%. Negative currency translation effects of 3% were mainly related to the weakness of the US dollar, the Brazilian real and the Argentinian peso. Estimated COVID-19 effects slightly reduced sales growth.

Sales in North America decreased by 10% (organic growth: -3%) to €549 million (Q4/19: €609 million). The decrease was driven by fewer elective treatments, supply constraints for certain products due to temporary manufacturing issues and competitive pressure, which outweighed extra demand for COVID-19 related products. In FY/20, sales in North America decreased by 2% (organic growth: 0%) to €2,376 million (FY/19: €2,424 million). Sales in Europe increased by 13% (organic growth: 9%) to €680 million (Q4/19: €604 million) mainly due to increased demand for COVID-19 related products. In FY/20, sales in Europe increased by 6% (organic growth: 6%) to €2,458 million (FY/19: €2,313 million). Sales in Asia-Pacific increased by 11% (organic growth: 14%) to €428 million (Q4/19: €385 million). While China saw a solid recovery based on increasing elective procedures, other Asian markets were lagging behind. In FY/20, sales in Asia-Pacific decreased by 1% (organic growth: 1%) to €1,497 million (FY/19: €1,506 million). Sales in Latin America/Africa decreased by 6% (organic growth: 16%) to €158 million (Q4/19: €168 million). In FY/20, sales in Latin America/Africa decreased by 5% (organic growth: 17%) to €645 million (FY/19: €676 million).

1 Before special items

2 Net income attributable to shareholders of Fresenius SE & Co. KGaA

For a detailed overview of special items please see the reconciliation tables on pages 20-22 in the PDF document.

EBIT before special items decreased by 17% (-10% in constant currency) to €236 million (Q4/191: €285 million) with an EBIT margin before special items of 13.0% (Q4/191:16.1%). The decline is driven by headwinds leading to some underutilized production capacities in the US, coupled with selective supply constraints due to temporary manufacturing issues, incremental COVID-19 related expenses, competitive pressure, a negative effect due to the bankruptcy of a customer as well as planned SG&A spending ahead of the launch of the company’s first US biosimilar. Lower corporate costs due to travel restrictions and phasing of projects partially offset the decline. Estimated COVID-19 effects had a moderate negative impact on EBIT growth in Q4/20. In FY/20, EBIT before special items decreased by 9% (-6% in constant currency) to €1,095 million (FY/191: €1,205 million) with an EBIT margin before special items of 15.7% (FY/191: 17.4%). Estimated COVID-19 effects had an insignificant impact on EBIT growth in FY/20.

Net income1,2 decreased by 19% (-11% in constant currency) to €148 million (Q4/191: €183 million). In FY/20, net income1,2 decreased by 8% (-5% in constant currency) to €730 million (FY/191: €797 million).

Operating cash flow increased to €307 million (Q4/19: €291 million) with a margin of 16.9% (Q4/19: 16.5%). In FY/20, operating cash flow increased by 11% to €1,143 million (FY/19: €1,028 million) with a margin of 16.4% (FY/19: 14.9%) due to the favorable working capital development.

For FY/21, Fresenius Kabi expects organic sales3 growth in a low to mid-single digit percentage range. Constant currency EBIT4 is expected to show a stable development up to low single digit percentage growth. Both sales and EBIT outlook include expected COVID-19 effects.

1 Before special items

2 Net income attributable to shareholders of Fresenius SE & Co. KGaA

3 FY/20 base: €6,976 million

4 FY/20 base: €1,095 million, before special items, FY/21: before special items

For a detailed overview of special items please see the reconciliation tables on pages 20-22 in the PDF document.

Fresenius Helios

Fresenius Helios is Europe's leading private hospital operator. The company comprises Helios Germany and Helios Spain (Quirónsalud). Helios Germany operates 89 hospitals, ~130 outpatient centers and 6 prevention centers. Quirónsalud operates 46 hospitals, 70 outpatient centers and around 300 occupational risk prevention centers. In addition, the company is active in Latin America with 6 hospitals and as a provider of medical diagnostics.

- Recovery of elective procedures in Spain in Q4

- Continued financial support provided by German government throughout Q4

- Helios Spain with strong organic sales and EBIT growth based on catch-up effects additionally fueled by contributions from acquisitions in Latin America

Sales increased by 13% (13% in constant currency) to €2,637 million (Q4/19: €2,344 million). Organic growth was 9%. Acquisitions contributed 4% to sales growth. COVID-19 effects had an insignificant effect on organic growth. In FY/20, sales increased by 6% (7% in constant currency) to €9,818 million (FY/19: €9,234 million). Organic growth was 4%. Acquisitions contributed 3% to sales growth. COVID-19 effects had a slight negative impact on organic growth.

Sales of Helios Germany increased by 11% (organic growth: 8%) to €1,637 million (Q4/19: €1,475 million). In FY/20, sales of Helios Germany increased by 7% (organic growth: 6%) to €6,340 million (FY/19: €5,940 million). COVID-19 effects were mitigated by government financial support and hence had only a slight negative impact on organic growth in both Q4/20 and FY/20.

Sales of Helios Spain increased by 15% (17% in constant currency) to €999 million (Q4/19: €867 million). Organic growth of 11% was driven by a strong recovery of elective procedures and a consistently high level of outpatient treatments. Thus, COVID-19 effects had a moderate positive impact on organic growth in Q4. The hospital acquisitions in Colombia contributed 6% to sales growth. In FY/20, sales of Helios Spain increased by 6% (7% in constant currency) to €3,475 million (FY/19: €3,292 million). Organic growth was 2%. Acquisitions contributed 5% to sales growth. COVID-19 effects had a significant negative impact on organic sales growth.

1 Net income attributable to shareholders of Fresenius SE & Co. KGaA

EBIT of Fresenius Helios increased by 12% (13% in constant currency) to €328 million (Q4/19: €294 million) with an EBIT margin of 12.4% (Q4/19: 12.5%). COVID-19 effects, in particular due to the strong recovery of elective procedures in Spain, had a significant positive effect on EBIT growth in Q4. In FY/20, EBIT of Fresenius Helios remained on prior year’s level (0% in constant currency) at €1,025 million (FY/19: €1,025 million) with an EBIT margin of 10.4% (FY/19: 11.1%). COVID-19 effects had a moderate negative impact on EBIT growth.

EBIT of Helios Germany increased by 10% to €157 million (Q4/19: €143 million) with an EBIT margin of 9.6% (Q4/19: 9.7%). Financial support provided by the German government under revised regulations focusing on regions with high COVID incidences broadly offset additional headwinds as Helios Germany continued to play a crucial role in treating COVID-19 patients. In FY/20, EBIT of Helios Germany increased by 4% to €602 million (FY/19: €577 million) with an EBIT margin of 9.5% (FY/19: 9.7%). Due to the comprehensive financial support provided by the German government, COVID-19 effects had an overall insignificant impact on the EBIT development.

EBIT of Helios Spain increased by 17% (19% in constant currency) to €159 million (Q4/19: €136 million) with an EBIT margin of 15.9% (Q4/19: 15.7%). The growth is driven by a recovery of elective procedures following the government-ordered postponement of planned surgical procedures in Q2, where medically justifiable. Thus, COVID-19 effects had a significant positive effect on EBIT growth in Q4. In FY/20, EBIT of Helios Spain decreased by 5% (-5% in constant currency) to €420 million (FY/19: €443 million) with an EBIT margin of 12.1% (FY/19: 13.5%). COVID-19 effects had a very significant negative impact on EBIT growth with missing or delayed elective procedures and higher expenses amid the comprehensive efforts to combat the pandemic.

Net income1 increased by 14% to €225 million (Q4/19: €197 million). In FY/20, net income1 remained on prior year’s level at €666 million (FY/19: €664 million).

Operating cash flow increased to €434 million (Q4/19: €226 million) with a margin of 16.5% (Q4/19: 9.6%), driven by phasing of payments under the German law to ease the financial burden on hospitals. In FY/20, operating cash flow increased to €1,149 million (FY/19: €733 million) with a margin of 11.7% (FY/19: 7.9%).

1 Net income attributable to shareholders of Fresenius SE & Co. KGaA

For FY/21, Fresenius Helios expects organic sales1 growth in a low to mid-single digit percentage range and constant currency EBIT2 growth in a mid to high single digit percentage range. Both sales and EBIT outlook include expected COVID-19 effects.

1 FY/20 base: €9,818 million

2 FY/20 base: €1,025 million; FY/21 before special items

Fresenius Vamed

Fresenius Vamed manages projects and provides services for hospitals and other health care facilities worldwide and is a leading post-acute care provider in Central Europe. The portfolio ranges along the entire value chain: from project development, planning, and turnkey construction, via maintenance and technical management to total operational management.

- Significant COVID-19 impact in the project business related to delays, cancellations and global supply chain restraints continued

- Good order intake in Q4 indicates first signs of recovery in project business

- Rehabilitation business continued to be impacted by less demand for rehabilitation treatments and postponements of elective surgeries; technical service business remained robust

Sales decreased by 22% (-22% in constant currency) to €577 million (Q4/19: €737 million). Organic growth was -22%. Acquisitions did not contribute to growth. Estimated COVID-19 effects had a very significant negative impact on growth. In FY/20, sales decreased by 6% (-6% in constant currency) to €2,068 million (FY/19: €2,206 million). Organic growth was -8%. Acquisitions contributed 2% to growth. Estimated COVID-19 effects had a very significant negative impact on growth.

Sales in the service business decreased by 1% to €372 million (Q4/19: €374 million).

Sales in the project business decreased by 44% to €205 million (Q4/19: €363 million), driven by postponements and cancellations of projects. In FY/20, sales in the service business grew by 3% to €1,435 million (FY/19: €1,399 million). Sales in the project business decreased by 22% to €633 million (FY/19: €807 million).

1 Net income attributable to shareholders of VAMED AG

EBIT decreased by 42% (-42% in constant currency) to €39 million (Q4/19: €67 million) with an EBIT margin of 6.8% (Q4/19: 9.1%). Estimated COVID-19 effects had a very significant negative impact on EBIT. Capacities in the post-acute care clinics were left partially empty given a generally lower intake of elective surgery patients from acute-care hospitals. Authority-instigated restrictions or even closures of individual facilities also had a negative effect. In the project business, project delays and global supply chain restraints triggered incremental expenses. In FY/20, EBIT decreased by 78% (-79% in constant currency) to €29 million (FY/19: €134 million) with an EBIT margin of 1.4% (FY/19: 6.1%). Estimated COVID-19 effects had a very significant negative impact on EBIT.

Net income1 decreased to €25 million (Q4/19: €44 million). In FY/20, net income1 decreased to €2 million (FY/19: €83 million).

Order intake was €648 million in Q4/20 (Q4/19: €576 million) and €1,010 million in FY/20 (FY/19: €1,314 million). As of December 31, 2020, order backlog was at €3,055 million (December 31, 2019: €2,865 million). Order intake and order backlog were marked by COVID-19 related cancellations and project delays.

Operating cash flow increased to €74 million (Q4/19: €0 million) with a margin of 12.8% (Q4/19: 0%), driven by a favorable working capital development mainly related to pre-payments. In FY/20, operating cash flow increased to €78 million (FY/19: -€17 million) with a margin of 3.8% (FY/19: -0.8%).

For FY/21, Fresenius Vamed expects organic sales2 growth in a mid to high single digit percentage range and EBIT3 to grow to a high double-digit euro million amount. Both sales and EBIT outlook include expected negative COVID-19 effects.

1 Net income attributable to shareholders of VAMED AG

2 FY/20 base: €2,068 million

3 FY/20 base: €29 million; FY/21 before special items

Conference Call

As part of the publication of the results for FY 2020, a conference call will be held on February 23, 2021 at 1:30 p.m. CET (7:30 a.m. EST). All investors are cordially invited to follow the conference call in a live broadcast over the Internet at www.fresenius.com/investors. Following the call, a replay will be available on our website.

For additional information on the performance indicators used please refer to our website https://www.fresenius.com/alternative-performance-measures.

This release contains forward-looking statements that are subject to various risks and uncertainties. Future results could differ materially from those described in these forward-looking statements due to certain factors, e.g. changes in business, economic and competitive conditions, regulatory reforms, results of clinical trials, foreign exchange rate fluctuations, uncertainties in litigation or investigative proceedings, and the availability of financing. Fresenius does not undertake any responsibility to update the forward-looking statements in this release.

Fresenius has proven the resilience of its business model in a challenging environment in FY/20. Based on preliminary and unaudited results, Fresenius achieved its sales and net income1 guidance including COVID-19 effects. Fresenius expected sales growth2 of 3% to 6% and a net income1,3 development at the lower end of a range of -4% to +1%, both in constant currency.

Excluding estimated COVID-19 effects, the Group performed very well against its original guidance ranges of 4% to 7% sales growth and 1% to 5% net income1,3 growth, both in constant currency.

The previously flagged risk of an impairment of goodwill and tradenames at Fresenius Medical Care Latin America, as a consequence of the macro-economic downturn and increasing risk adjustment rates for certain countries in Latin America, has materialized and impacts reported FY/20 Group net income1.

Fresenius firmly intends to extend its track record of 27 consecutive dividend increases.

1 Net income attributable to shareholders of Fresenius SE & Co. KGaA

2 FY/19 base: €35,409 million

3 FY/19 base: €1,879 million; before special items (transaction-related expenses, revaluations of biosimilars contingent purchase price liabilities, gain related to divestitures of Care Coordination activities at FMC, expenses associated with the cost optimization program at FMC); FY/20: before special items

Current expectations for FY/21

Based on the current status of the Group’s financial planning process and assuming that the current burdens and constraints caused by the COVID-19 pandemic only begin to recede in the second half of the year, Fresenius targets healthy sales growth1 and at least broadly stable net income2 year over year in FY/21.

The FY/21 earnings are, hence, expected to be very meaningfully impacted by COVID-19 effects. In particular, the significant acceleration of mortality among dialysis patients due to COVID-19 is expected to have a material impact on Fresenius Medical Care’s results and hence on Fresenius Group’s net income2 growth.

Fresenius continues to monitor and analyse the COVID-19 pandemic and associated implications, including the availability of government support, as well as pace, adoption and effectiveness of vaccinations, and will comment further as part of its FY/20 earnings call.

Stephan Sturm, CEO of Fresenius, said: “In 2020, we coped well with the burdens and restrictions caused by the pandemic. For 2021, I am confident that our Company will continue to perform solidly - despite the COVID-related impact on earnings anticipated at Fresenius Medical Care. Our underlying growth prospects remain robust. Fresenius continues to make a significant contribution to overcoming this global health crisis as swiftly as possible. Since the beginning of the pandemic, we have made an enormous effort to ensure that our patients continue to receive excellent medical care and that they – as well as our employees – are protected from infection. For this to succeed, close cooperation between all partners in the healthcare sector is needed more than ever, backed by political support. For instance, the conditions must be created to vaccinate the particularly vulnerable group of dialysis patients with high priority. We must not forget: Behind the numbers are people’s fates. Every single patient, every life counts.”

1 In constant currency

2 Net income attributable to shareholders of Fresenius SE & Co. KGaA; in constant currency; before any special items and any one-time expenses related to likely efficiency and cost saving programs

Efficiency and cost saving programs

To counter the current challenging business environment, Fresenius will launch additional initiatives across the Group to further improve profitability. More details will be announced with the publication of FY/20 results.

Group medium-term targets

The current information and assumptions do not trigger a revision of Fresenius’ medium-term growth targets, which were set before the COVID-19 pandemic emerged. As usual, the company will give an update on its medium-term expectations with the publication of its FY/20 results.

Next steps

Fresenius will announce more detailed FY/21 financial guidance with the release of its FY/20 results on February 23, 2021.

For additional information on the performance indicators used please refer to our website at https://www.fresenius.com/alternative-performance-measures.

This release contains forward-looking statements that are subject to various risks and uncertainties. Future results could differ materially from those described in these forward-looking statements due to certain factors, e.g. changes in business, economic and competitive conditions, regulatory reforms, results of clinical trials, foreign exchange rate fluctuations, uncertainties in litigation or investigative proceedings, and the availability of financing. Fresenius does not undertake any responsibility to update the forward-looking statements in this release.

- Fresenius Medical Care with continued strong earnings growth in constant currency

- Fresenius Kabi showed a recovery in Europe and return to growth in China whilst headwinds weigh on North American business

- Helios Germany with sales growth in Q3 due to recovery of elective procedures; Helios Spain with significant growth based on catch-up effects

- Fresenius Vamed continues to be heavily impacted by COVID-19 related project delays, high-end technical service remained robust

If no timeframe is specified, information refers to Q3/2020; 2020 and 2019 according to IFRS 16

1 Before special items

2 Net income attributable to shareholders of Fresenius SE & Co. KGaA

For a detailed overview of special items please see the reconciliation tables on pages 17-19 in the PDF document.

Stephan Sturm, CEO of Fresenius, said: "Fresenius remains stable and resilient, and was able to show it once again in the third quarter. Despite the ongoing and in some cases drastic restrictions caused by COVID-19, our patients could continue to rely on and benefit from our care. Fresenius is also reliable, in terms of business development: We forecasted that after a second quarter impacted by the lockdowns our sales and earnings would resume their positive trajectory – and they did just that. Despite the coronavirus, we were even able to achieve a strong increase in sales over last year’s third quarter. Our quarterly earnings of €427 million are also robust. We are well prepared for the challenges that the pandemic will pose to us over the coming months. As a result, I remain confident that we will reach our 2020 targets and continue our healthy growth in the coming years."

FY/20 Group guidance

Based on the Group’s solid business development in Q1-3/20, Fresenius confirms its sales and net income guidance for 2020 including estimated COVID-19 effects. Fresenius projects sales growth1 of 3% to 6% in constant currency. Net income2,3 is expected to develop in a range of - 4% to +1%.

Fresenius projects net debt/EBITDA4 to be around the top-end of the self-imposed target corridor of 3.0x to 3.5x by the end of FY/20 including estimated COVID-19 effects.

COVID-19 will continue to impact Fresenius’ operations in Q4/20. Fresenius recognizes the increasing COVID-19 case numbers, and the associated various containment measures being enacted in many of the Company’s relevant markets. Thus, the Group’s FY/20 guidance assumes no containment measures that have a significant and direct impact on the health care sector that are not appropriately compensated.

1 FY/19 base: €35,409 million

2 Net income attributable to shareholders of Fresenius SE & Co. KGaA

3 FY/19 base: €1,879 million; before special items (transaction-related expenses, revaluations of biosimilars contingent purchase price liabilities, gain related to divestitures of Care Coordination activities at FMC, expenses associated with the cost optimization program at FMC); FY/20: before special items

4 At LTM average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures; excluding further potential acquisitions; before special items

For a detailed overview of special items please see the reconciliation tables on pages 17-19 in the PDF document.

5% sales growth in constant currency

Group sales increased by 1% (5% in constant currency) to €8,918 million (Q3/19: €8,842 million). Organic sales growth was 3%. Acquisitions/divestitures contributed net 2% to growth. Currency translation had a negative impact on sales growth of 4%. Excluding estimated COVID-19 effects1, Group sales growth would have been 6% to 7%, in constant currency. In Q1-3/20, Group sales increased by 3% (5% in constant currency) to €26,973 million (Q1-3/19: €26,098 million). Organic sales growth was 3%. Acquisitions/divestitures contributed net 2% to growth. Currency translation had a negative impact on sales growth of 2%. Excluding estimated COVID-19 effects1, Group sales growth would have been 7% to 8% in constant currency.

1% net income2,3 growth in constant currency

Group EBITDA decreased by 2% (increased by 2% in constant currency) to €1,729 million (Q3/192: €1,763 million). In Q1-3/20, Group EBITDA increased by 2% (2% in constant currency) to €5,246 million (Q1-3/192: €5,167 million).

Group EBIT decreased by 3% (increased by 1% in constant currency) to €1,113 million (Q3/192: €1,153 million). The missing contribution from elective procedures, volume headwinds leading to underutilized production capacities, COVID-19 related project delays at Fresenius Vamed as well as Group-wide COVID-19 related expenses weighed on EBIT. The EBIT margin was 12.5% (Q3/192: 13.0%). In Q1-3/20, Group EBIT decreased by 1% (0% in constant currency) to €3,361 million (Q1-3/192: €3,401 million). The EBIT margin was 12.5% (Q1-3/192: 13.0%). Following higher levels of investments in recent years, Fresenius sees higher levels of depreciation and amortization in 2020.

Group net interest before special items improved to -€154 million (Q3/19: -€171 million) mainly due to successful refinancing activities, lower interest rates as well as currency translation effects. Reported Group net interest improved to -€154 million (Q3/19: -€172 million). In Q1-3/20, Group net interest before special items improved to -€495 million (Q1-3/19: -€532 million) while reported Group net interest improved to -€503 million (Q1-3/19: -€535 million).

1 For estimated COVID-19 effects in Q3/20 and Q1-3/20 please see table on page 15 in the PDF document.

2 Before special items

3 Net income attributable to shareholders of Fresenius SE & Co. KGaA

For a detailed overview of special items please see the reconciliation tables on pages 17-19 in the PDF document.

The Group tax rate before special items (Q3/19: 23.1%) and the reported Group tax rate (Q3/19: 21.2%) were 22.0%. In Q1-3/20, the Group tax rate before special items (Q1-3/19: 23.1%) and the reported Group tax rate (Q1-3/19: 22.4%) were 22.7%.

Noncontrolling interests before special items and reported noncontrolling interests were €321 million (Q3/19: both €310 million), of which 97% were attributable to the noncontrolling interests in Fresenius Medical Care. In Q1-3/20, noncontrolling interests before special items and reported were €913 million (Q1-3/19 before special items: €834 million; reported €826 million).

Group net income1 before special items decreased by 4% (increased by 1% in constant currency) to €427 million (Q3/19: €445 million). Excluding estimated COVID-19 effects2, net income before special items and in constant currency would have grown 1% to 5%. Reported Group net income1 was €427 million (Q3/19: €444 million). In Q1-3/20, Group net income1 before special items decreased by 5% (-4% in constant currency) to €1,302 million (Q1-3/19: €1,373 million). Excluding estimated COVID-19 effects2, net income before special items and in constant currency would have grown 2% to 6%. Reported Group net income1 was €1,297 million (Q1-3/19: €1,368 million).

Earnings per share1 before special items decreased by 4% (0% in constant currency) to €0.77 (Q3/19: €0.80). Reported earnings per share1 were €0.77 (Q3/19: €0.80). In Q1-3/20, earnings per share1 before special items decreased by 5% (-4% in constant currency) to €2.34 (Q1-3/19: €2.47). Reported earnings per share1 were €2.33 (Q1-3/19: €2.46).

Continued investment in growth

Spending on property, plant and equipment was €521 million corresponding to 6% of sales (Q3/19: €586 million; 7% of sales). These investments served primarily for the modernization and expansion of dialysis clinics, production facilities as well as hospitals, and day clinics. Despite the COVID-19 pandemic, Fresenius has been largely able to continue its investment programs, although there remains some uncertainty on the timing of projects for the remainder of the year. In Q1-3/20, spending on property, plant and equipment was €1,542 million corresponding to 6% of sales (Q1-3/19: €1,592 million; 6% of sales).

Total acquisition spending was €142 million (Q3/19: €135 million). In Q1-3/20, total acquisition spending was €651 million, mainly for the acquisition of three hospitals in Colombia by Fresenius Helios (Q1-3/19: €2,292 million, mainly for the acquisition of NxStage by Fresenius Medical Care).

1 Net income attributable to shareholders of Fresenius SE & Co. KGaA

2 For estimated COVID-19 effects in Q3/20 and Q1-3/20 please see table on page 15 in the PDF document.

For a detailed overview of special items please see the reconciliation tables on pages 17-19 in the PDF document.

Good cash flow development

Group operating cash flow was €1,199 million (Q3/19: €1,483 million) with a margin of 13.4% (Q3/19: 16.8%). Free cash flow before acquisitions and dividends was €682 million (Q3/19: €907 million). Given dividend payment in Q3/20 versus Q2/19, Free cash flow after acquisitions and dividends was -€185 million (Q3/19: €732 million).

In Q1-3/20, Group operating cash flow increased to €5,159 million (Q1-3/19: €2,977 million) with a margin of 19.1% (Q1-3/19: 11.4%). The increase was largely driven by Fresenius Medical Care due to the U.S. federal relief funding and advanced payments under the Coronavirus Aid, Relief and Economic Security Act (CARES Act) as well as by the shorter payment periods of the COVID-19 governmental compensation and reimbursement scheme for Helios Germany. Free cash flow before acquisitions and dividends was €3,593 million (Q1-3/19: €1,388 million). Free cash flow after acquisitions and dividends was €2,149 million (Q1-3/19: -€1,634 million, driven by the acquisition of NxStage by Fresenius Medical Care).

Solid balance sheet structure

Group total assets increased by 2% (5% in constant currency) to €68,321 million (Dec. 31, 2019: €67,006 million). Current assets increased by 10% (15% in constant currency) to €16,833 million (Dec. 31, 2019: €15,264 million), mainly driven by the increase of cash and cash equivalents. Non-current assets remained nearly unchanged (2% in constant currency) at €51,488 million (Dec. 31, 2019: €51,742 million).

Total shareholders’ equity decreased by 1% (increased by 4% in constant currency) to €26,201 million (Dec. 31, 2019: €26,580 million). The equity ratio was 38.3% (Dec. 31, 2019: 39.7%).

Group debt remained nearly unchanged (increased by 1% in constant currency) at €27,171 million (Dec. 31, 2019: € 27,258 million). Group net debt decreased by 4% (-3% in constant currency) to € 24,513 million (Dec. 31, 2019: € 25,604 million), driven by the exceptional cash flow development.

As of September 30, 2020, the net debt/EBITDA ratio improved to 3.45x1,2 (Dec. 31, 2019: 3.61x1,2) driven by the exceptional cash flow development, despite COVID-19 effects weighing on EBITDA.

1 At LTM average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures

2 Before special items

For a detailed overview of special items please see the reconciliation tables on pages 17-19 in the PDF document.

Business Segments

Fresenius Medical Care (Financial data according to Fresenius Medical Care press release)

Fresenius Medical Care is the world's largest provider of products and services for individuals with renal diseases. As of September 30, 2020, Fresenius Medical Care was treating 349,167 patients in 4,073 dialysis clinics. Along with its core business, the company provides related medical services in the field of Care Coordination.

- Solid sales and strong earnings growth at constant currency continues in Q3

- Q3 development impacted by currency headwinds and expected lower reimbursement from calcimimetics

- Guidance for FY/20 confirmed

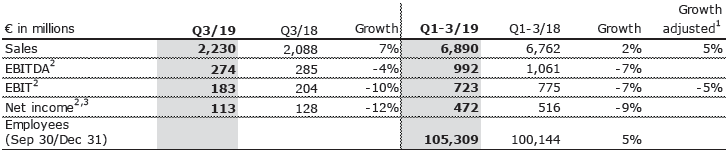

Sales of Fresenius Medical Care remained on prior year’s level (increased by 6% in constant currency) at €4,414 million (Q3/19: €4,419 million). Organic sales growth was 3%. Acquisitions/divestitures contributed net 3% to growth. In Q1-3/20, Fresenius Medical Care increased sales by 4% (6% in constant currency) to €13,459 million (Q1-3/19: €12,897 million). Organic sales growth was 4%.

There were no adjustments to reported EBIT in Q3/20 and Q1-3/20. Reported EBIT increased by 6% (11% in constant currency) to €632 million (Q3/19: €595 million). The reported EBIT margin was 14.3% (Q3/19: 13.5%). The increase in margin was driven by negative prior year earnings effects, an increase in commercial revenue and favorable cost management of pharmaceuticals, offsetting the lower reimbursement for calcimimetics, all in the North America region. EBIT on an adjusted basis increased by 2% (7% in constant currency) to €632 million (Q3/19: €620 million). The EBIT margin on an adjusted basis was 14.3% (Q3/19: 14.0%).

1 Before special items

2 Net income attributable to shareholders of Fresenius Medical Care AG & Co. KGaA

For a detailed overview of special items please see the reconciliation tables on pages 17-19 in the PDF document.

In Q1-3/20, reported EBIT increased by 11% (12% in constant currency) to €1,843 million (Q1-3/19: €1,653 million). The reported EBIT margin was 13.7% (Q1-3/19: 12.8%). EBIT on an adjusted basis increased by 9% (9% in constant currency) to €1,843 million (Q1-3/19: €1,693 million). The EBIT margin on an adjusted basis was 13.7% (Q1-3/19: 13.1%).

There were no adjustments to reported net income in Q3/20 and Q1-3/20. Reported net income1 grew by 6% (11% in constant currency) to €354 million (Q3/19: €333 million) and increased on an adjusted basis by 7% (11% in constant currency) to €354 million (Q3/19: €332 million). In Q1-3/20, reported net income1 grew by 15% (15% in constant currency) to €987 million (Q1-3/19: €857 million) and increased on an adjusted basis by 14% (14% in constant currency) to €987 million (Q1-3/19: €868 million).

Operating cash flow was €746 million (Q3/19: €868 million) with a margin of 16.9% (Q3/19: 19.7%). In Q1-3/20, operating cash flow was €3,649 million (Q1-3/19: €1,796 million) with a margin of 27.1% (Q1-3/19: 13.9%). The increase was largely driven by the U.S. federal relief funding and advanced payments under the CARES Act and other COVID-19 relief, as well as working capital improvements driven by cash collections.

Fresenius Medical Care continues to expect both revenue2 and net income1,3 to grow at a mid to high single digit rate in 2020. These targets are inclusive of anticipated COVID-19 effects, in constant currency and exclude special items4. They are based on the adjusted results 2019, including the effects of the operations of the NxStage acquisition and the IFRS 16 implementation.

For further information, please see Fresenius Medical Care’s press release at www.freseniusmedicalcare.com.

1 Net income attributable to shareholders of Fresenius Medical Care AG & Co. KGaA

2 FY/19 base: €17,477 million

3 FY/19 base: €1,236 million (FY/20: before special items)

4 Special items are effects that are unusual in nature and have not been foreseeable or not foreseeable in size or impact at the time of giving guidance.

For a detailed overview of special items please see the reconciliation tables on pages 17-19 in the PDF document.

Fresenius Kabi

Fresenius Kabi offers intravenously administered generic drugs, clinical nutrition and infusion therapies for seriously and chronically ill patients in the hospital and outpatient environments. The company is also a leading supplier of medical devices and transfusion technology products. In the biosimilars business, Fresenius Kabi develops products with a focus on oncology and autoimmune diseases.

- In North America decreased demand given fewer elective treatments and some supply constraints due to temporary manufacturing issues outweighed extra demand for COVID-19 related products

- China recovery accelerates with elective treatments rebounding nearly to pre-pandemic levels

- Strong EBIT growth in Europe and positive development in China only partially compensates EBIT decrease in North America

- FY/20 guidance confirmed