Credit Relations

Financing Strategy & Targets

Ensure financial flexibility, maintain our investment grade rating, limit refinancing risks and optimize the cost of capital are the main objectives in Fresenius’s financing strategy.

To remain financially flexible, we maintain adequate liquidity headroom. We are committed to our investment grade rating, which provides us with advantages with respect to funding costs, facilitates markets access, and thus contributes to greater financial flexibility overall. Our financing strategy aims at ensuring a stable investment grade rating in the long term.

Refinancing risks are limited due to a balanced maturity profile which is characterized by a broad range of maturities with a high proportion of mid- and long-term debt. We use various financing instruments in a targeted manner to diversify our financing mix and our investor base.

Relevant financing instruments include bonds, Schuldschein Loans and bank loans. In addition, Fresenius maintains a commercial paper program.

Another key objective of Fresenius’ financing strategy is to optimize the cost of capital by employing an adequate mix of equity and debt.

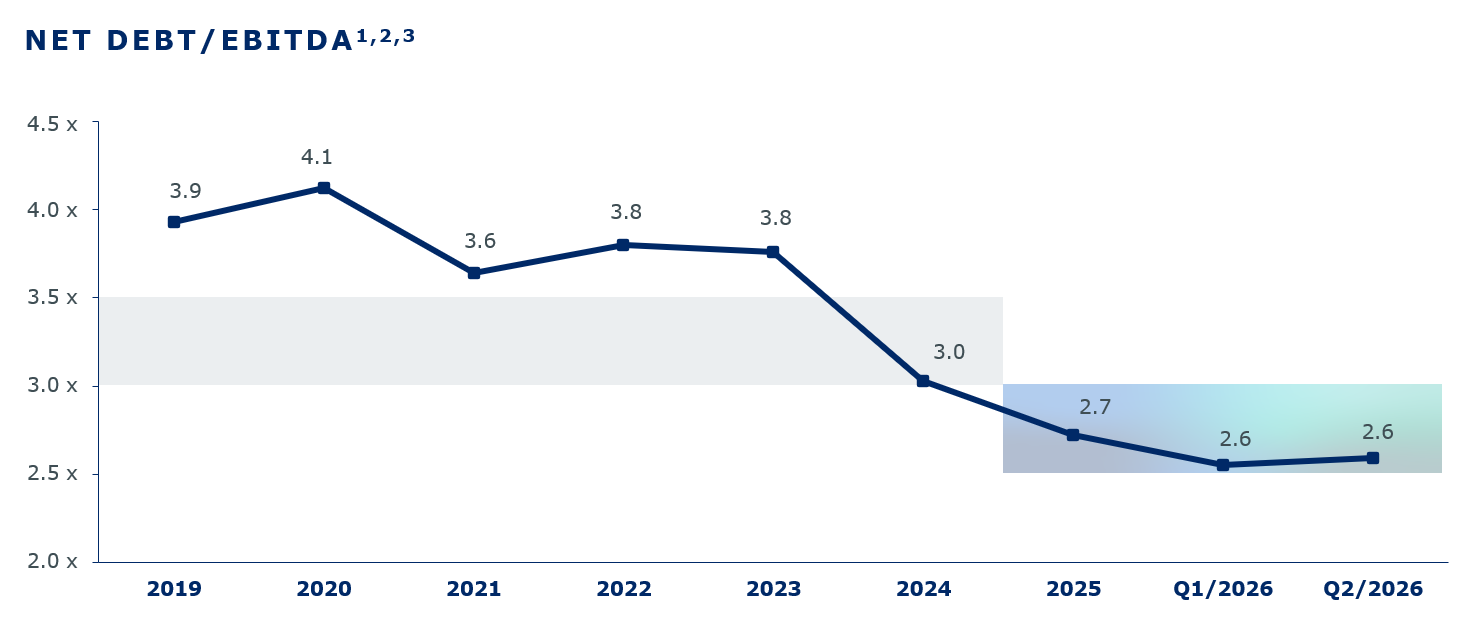

In 2026, adherence to our self-imposed target corridor will continue to be of central importance to us. Our self-imposed target corridor of 2.5 x to 3.0 x allows us to stay financially flexible while solidifying our investment grade rating.

Fresenius Group

1 Prior-year figures have been adjusted due to the deconsolidation of Fresenius Medical Care

2 Before special items

3 At LTM average exchange rates for both net debt and EBITDA; pro forma acquisitions/divestitures; including lease liabilities; including Fresenius Medical Care and Vitrea dividends; net debt adjusted for the valuation effect of the exchangeable bond

Financing Instruments

Bonds

| Issuer | Volume in million | Coupon | Maturity |

|---|---|---|---|

| €500 | 0.375% | 2026 | |

| €750 | 1.625% | 2027 | |

| €750 | 0.75% | 2028 | |

| CHF275 | 2.96% | 2028 | |

| €500 | 2.875% | 2029 | |

| CHF225 | 1.5975% | 2029 | |

| €500 | 5.00% | 2029 | |

| €500 | 2.75% | 2029 | |

| €550 | 2.875% | 2030 | |

| €500 | 5.125% | 2030 | |

| €500 | 3.375% | 2031 | |

| €500 | 1.125% | 2033 | |

| €500 | 3.50% | 2034 | |

| €500 | 3.750% | 2034 | |

| €700 | 2.125% | 2027 | |

| €500 | 0.50% | 2028 | |

| €500 | 0.875% | 2031 | |

| €500 | 3.00% | 2032 |

Schuldschein loans

| Issuer | Volume in million | Interest rate fixed/variable | Maturity |

|---|---|---|---|

Fresenius SE & Co. KGaA | €117 | 0.85% | 2026 |

Fresenius SE & Co. KGaA | €207 | 1.96%/variable | 2027 |

Fresenius SE & Co. KGaA | €101 | 4.62% | 2028 |

Fresenius SE & Co. KGaA | €84 | 1.10% | 2029 |

Fresenius SE & Co. KGaA | €66 | 4.77% | 2030 |

EIB loan

| Issuer | Volume in million | Coupon | Maturity |

|---|---|---|---|

Fresenius SE & Co. KGaA | €400 | variable | 2030 |

The European Investment Bank (EIB) is the biggest multilateral financial institution in the world and one of the largest providers of finance for climate action, providing economic support to sectors that contribute significantly to technological innovation, growth, employment, regional cohesion and environmental sustainability in Europe and beyond.

Fresenius received a €400 million loan in December 2025 to strengthen its European research and development (R&D) activities. The financing is used to support expansion of Fresenius Kabi's manufacturing of medical products and biosimilars in European countries.

The Fresenius SE & Co. KGaA Commercial Paper Program enables Fresenius to issue short-term notes of up to €1.5 bn on the money market. The issuances are made through the European Commercial Paper Program (ECP).

| Issuer: | Fresenius SE & Co. KGaA, Fresenius Finance Ireland plc. |

| Program amount | € 1,500,000,000 |

| Arranger | Commerzbank |

| Dealer | Barclays, Commerzbank, Crédit Agricole, DZ BANK AG, Landesbank Baden-Württemberg, Landesbank Hessen-Thüringen, ING Bank N.V. |

| Issuing and paying agent | Commerzbank |

| Term | up to 1 year less 1 day |

Rating

Fresenius is covered by the leading rating agencies Standard & Poor's, Moody's and Fitch. The following table shows Fresenius SE & Co. KGaA's current ratings.

Rating

| Standard & Poor's | Moody's | Fitch | |

|---|---|---|---|

Corporate Credit Rating | BBB | Baa3 | BBB- |

Outlook | positive | stable | stable |

Contact

Director Investor Relations

T: +49 (0) 6172 608-2486

elisabeth.truckenbrodt@fresenius.com

New information

Related Links

Interactive Tool