- Group organic revenue growth of 9%1,2 to €5.3 billion2 driven by a strong Kabi performance and good organic growth at Helios.

- Strong bottom-line traction with Group EBIT2 increase in constant currency of 9%3 to €552 million and EPS growth of 7%2,3,4.

- Group outlook for fiscal 2024 upgraded; Organic revenue growth1,2 is now expected to grow between 6% to 8% (previous: between 4% to 7%) and EBIT growth2 in constant currency is now targeted to be in the 8 to 11% range (previous: between 6% to 10%).

- Group-wide cost and productivity savings ahead of plan with target for FY/24 already achieved YTD.

- Excellent operating cash flow resulting from focused cash management.

- Deleveraging continued, and leverage ratio further improved to 3.24x2,5 driven by excellent cash flow; Leverage target corridor under review.

- Fresenius Kabi delivering above the top-end of the structural growth band with organic revenue growth of 11%6; strong EBIT margin at 15.9%2.

- Growth Vectors at Kabi show continued strong performance, led by dynamic growth at Biopharma, which had yet again positive EBIT in Q3. Tyenne is in line with expectations, building on strong momentum.

- Fresenius Helios with excellent organic revenue growth of 8% driven by solid performance in Spain and supported by some favorable technical reclassifications in Germany; EBIT margin of 7.9%2 in line with expectations due to anticipated lower seasonal demand in Spain; last quarter of energy relief funding support.

- Dedicated Helios performance program underway to drive further operational excellence and compensate ending energy relief funding in Germany.

Michael Sen, CEO of Fresenius: Team Fresenius delivered an excellent third quarter in 2024 – all financial metrics improved versus the prior year. Revenues grew strongly, with margin expansion across the Group, and significantly improved cash flow generation. Both Kabi and Helios continue to deliver consistent and sustained financial performance. We are more focused and stronger, deploying our cash to reduce debt further, while growing earnings per share and driving shareholder returns. Quarter after quarter we are showing how our #FutureFresenius strategy is paying off. Our mission remains at the core of our activities: saving and improving human lives. Fresenius is: Committed to Life.” Sen continued, “Given the strength of our first nine months, we are upgrading our revenue and earnings guidance for the year.”

1 Organic growth rate adjusted for accounting effects related to Argentina hyperinflation.

2 Before special items

3 Growth rate adjusted for Argentina hyperinflation

4 Excluding Fresenius Medical Care

5 At average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures, including lease liabilities, including Fresenius Medical Care dividend

6 Organic growth rate adjusted for the accounting effects related to Argentina hyperinflation.

Conference call and Audio webcast

As part of the publication of the results for Q3/24, a conference call will be held on November 6, 2024 at 1:30 p.m. CET (7:30 a.m. EST). All investors are cordially invited to follow the conference call in a live audio webcast at www.fresenius.com/investors. Following the call, a replay will be available on

our website.

Note on the presentation of financial figures

An overview of the presentation of the financial figures are available on page 14 of this Investor News.

Structural productivity improvements: Target achieved ahead of plan

The Group-wide cost and efficiency measures are progressing faster than planned. The target for annual sustainable cost savings of ~€400 million at EBIT level has already been achieved with accumulative savings totaling €408 million until the end of Q3/24. Originally, it was expected to achieve the target by year-end 2025.

Fresenius will continue its efforts to increase structural productivity. So far, Kabi has delivered the majority of the savings. Going forward, it will be Fresenius Helios with its dedicated efficiency program focused on operations excellence including reduction of process and waiting times and digitalization of processes, resource optimization and synergies in particular in logistics and procurement. An update will be provided as part of the FY/24 results in February 2025.

Further efforts to enhance structural efficiency will, however, also be driven forward by Fresenius Kabi and the Corporate Center. Key elements include measures to reduce complexity, optimize supply chains and improve procurement processes.

Group sales and earnings development

Group revenue before special items increased by 7% (9% in constant currency) to €5,303 million (Q3/23: €4,967 million). Organic growth was 9%2, driven by Kabi and Helios's ongoing strong performance. Currency translation had a negative effect of 2% on revenue growth.

Group EBITDA before special items increased by 4% (5% in constant currency) to €814 million (Q3/23: €783 million).

Group EBIT before special items increased by 8% (9% in constant currency) to €552 million (Q3/23: €509 million), mainly driven by the strong organic revenue growth at Kabi and Helios and the continued progress of the groupwide cost savings program. The EBIT margin before special items was 10.4% (Q3/23: 10.2%). Reported Group EBIT was €492 million (Q3/23: €362 million).

Group net interest before special items increased to -€116 million (Q3/23: -€102 million) mainly due to financing activities in a higher interest rate environment.

Group tax rate before special items was 24.5% (Q3/23: 23.1%).

1 Before special items

2 Organic growth rate adjusted for accounting effects related to Argentina hyperinflation

3 Net income attributable to shareholders of Fresenius SE & Co. KGaA

Constant currency growth rates adjusted for Argentina hyperinflation. Financial figures and growth rates adjusted for the divestment of the fertility services group Eugin and the hospital stake in Peru.

Net income1 from deconsolidated Fresenius Medical Care operations before special items increased by 38% (42% in constant currency) to €76 million (Q3/231: €55 million).

Group net income1 before special items increased by 12% (13% in constant currency) to €388 million (Q3/231: €347 million). The increase was driven by operating strength. Reported Group net income1 increased to €326 million (Q3/231: -€406 million) mainly due to Fresenius Medical Care's positive net income contribution. The negative net income in the prior year period was due to the non-cash valuation effect of Fresenius Medical Care in accordance with IFRS 5.

Group net income1 before special items excluding Medical Care increased by 7% (7% in constant currency) to €312 million (Q3/231: €292 million).

Earnings per share1 before special items increased by 12% (13% in constant currency) to €0.69 (Q3/231: €0.62). Reported earnings per share1 were €0.58 (Q3/231: -€0.72).

1Net income attributable to shareholders of Fresenius SE & Co. KGaA

Constant currency growth rates adjusted for Argentina hyperinflation. Financial figures and growth rates adjusted for the divestment of the fertility services group Eugin and the hospital stake in Peru.

For a detailed overview of special items please see the reconciliation tables at

Financial Results | FSE (fresenius.com).

Group Cash flow development

Group operating cash flow (continuing operations) increased to €763 million (Q3/23: €603 million) mainly driven by the very good operational business development and improvements in working capital at Helios and Kabi. Group operating cash flow margin was 14.4% (Q3/23: 12.1%). Before acquisitions, dividends and lease liabilities, free cash flow (continuing operations) increased to €532 million (Q3/23: €346 million). After acquisitions, dividends and lease liabilities, free cash flow (continuing operations) improved to €623 million (Q3/23: €102 million).

Fresenius Kabi’s operating cash flow remained almost stable at €374 million (Q3/23: €380 million) with a margin of 17.7% (Q3/23: 18.8%).

Fresenius Helios’ operating cash flow increased to €454 million (Q3/23: €208 million) due to the strong focus on cash and working capital management in Germany and Spain. The operating cash flow margin improved to 14.7% (Q3/23: 7.3%).

The cash conversion rate (CCR), which is defined as the ratio of adjusted free cash flow1 to EBIT before special items was 1.2 in Q3/24 (LTM) (Q3/23: 0.9, LTM). This positive development is due to the strong cash flow focus across the Group.

The CCR is expected to be around 1 in FY/24.

1Cash flow before acquisitions and dividends; before interest, tax, and special items

Group leverage

Group debt decreased by -16% (-16% in constant currency) to €13,317 million

(Dec. 31, 2023: € 15,830 million) mainly related to the repayment of debt based on the excellent cash flow development and the around €400 million reduction of the leasing liabilities related to the Vamed exit. Group net debt decreased by -11%

(-11% in constant currency) to € 11,823 million (Dec. 31, 2023: € 13,268 million).

As of September 30, 2024, the net debt/EBITDA ratio was 3.24x1,2 (Dec. 31, 2023: 3.76x1,2) corresponding to a reduction of 52 bps compared to Dec. 31, 2023. This achievement is due to a combination of better EBITDA and Free cash flow. The legally required suspension of dividend payments and the Vamed exit further supported the positive development. Compared to Q3/23 (4.03x1,2) this is a 79 bps reduction.

Fresenius anticipates improving net debt/EBITDA ratio further3 towards the lower end of the self-imposed corridor of 3.0 to 3.5x by year-end 2024. This is expected to be driven by further reducing net debt and operational performance of the Operating Companies.

ROIC was 6.1% in Q1-3/24 (FY/23: 5.2%) mainly driven by the improvement in EBIT and the stringent capital allocation. With that, ROIC is within the ambition range of 6% to 8%. For 2024, Fresenius expects ROIC to be above 6.0% (previous: around 6.0%).

1 At average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures, including lease liabilities, including Fresenius Medical Care dividend

2 Before special items

3 At expected average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures; excluding further potential acquisitions/divestitures; before special items; including lease liabilities, including Fresenius Medical Care dividend

For a detailed overview of special items please see the reconciliation tables at

Financial Results | FSE (fresenius.com).

Operating Company Fresenius Kabi

Revenue increased by 5% (10% constant currency) to €2,114 million (Q3/23: €2,021 million). Organic growth was 11%1. This performance was driven by positive pricing effects, particularly in Argentina, and the excellent operating performance of the Growth Vectors.

Revenue of the Growth Vectors (MedTech, Nutrition and Biopharma) increased by 9% (16% in constant currency) to €1,158 million (Q3/23: €1,067 million). Organic growth was excellent at 16%1.

In Nutrition, organic growth of 11%1 benefited from positive pricing effects in Argentina and the good development in the US, driven by the ongoing roll-out of lipid emulsions. China continued to be impacted by a general economic weakness, price declines in connection with tenders, and indirect effects of the government’s countrywide anti-corruption campaign. Biopharma showed excellent organic growth of 66%1 driven by the overall good Biosimilars rollout in Europe and the U.S., with Tyenne standing out. Moreover, mAbxience also performed strongly, driven by bevacizumab and milestone payments. In MedTech, organic growth was of 7%1 driven by a broad-based positive development in the US, Europe and International, reflecting strong performances for infusion and nutrition systems.

1 Organic growth rate adjusted for accounting effects related to Argentina hyperinflation.

2 Before special items

Constant currency growth rates adjusted for Argentina hyperinflation.

For a detailed overview of special items please see the reconciliation tables at

Financial Results | FSE (fresenius.com).

Revenue in the Pharma (IV Drugs & Fluids) business increased by 2% (3% in constant currency; organic growth: 6% ) and amounted to €957 million (Q3/23: €941 million). Organic growth was mainly driven by a strong performance in Europe and International and solid growth in the U.S., driven by an improved backorder situation, compensating the softer development in China.

EBIT2 of Fresenius Kabi increased by 16% (16% in constant currency) to €335 million (Q3/23: €289 million) mainly due to the good revenue development, the positive EBIT result of the Biopharma business, and ongoing progress of the cost saving initiatives. EBIT margin2 was 15.9% (Q3/23: 14.3%) and thus at the upper end of 2024 outlook.

EBIT2 of the Growth Vectors increased by 62% (constant currency: 53%) to €168 million (Q3/23: €104 million) due to the positive EBIT of the Biopharma business and the good revenue development. EBIT margin2 was 14.5% (Q3/23: 9.8%). The Biopharma business is now expected to be EBIT break even also in the FY/24.

EBIT2 in the Pharma business decreased by -9% (constant currency: -8%) to €182 million (Q3/23: €200 million) primarily driven by additional costs due to the start of production at the main US plants in Wilson and Melrose Park. EBIT margin2 was 19.0% (Q3/23: 21.3%).

1 Organic growth rate adjusted for accounting effects related to Argentina hyperinflation.

2 Before special items

Constant currency growth rates adjusted for Argentina hyperinflation.

For a detailed overview of special items please see the reconciliation tables at

Financial Results | FSE (fresenius.com).

Operating Company Fresenius Helios

Revenue before special items increased by 8% (8% in constant currency) to €3,082 million (Q3/23: €2,863 million). Organic growth was 8%.

Revenue of Helios Germany increased by 8% (in constant currency: 8%) to €1,940 million (Q3/23: €1,800 million) due to pricing effects coupled with volume growth and supported by some favourable technical reclassifications. Organic growth was 8%.

Revenue of Helios Spain before special items increased by 8% (8% in constant currency) to €1,142 million (Q3/23: €1,062 million) driven by solid activity levels despite the anticipated lower seasonal demand, and favourable price effects. Organic growth was 8%. The clinics in Latin America also showed a good performance, additionally supported by currency exchange rate effects.

EBIT1 of Fresenius Helios increased by 7% (6% in constant currency) to €244 million (Q3/23: €229 million) with an EBIT margin1 of 7.9% (Q3/23: 8.0%).

EBIT1 of Helios Germany increased by 8% to €170 million (Q3/23: €157 million) with an EBIT margin1 of 8.8% (Q3/23: 8.7%). Q3/24 marked the last quarter in which energy relief funding was recognized in the income statement supporting profitability.

EBIT1 of Helios Spain decreased by -3% (0% in constant currency) to €73 million (Q3/23: €75 million) due to the expected seasonal softness and some phasing effects. The EBIT margin1 was 6.4% (Q3/23: 7.1%). On a more comparable nine-months basis, the EBIT margin1 was 11.2% (Q1-3/23: 11.2%).

1 Before special items

Financial figures and growth rates adjusted for the divestment of the fertility services group Eugin and the hospital stake in Peru.

For a detailed overview of special items please see the reconciliation tables at

Financial Results | FSE (fresenius.com).

Implications of the Fresenius Vamed exit

As of Q2 2024, Vamed is no longer a reporting segment of Fresenius. The company’s High-End-Services (HES) which offers services for Fresenius Helios and other hospitals, is included under Corporate / Other in the Group consolidated segment reporting.

In Q1-3/24, the divestment of the rehabilitation business and the Vamed operations in Austria led to non-cash special items of €406 million at Group net income level.

Special items related to the gradual scale back of the international project business amounted to €441 million at Group EBIT level in Q1-3/24, and to €357 million2 at Group net income level. A total amount of high triple-digit million euros of special items is expected, which is spread over the next few years and will be mostly cash-effective.

1 Before special items

2 According to ownership share

Financial figures and growth rates adjusted for the divestment of the fertility services group Eugin and the hospital stake in Peru.

For a detailed overview of special items please see the reconciliation tables at

Financial Results | FSE (fresenius.com).

Group and segment outlook for 20241

Fresenius upgrades its outlook for FY/24. Based on the excellent first nine months of 2024, Group organic revenue growth2,4,5 is now expected to grow between

6% to 8% (previous: between 4% to 7%) in 2024 and Group constant currency EBIT3,4 is anticipated to grow in a 8% to 11% range (previous: between 6% to 10%).

Fresenius Kabi expects organic revenue growth5 in a mid-to high-single-digit percentage range in 2024. The EBIT margin4 is expected to be in a range of 15% to 16% (structural margin band: 14% to 17%).

Fresenius Helios expects organic revenue4 to grow in mid-single digit percentage range in 2024. The EBIT margin4 is expected to be within 10% to 11% (structural margin band: 10% to 12%).

The Group outlook is given without Fresenius Vamed, i.e. exclusively for the Operating Companies Fresenius Kabi and Fresenius Helios.

1 For the prior-year basis please see table “Basis for Guidance for 2024”

2 2023 base: €20,307 million

3 2023 base: €2,266 million

4 Before special items

5 Organic growth rate adjusted for accounting effects related to Argentina hyperinflation.

Basis for Guidance for 2024

If no timeframe is specified, information refers to Q3/2024.

An overview of the results for Q3/2024 - before and after special items – is available on our website.

Consolidated results for Q3/24 as well as for Q3/23 include special items. These concern: divestment of the fertility services group Eugin and the hospital stake in Peru, Vamed exit, expenses associated with the Fresenius cost and efficiency program, transaction costs for mAbxience and Ivenix, costs in relation to the change of legal form of Fresenius Medical Care, legacy portfolio adjustments, IT transformation, transformation/exit Vamed, discontinued operations Vamed, special items at Fresenius Medical Care, and impact of PPA due to the application of the equity method to the Fresenius Medical Care investment. The special items shown within the reconciliation tables are reported in the Corporate/Other segment.

Note on the deconsolidation of Fresenius Medical Care

Following the deconsolidation of Fresenius Medical Care, Group financial figures are presented in accordance with IAS 28 (at equity method) since December 1, 2023. The proportionate share of 32% of Fresenius Medical Care is presented as a separate line in Fresenius Group’s P&L and balance sheet. Dividends received from Fresenius Medical Care are reported as a separate line as part of the cash flow statement. Moreover, IAS 28 requires a full purchase price allocation (PPA). The accounting for the PPA is treated as special item. For reasons of simplification and comparability, Fresenius presents net income with and without Fresenius Medical Care`s equity result.

Note on the portfolio optimization at Fresenius Helios

As part of the portfolio optimization, the sale of the fertility services group Eugin was completed on January 31, 2024. The divestment of the majority stake in the hospital Clínica Ricardo Palma hospital in Lima, Peru, was completed on April 23, 2024. Therefore, results of Fresenius Helios and accordingly of the Fresenius Group for Q3/24 and Q3/23 are adjusted.

Note on the growth rates Fresenius Kabi

Growth rates in constant currency of Fresenius Kabi are adjusted. Adjustments relate to the hyperinflation in Argentina. Accordingly, in constant currency growth rates of the Fresenius Group are also adjusted.

Note on the Vamed exit

Due to the application of IFRS 5, the prior year and prior quarter figures of the current year have been adjusted in the consolidated statement of income and the consolidated statement of cash flows. Vamed’s High-End-Services (HES) which offers services for Fresenius Helios and other hospitals, will be transferred to Fresenius and is included under Corporate / Other in the Group consolidated segment reporting. Details on the financial and accounting implications of the Vamed exit and the portfolio adjustments at Fresenius Helios are available on our website.

Information on the performance indicators are available on our website at www.fresenius.com/alternative-performance-measures.

This release contains forward-looking statements that are subject to various risks and uncertainties. Future results could differ materially from those described in these forward-looking statements due to certain factors, e.g. changes in business, economic and competitive conditions, regulatory reforms, results of clinical trials, foreign exchange rate fluctuations, uncertainties in litigation or investigative proceedings, the availability of financing and unforeseen impacts of international conflicts. Fresenius does not undertake any responsibility to update the forward-looking statements in this release.

- Strong organic growth in Group revenue of 8%1 to €5.4 billion2; excellent Group EBIT2 increase in constant currency of 15%3 to €660 million reflects strong operating performance and group-wide cost savings progressing ahead of plan.

- Strong bottom-line delivery: 15%2,3,4 EPS growth in constant currency.

- Major progress on deleveraging: Leverage ratio at 3.43x2,5 and therefore within the target corridor, in particular due to operating strength and the excellent cash flow.

- Structural productivity improvements ahead of plan.

- Strong operating cash flow development driven by working capital efficiencies and the increased focus on cash generation as well as excellent operating performance.

- Group outlook for fiscal 2024 confirmed based on excellent first half; Optimistic to get Group EBIT growth2,6 into upper half of 6 to 10% range.

- Fresenius Kabi clearly above the top-end of the structural growth band with very strong organic revenue growth of 11%1 ; excellent EBIT margin at 15.9%2.

- Growth Vectors at Kabi pacing performance: very strong organic growth of 19%1; EBIT margin of 14.7%2 within structural margin band.

- Biopharma accelerating momentum: very strong revenue growth and yet again positive EBIT in Q2 driven by the licensing business at mAbxience and ongoing ramp up of Tyenne.

- Fresenius Helios with strong organic revenue growth of 6%; EBIT margin of 11.1%2 driven by an excellent operating performance in Spain.

1 Organic growth rate adjusted for accounting effects related to Argentina hyperinflation.

2 Before special items

3 Growth rate adjusted for Argentina hyperinflation

4 Excluding Fresenius Medical Care

5 At average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures, including lease liabilities, including Fresenius Medical Care dividend

6 Constant currency

Conference call and Audio webcast

As part of the publication of the results for Q2/24, a conference call will be held on July 31, 2024 at 1:30 p.m. CEST (7:30 a.m. EDT). All investors are cordially invited to follow the conference call in a live audio webcast at www.fresenius.com/investors. Following the call, a replay will be available on our website.

Michael Sen, CEO of Fresenius: “Fresenius had an outstanding Q2 and first half in 2024. We delivered strong top-line growth, higher margins, and even more powerful bottom-line growth. Cash came in extremely strong, materially improving our financial profile. We are well ahead of our plans to deleverage and to take out costs. 2024 is an inflection year where we see how the work we’ve done continues to impact and improve the lives of patients and generate value for all stakeholders. Fresenius is 'Committed to Life' ".

Structural productivity improvements ahead of plan

The Group-wide cost and efficiency measures are progressing faster than planned. Including the first half of 2024, Fresenius has achieved structural cost savings totaling ~€336 million at EBIT level.

For the remainder of the year, Fresenius will continue its efforts to further increase its structural productivity. Some measures that were planned for 2025 will be brought forward to the current financial year. The company aims to achieve the target of annual sustainable cost savings of ~€400 million at EBIT level by year-end 2024. Originally, this was expected in 2025.

The structural cost savings continue to be driven by all business segments and the Corporate Center. Key elements include measures to reduce complexity, optimize supply chains and improve procurement processes.

Group sales and earnings development

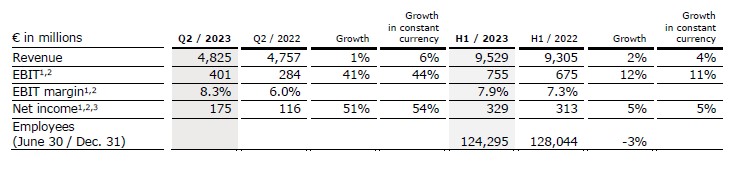

Group revenue before special items increased by 6% (8% in constant currency) to €5,414 million (Q2/23: €5,113 million). Organic growth was 8%2 driven by an ongoing strong performance of Kabi and Helios. Currency translation had a negative effect of 2% on revenue growth.

Group EBITDA before special items increased by 14% (14% in constant currency) to €938 million (Q2/23: €822 million).

Group EBIT before special items increased by 16% (15% in constant currency) to €660 million (Q2/23: €571 million) mainly driven by the good earnings development at Kabi and Helios and the continued progress of the groupwide cost savings program. The EBIT margin before special items was 12.2% (Q2/23: 11.2%). Reported Group EBIT was €265 million (Q2/23: €187 million).

Group net interest before special items was -€108 million (Q2/23: -€99 million) mainly due to financing activities in a higher interest rate environment.

Group tax rate before special items was 26.1% (Q2/23: 25.2%).

1 Before special items

2 Organic growth rate adjusted for accounting effects related to Argentina hyperinflation

3 Net income attributable to shareholders of Fresenius SE & Co. KGaA

Constant currency growth rates adjusted for Argentina hyperinflation. Financial figures and growth rates adjusted for the divestment of the fertility services group Eugin and the hospital stake in Peru.

Net income1 from deconsolidated Fresenius Medical Care operations before special items increased by 21% (16% in constant currency) to €69 million (Q2/231: €57 million).

Group net income1 before special items increased by 16% (15% in constant currency) to €457 million (Q2/231: €393 million). The increase was driven by the operating strength.

Group net income1 before special items excluding Medical Care increased by 15% (15% in constant currency) to €388 million (Q2/231: €336 million).

Reported Group net income1 decreased to -€373 million (Q2/231: €80 million) due to effects from special items related to the Vamed exit and the discontinued operations at Vamed.

Earnings per share1 before special items increased by 16% (15% in constant currency) to €0.81 (Q2/231: €0.69). Reported earnings per share1 were -€0.66 (Q2/231: €0.15) effects from special items related to the Vamed exit and the discontinued operations at Vamed.

1 Net income attributable to shareholders of Fresenius SE & Co. KGaA

Constant currency growth rates adjusted for Argentina hyperinflation. Financial figures and growth rates adjusted for the divestment of the fertility services group Eugin and the hospital stake in Peru.

For a detailed overview of special items please see the reconciliation tables at Financial Results.

Group Cash flow development

Group operating cash flow (continuing operations) almost quintupled to €709 million (Q2/23: €148 million). This excellent development is mainly related to working capital efficiencies and the increased focus on cash generation as well as excellent operating performance in Spain at Fresenius Helios. Group operating cash flow margin was 13.1% (Q2/23: 2.9%). Free cash flow before acquisitions, dividends and lease liabilities (continuing operations) increased to €674 million (Q2/23: €40 million). Free cash flow after acquisitions, dividends and lease liabilities (continuing operations) improved to €655 million (Q2/23: -€556 million).

Fresenius Kabi’s operating cash flow increased to €259 million (Q2/23: €180 million) with a margin of 12.3% (Q2/23: 9.0%) mainly driven by an improved working capital management, in particular related to inventories and receivables.

Fresenius Helios’ operating cash flow increased to €604 million (Q2/23: €61 million) in particular due to the strong operating performance in Spain and catch-up effects following a weaker first quarter. The strong focus on cash generation and improved management of working capital is also paying off. The operating cash flow margin was 18.7% (Q2/23: 2.0%).

The cash conversion rate (CCR), which is defined as the ratio of adjusted free cash flow1 to EBIT before special items was 1.1 in Q2/24 (LTM) (Q1/24: 0.9 LTM). This positive development is due to the increased cash flow focus across the Group.

1 Cash flow before acquisitions and dividends; before interest, tax, and special items

Group leverage

Group debt decreased by 14% (-15% in constant currency) to €13,536 million (Dec. 31, 2023: € 15,830 million) mainly related to the repayment of debt and the €400 million reduction of the leasing liabilities related to the Vamed exit. Group net debt decreased by 6% (-7% in constant currency) to € 12,428 million (Dec. 31, 2023: € 13,268 million).

As of June 30, 2024, the net debt/EBITDA ratio was 3.43x1,2 (Dec. 31, 2023: 3.76x1,2) corresponding to a reduction of 33 bps compared to FY/23. This achievement is due to a combination of the improved operational performance as well as better EBITDA and Free cash flow. The legally required suspension of dividend payments and the Vamed exit further supported the positive development. Compared to Q2/23 (4.19x1,2) this is a 76 bps reduction.

Fresenius expects the net debt/EBITDA3 ratio to be within the self-imposed corridor of 3.0 to 3.5x by the end of 2024. Further improvement in the second half of 2024 is expected. This is expected to be driven by further reducing net debt and by the operational performance at the Operating Companies.

ROIC improved to 6.0% in Q2/24 (FY/23: 5.2%) mainly due to the EBIT improvement and the stringed capital allocation. With that, ROIC reached the lower end of the self-defined target range of 6% to 8%.

For 2024, Fresenius now expects ROIC to be around 6.0% (previous: 5.4% to 6.0%), (2023: 5.2%).

1 At average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures, including lease liabilities, including Fresenius Medical Care dividend

2 Before special items

3 At expected average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures; excluding further potential acquisitions/divestitures; before special items; including lease liabilities, including Fresenius Medical Care dividend

For a detailed overview of special items please see the reconciliation tables at Financial Results.

Operating Company Fresenius Kabi

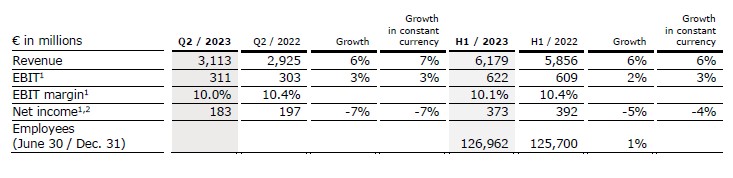

Revenue increased by 5% (10% constant currency) to €2,101 million (Q2/23: €2,001 million). The reported revenue growth is mainly driven by negative currency translation effects related to the hyperinflation in Argentina. Organic growth was 11%1. This strong performance was driven by the Growth Vectors and helped by pricing effects in Argentina.

Revenue of the Growth Vectors (MedTech, Nutrition and Biopharma) increased by 8% (19% in constant currency) to €1,149 million (Q2/23: €1,062 million). Organic growth was outstanding at 19%1. In Nutrition, organic growth of 14%1 benefited from the good development in the US, driven by the ongoing roll-out of lipid emulsions. Whereas China continued to be impacted by indirect effects of the government’s countrywide anti-corruption campaign and tender headwinds. Biopharma showed excellent organic growth of 102%1 driven by licensing agreements at mAbxience and the successful product launch of Tyenne in Europe. In MedTech, organic growth was of 9%1 driven by a broad-based positive development across most regions and many products groups.

Revenue in the Pharma (IV Drugs & Fluids) business was flat (0% in constant currency; organic growth: 2%1) and amounted to €951 million (Q2/23: €952 million). Organic growth was mainly driven by the positive development across many regions, particularly Europe.

EBIT2 of Fresenius Kabi increased by 17% (17% in constant currency) to €334 million (Q2/23: €285 million) mainly due to the good revenue development, the EBIT break-even result of the Biopharma business, and ongoing progress of the cost saving initiatives. EBIT margin2 was 15.9% (Q2/23: 14.2%) and thus at the upper end of 2024 outlook.

EBIT2 of the Growth Vectors increased by 93% (constant currency: 47%) to €169 million (Q2/23: €88 million) due to the EBIT break-even result of the Biopharma business and the good revenue development. EBIT2 margin was 14.7% (Q2/23: 8.3%).

EBIT2 in the Pharma business decreased by 10% (constant currency: -11%) to €185 million (Q2/23: €206 million) primarily driven by additional costs due to the start of production at the main US plants in Wilson and Melrose Park. EBIT2 margin was 19.5% (Q2/23: 21.6%).

1 Organic growth rate adjusted for accounting effects related to Argentina hyperinflation.

2 Before special items

Constant currency growth rates adjusted for Argentina hyperinflation.

For a detailed overview of special items please see the reconciliation tables at Financial Results.

Operating Company Fresenius Helios

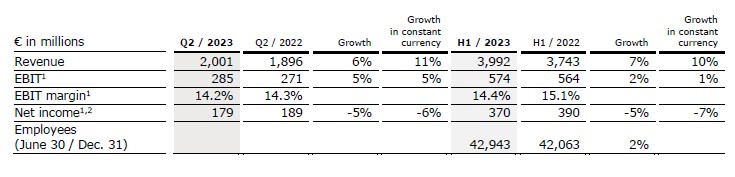

Revenue before special items increased by 7% (6% in constant currency) to €3,230 million (Q2/23: €3,020 million). Organic growth was 6%.

Revenue of Helios Germany increased by 3% (in constant currency: 3%) to €1,882 million (Q2/23: €1,823 million), mainly driven by favourable price effects and moderately increased activity levels. Organic growth was 3%.

Revenue of Helios Spain before special items increased by 13% (11% in constant currency) to €1,348 million (Q2/23: €1,198 million) driven by a positive calendar effect related to the Easter week and related higher activities, as well as positive price effects. Organic growth was 11%. The clinics in Latin America also showed a good performance.

EBIT1 of Fresenius Helios increased by 19% (18% in constant currency) to €357 million (Q2/23: €301 million) with an excellent EBIT margin1 of 11.1% (Q2/23: 10.0%) due to the strong operating performance in Spain.

EBIT1 of Helios Germany increased by 2% to €157 million (Q2/23: €154 million) with an EBIT margin1 of 8.3% (Q2/23: 8.4%) driven by the solid revenue development and helped by Government relief funding for higher energy costs.

EBIT1 of Helios Spain increased by 33% (32% in constant currency) to €201 million (Q2/23: €151 million) driven by the strong revenue growth based on the positive calendar effect related the Easter week as well as positive price effects. The EBIT margin1 reached 14.9% (Q2/23: 12.6%), clearly above the structural margin band ambition. On a more comparable half-year basis, the EBIT margin improved 30 bps to13.3% (H1/23: 13.0%).

Exit Fresenius Vamed

As of Q2 2024, Vamed is no longer a reporting segment of Fresenius. The company’s High-End-Services (HES) which offers services for Fresenius Helios and other hospitals, will be transferred to Fresenius and has already been included under Corporate / Other in the Group consolidated segment reporting.

The divestment of the rehabilitation business and the Vamed operations in Austria led to non-cash special items of €427 million at Group net income level.

Due to the exit from the project business, a total amount of high triple-digit million euros of special items are expected, which are spread over the next few years and mostly cash-effective. In H1/24, special items related to the gradual scale back of the international project business amounted to €425 million at Group EBIT level and to €343 million2 at Group net income level.

1 Before special items

2 According to 77% ownership share

Financial figures and growth rates adjusted for the divestment of the fertility services group Eugin and the hospital stake in Peru.

For a detailed overview of special items please see the reconciliation tables at Financial Results.

Group and segment outlook for 20241

Fresenius confirms its outlook for FY/24. Based on the excellent first half year, Fresenius is optimistic to get Group constant currency EBIT2,3 growth into the upper half of the 6% to 10% range. For 2024, Group organic revenue growth2,3 is expected to grow between 4% to 7%.

Fresenius Kabi expects organic revenue growth in a mid-to high-single-digit percentage range in 2024. The EBIT margin3 is expected to be in a range of 15% to 16% (structural margin band: 14% to 17%).

Fresenius Helios expects organic revenue3 to grow in mid-single digit percentage range in 2024. The EBIT margin3 is expected to be within 10% to 11% (structural margin band: 10% to 12%).

The Group outlook is given without Fresenius Vamed, i.e. exclusively for the Operating Companies Fresenius Kabi and Fresenius Helios.

1 For the prior-year basis please see table “Basis for Guidance for 2024”

2 2023 base: €2,266 million

3 Before special items

4 2023 base: €20,307 million

Basis for Guidance for 2024

1 Before special items

If no timeframe is specified, information refers to Q2/2024.

An overview of the results for Q2/2024 - before and after special items – is available on our website.

Consolidated results for Q2/24 as well as for Q2/23 include special items. These concern: divestment of the fertility services group Eugin and the hospital stake in Peru, Vamed exit, expenses associated with the Fresenius cost and efficiency program, transaction costs for mAbxience and Ivenix, costs in relation to the change of legal form of Fresenius Medical Care, legacy portfolio adjustments, IT transformation, transformation/exit Vamed, discontinued operations Vamed, special items at Fresenius Medical Care, and impact of PPA due to the application of the equity method to the Fresenius Medical Care investment. The special items shown within the reconciliation tables are reported in the Corporate/Other segment.

Note on the deconsolidation of Fresenius Medical Care

Following the deconsolidation of Fresenius Medical Care, Group financial figures are presented in accordance with IAS 28 (at equity method) since December 1, 2023. The proportionate share of 32% of Fresenius Medical Care is presented as a separate line in Fresenius Group’s P&L and balance sheet. Dividends received from Fresenius Medical Care are reported as a separate line as part of the cash flow statement. Moreover, IAS 28 requires a full purchase price allocation (PPA). The accounting for the PPA is treated as special item. For reasons of simplification and comparability, Fresenius presents net income with and without Fresenius Medical Care`s equity result.

Note on the portfolio optimization at Fresenius Helios

As part of the portfolio optimization, the sale of the fertility services group Eugin was completed on January 31, 2024. The divestment of the majority stake in the hospital Clínica Ricardo Palma hospital in Lima, Peru, was completed on April 23, 2024. Therefore, results of Fresenius Helios and accordingly of the Fresenius Group for Q2/24 and Q2/23 are adjusted.

Note on the growth rates Fresenius Kabi

Growth rates in constant currency of Fresenius Kabi are adjusted. Adjustments relate to the hyperinflation in Argentina. Accordingly, in constant currency growth rates of the Fresenius Group are also adjusted.

Note on the Vamed exit

Due to the application of IFRS 5, the prior year and prior quarter figures of the current year have been adjusted in the consolidated statement of income and the consolidated statement of cash flows. Vamed’s High-End-Services (HES) which offers services for Fresenius Helios and other hospitals, will be transferred to Fresenius and is included under Corporate / Other in the Group consolidated segment reporting. Details on the financial and accounting implications of the Vamed exit and the portfolio adjustments at Fresenius Helios are available on our website.

Information on the performance indicators are available on our website at

https://www.fresenius.com/alternative-performance-measures.

This release contains forward-looking statements that are subject to various risks and uncertainties. Future results could differ materially from those described in these forward-looking statements due to certain factors, e.g. changes in business, economic and competitive conditions, regulatory reforms, results of clinical trials, foreign exchange rate fluctuations, uncertainties in litigation or investigative proceedings, the availability of financing and unforeseen impacts of international conflicts. Fresenius does not undertake any responsibility to update the forward-looking statements in this release.

Fresenius published its first Sustainability Highlights Report today. In the online report, the company presents its sustainability strategy, ambitions and highlights. In addition, the company reports on Scope 3 emissions for the first time, thereby creating full transparency across the entire value chain.

- Improving Fresenius Helios outlook for FY/24 – Expecting mid-single-digit revenue growth and an EBIT margin of 10% to 11% in FY/24

- Raising ambition level for Fresenius Helios within Fresenius Financial Framework – Targeting organic revenue growth of 4% to 6% p.a. as well as structural EBIT margin band of 10% to 12%

- System-critical and stable businesses – Helios Germany’s and Quirónsalud’s patient-centric, reliable and market-leading provider network driving steady capital-efficient organic growth and consistent cash-flow generation

- Digital and data strategy – Bringing new tools and technologies, such as AI, to clinical practice and tapping opportunities to leverage proprietary data to boost treatment outcomes

- Key value drivers – Clustering and specialization, outpatient integration, and emergency care provision in Germany; technology-focused improvements, enhanced physician value proposition, and selective network expansion in Spain

At its Capital Markets Day in London, global healthcare company Fresenius today presented a strategy update for its Care Provision Platform and improved the outlook for its Operating Company Fresenius Helios. For FY/24, Fresenius Helios now expects organic revenue to grow in a mid-single digit percentage range (previous: low-to-mid-single-digit percentage range) and targets an EBIT margin of 10 to 11% (previous: within structural margin band of 9% to 11%). Furthermore, Fresenius raised its ambition level for Fresenius Helios within the Fresenius Financial Framework, and now targets an annual organic revenue growth of 4% to 6% (previous: 3% to 5%) as well as a structural margin band of 10% to 12% (previous: 9% to 11%). The ambition is to grow EBIT stronger than revenue, hence, underlining accelerated profitable growth. Fresenius Helios further sharpens its focus on optimizing net working capital to improve its sustainable cash flow generation. The expected acceleration of organic revenue growth, targeted productivity improvements, enhanced profitability and rigorous capital allocation measures are contributing to Fresenius Group’s ambition to improve its Return on Invested Capital (ROIC) and its deleveraging efforts.

The improved expectations follow a strong start into 2024 and are based on the key elements and drivers of Fresenius Helios’ growth strategy, which Fresenius outlined to analysts and investors today. The main growth drivers at Helios in Germany are an extended medical cluster & specialization strategy, further improved outpatient integration and a boost of the emergency care provision. At Quirónsalud, the main growth drivers are technology-focused improvements, various physician support initiatives, as well as a selective network expansion. Fresenius Helios is Europe's leading private healthcare provider. It operates around 140 hospitals and more than 400 outpatient facilities under its brands Helios in Germany and Quirónsalud in Spain and Colombia.

Fresenius CEO Michael Sen said: “As a leading therapy-focused company, we are shaping the future of healthcare, which will be digital, data-driven, personalized and human. And this is where our strength lies. We are close to the patients. We are Committed to Life. That is the promise we have made with #FutureFresenius. And we are a simpler and stronger company today. Our sharpened focus on our Operating Companies is paying off. The strong and reliable growth momentum of our Care Provision Platform gives us confidence which is why we are improving the outlook for Fresenius Helios for the full year.”

Hospital markets growing

Hospital markets in Germany and Spain are growing steadily and reliably. In Germany, the total hospital market in 2023 was around €120 billion. It is expected to grow by 3% to 4% per year until 2027, driven by supportive demographic trends including an aging population and inflation-related base rate adjustments. Furthermore, Helios Germany sees itself well positioned to benefit from the planned hospital reform, which fosters hospital network concentration, specialization and a stronger integration of inpatient and outpatient care.

In Spain, where there are distinct public and private healthcare systems, the private provider segment accounted for 20% (€21 billion) of total provider expenditures in 2023 and is expected to grow at an average rate of 4% to 5% annually until 2027. This growth is – like in Germany – also driven by demographic factors, and price adjustments, but also by a continued uptake of private health insurances due to public system pressure, resulting in a growing demand for private provider offerings.

Robert Möller, member of the Fresenius Management Board and CEO of Fresenius Helios, said: “Providing world-class care and high-quality medical outcomes is key to our success. We lead in two steadily growing and highly attractive markets, representing roughly 30% of the EU's total population. It makes us number one in European healthcare provision, and it makes us critical for the systems we serve. With our proven focus on superior medical outcome quality, highly efficient care provision and strong digital and data capabilities, we are well positioned in both countries to drive steady, value-accretive growth.”

Growth strategies for Germany and Spain

In Germany, Helios will further drive its strategy of grouping its hospitals into highly specialized clusters, whereby two to five hospitals in geographic proximity form one multi-site hospital system. Experience shows that these clusters deliver higher medical quality, efficiency and growth by consolidating and better aligning medical and administrative activities as well as promoting specialization among the locations. The cluster and specialization strategy therefore is also well aligned with current and expected future regulatory changes in Germany. This also applies to the stronger integration of inpatient and outpatient care, which Helios expects to support with its own network of around 230 outpatient centers and strong relationships with external partners. These allow for seamless patient journeys and a closer collaboration between physicians resulting in improved patient experience and medical outcome quality.

Quirónsalud in Spain focuses on its core hospital operations and continued value creation based on its leadership position and solid market fundamentals. The Spanish hospital market is highly attractive with a growing private healthcare segment, providing tailwinds to Quirónsalud’s steady and resilient growth going forward. Focus of Quirónsalud will be on further improving clinical pathways, leveraging digital capabilities to optimize processes and performance as well as to boost patient care quality. Already today, Quirónsalud has an outstanding positioning in digitalization in Spain with more than 6 million registered patient portal users and large parts of the patient journey being already fully digitalized. In addition, Quirónsalud will drive value from strengthening its value proposition to attract and retain best-in-market talents as well as in engaging selective network expansion.

Digitalization as enabler to boost medical outcome quality

Given their commitment to highest medical quality, Helios Germany and Quirónsalud highly focus on outcome quality and its continuous further improvement by measurement against internal and external benchmarks. Helios in Germany, for example, delivers better quality performance versus the market average in 89% of its cases and has a patient satisfaction rate of 96%. Meanwhile Quirónsalud is the first private group worldwide to earn the JCI accreditation for healthcare quality at the corporate level and has a 90% patient satisfaction rate. Both Helios Germany and Quirónsalud are currently rolling out a structured benchmarking program to intensify cross company comparison and best practice sharing from best performing hospitals, setting the benchmark for all hospitals in the group.

Leveraging medical data, analytics and AI will further promote improved medical outcomes as well as personalized care and better patient experience. Fresenius Helios aims to systematically utilize medical and clinical data to improve treatment quality and outcomes, as well as unlock experience and efficiency gains for its patients, its people, and its performance at the same time. The clear aim is to have all relevant clinical decision-making supported by digital assistance in the mid-term.

ESG: Zero CO2 emissions by 2040

Fresenius Helios reiterates its ambitious ESG targets across its business activities with clearly defined tracking and connection to management remuneration. Its ESG strategy holistically aims to serve patients, people and the planet and is reflected in respective KPIs. Initiatives focused on patients include the Inpatient Quality Indicator and ISO certifications of Helios hospitals, for instance. The efforts for its people are, for example, captured with the People Engagement Index, reflecting initiatives like employee training. With regard to its planet commitment, Fresenius Helios’ key ambition is to reduce CO2 emissions by 50% by 2030 and to zero by 2040.

Webcast

Presentations will be held on June 5, 2024, starting at 11:30 a.m. CEDT. You are cordially invited to follow the Capital Markets Day in a live webcast at https://www.fresenius.com/capital-markets-day. After the event, a replay will be available on our website.

This release contains forward-looking statements that are subject to various risks and uncertainties. Future results could differ materially from those described in these forward-looking statements due to certain factors, e.g. changes in business, economic and competitive conditions, regulatory reforms, results of clinical trials, foreign exchange rate fluctuations, uncertainties in litigation or investigative proceedings, the availability of financing and unforeseen impacts of international conflicts. Fresenius does not undertake any responsibility to update the forward-looking statements in this release.

- Excellent start to 2024: Group outlook raised for FY/24 due to the excellent first quarter and a better than originally expected operating performance for the remainder of the financial year 2024: Group organic revenue growth 4 to 7%, EBIT growth in constant currency 6 to 10%.

- Strategic portfolio measures concluded: Structured exit from Investment Company Vamed initiated.

- Strong organic growth in Group revenue of 6%1 to € 5.7 billion in Q1/24; Group EBIT increase in constant currency by 15% to € 633 million reflects the excellent performance of Operating Companies and the group-wide cost savings progressing ahead of plan.

- EPS increases: 11% in constant currency.

- Strong operating cash flow development at Fresenius Kabi driven by working capital efficiencies; Fresenius Helios expects catch-up of outstanding receivables in Germany in the course of the year.

- Fresenius Kabi shows excellent organic revenue growth of 9%1 and an improved EBIT margin at 15.1% in particular driven by the positive development of the Biopharma business.

- Biopharma business picking up: EBIT break-even in Q1/24 driven by licensing business at mAbxience; Tyenne with good progress.

- Fresenius Helios with solid organic revenue growth of 5%2 and EBIT margin of 11.1%; supported by phasing of energy related government relief funding in Germany and strong operating performance.

1 Organic growth rate adjusted for the accounting effects related to Argentina hyperinflation.

2 Organic growth rate adjusted for the divestment of the fertility services group Eugin and the hospital stake in Peru.

If no timeframe is specified, information refers to Q1/2024.

An overview of the results for Q1/2024 - before and after special items – is available on our website.

Following the deconsolidation of Fresenius Medical Care, Group financial figures are presented in accordance with IAS 28 (at equity method) since December 1, 2023. The proportionate share of 32% of Fresenius Medical Care is presented as a separate line in Fresenius Group’s P&L and balance sheet. Dividends received from Fresenius Medical Care will also be reported as a separate line as part of the cash flow statement. Moreover, IAS 28 requires a full purchase price allocation (PPA). The accounting for the PPA is treated as special item. For reasons of simplification and comparability, Fresenius presents net income with and without Fresenius Medical Care`s equity result.

Information on the performance indicators are available on our website at https://www.fresenius.com/alternative-performance-measures.

Consolidated results for Q1/24 as well as for Q1/24 include special items. These concern: revaluations of biosimilars contingent purchase price liabilities, expenses associated with the Fresenius cost and efficiency program, transaction costs for mAbxience and Ivenix, costs in relation to the change of legal form of Fresenius Medical Care, the transformation of Fresenius Vamed, legacy portfolio adjustments, special items at Fresenius Medical Care, and impact of PPA equity method Fresenius Medical Care. The special items shown within the reconciliation tables are reported in the Corporate/Other segment.

Growth rates of Fresenius Kabi and Fresenius Helios are adjusted. Adjustsments relate to the divestment of the fertility services group Eugin and the hospital stake in Peru at Fresenius Helios and Helios Spain as well as to hyperinflation in Argentina at Fresenius Kabi. Accordingly, growth rates of the Fresenius Group are also adjusted.

Conference call and Audio webcast

As part of the publication of the results for Q1/24, a conference call will be held on May 8, 2024 at 1:30 p.m. CET (7:30 a.m. EST). All investors are cordially invited to follow the conference call in a live audio webcast at https://www.fresenius.com/investors. Following the call, a replay will be available on our website.

Michael Sen, CEO of Fresenius: “Fresenius has made an excellent start into the year and our focus on Fresenius Kabi and Fresenius Helios is paying off. We are confident to maintain our growth momentum and raise our outlook for the full year. With the exit from Vamed, our strategic portfolio restructuring is completed as planned. Fresenius is already a simpler, stronger, and more innovative company due to the consistent implementation of #FutureFresenius. We now have even more opportunities to offer world-class therapies and improve people’s health.”

#FutureFresenius: Exit from Investment Company Vamed concludes strategic portfolio measures

The exit from the Investment Company Vamed completes the strategic portfolio restructuring as part of #FutureFresenius. The exit is carried out in three parts: 1) The already announced sale of 67 % of Vamed’s rehabilitation business to the private equity company PAI. Closing of this transaction is expected in the second half of 2024 2) Vamed’s operations in Austria to be sold to an Austrian consortium of the construction companies Porr and Strabag for a total purchase price of €90 million. 3) The Health Tech Engineering (HTE) segment, which is responsible for the international project business and accounts for around 15% of Vamed's revenue, will gradually be scaled back in an orderly manner. The process should largely be completed by 2026. Until then, the business will be reported as a special item outside Fresenius' core business. Current project contracts will be fulfilled.

Vamed’s High-End-Services (HES) which offers services for Fresenius Helios and other hospitals, will be transferred to Fresenius. HES is a stable business with good growth prospects and accounts for around 30% of Vamed's revenues. The profitability of HES is in the mid-single-digit percentage range.

The divestments of the rehabilitation business and the operations in Austria lead to non-cash special items of around €0.6 billion.

Due to the exit from the project business, a high triple-digit-million euro amount of special items are expected, which are spread over the next few years and mostly cash-effective.

As of Q2 2024, Vamed will no longer be a reporting segment of Fresenius. In addition to reducing complexity, this step is expected to improve the Group's profitability by more than 50 basis points. It will also reduce net debt and increase the Group's return on invested capital (ROIC). Last but not least, the transparency and quality of earnings will be significantly enhanced.

After exiting from Vamed, Fresenius will consist of the two Operating Companies Fresenius Kabi and Fresenius Helios (each with 100% ownership share) and the Investment Company Fresenius Medical Care (32% ownership share).

Cost savings program fully on track

The groupwide cost savings program progressed is fully on track. Under the program, Fresenius realized ~€25 million incremental structural cost savings at EBIT level in Q1/24. In the same period, one-time costs of ~€15 million incurred to achieve these savings.

Fresenius expects to achieve annual sustainable cost savings of ~€400 million at EBIT level by 2025. So far, Fresenius reached ~€305 million of cumulative structural cost savings. To reach this target, one-time costs between ~€80 and €100 million are anticipated between 2024 and 2025.

For 2024, total cost savings of ~€330 to €350 million are expected. This corresponds to incremental cost savings of ~€50 to €70 million in 2024 compared to 2023.

The programs continue to target all business segments and the Corporate Center. Key elements include measures to optimize sales and administrative costs, fostering digitalization as well as improve procurement processes.

Group sales and earnings development

Group revenue increased by 4% (6% in constant currency) to €5,704 million (Q1/23: €5,546 million). Organic growth was 6%1 driven by an ongoing strong performance of our Operating Companies. Currency translation had a negative effect of 2% on revenue growth.

In Q1/24, revenue of the Operating Companies increased by 5% (7% in constant currency) to €5,216 million (Q1/23: €5,039 million).

Group EBITDA before special items increased by 13% (13% in constant currency) to €924 million (Q1/232: €828 million).

Group EBIT before special items increased by 15% (15% in constant currency) to €633 million (Q1/232: €554 million) mainly driven by the good earnings development at the Operating Companies and the continued progress of the groupwide cost savings program. The EBIT margin before special items was 11.1% (Q1/231: 10.0%). Reported Group EBIT was €559 million (Q1/23: €526 million).

The Operating Companies showed an 9% increase of EBIT before special items (9% in constant currency) to €631 million (Q1/232: €581 million) with an EBIT margin of 12.1% (Q1/232: 11.5%).

1 Organic growth rate adjusted for the divestment of the fertility services group Eugin, the hospital stake in Peru, and accounting effects related to Argentina hyperinflation.

2 Before special items

3 Net income attributable to shareholders of Fresenius SE & Co. KGaA

Group net interest before special items increased to -€115 million (Q1/231: -€87 million) mainly due to financing activities in a higher interest rate environment.

Group tax rate before special items was 24.5% (Q1/231: 24.4%).

Net income1 from deconsolidated Fresenius Medical Care operations before special items increased by 25% (33% in constant currency) to €60 million (Q1/232: €48 million).

Group net income2 before special items increased by 10% (11% in constant currency) to €429 million (Q1/232: €389 million). The increase was driven by the operating strength which outpaces higher interest.

Group net income1 before special items excluding Medical Care increased by 8% (8% in constant currency) to €369 million (Q1/232: €341 million).

Reported Group net income2 decreased to €278 million (Q1/232: €346 million).

Negative effects from the Purchase Price Allocation (PPA) and other negative special items at Fresenius Medical Care as well as the Vamed transformation had a negative impact on the Group net income income1.

Earnings per share2 before special items increased by 10% (11% in constant currency) to €0.76 (Q1/232: €0.69). Reported earnings per share2 were €0.49 (Q1/23: €0.61).

1 Before special items

2 Net income attributable to shareholders of Fresenius SE & Co. KGaA

For a detailed overview of special items please see the reconciliation tables at Financial Results.

Group Cash flow development

Group operating cash flow was €2 million (Q1/23: €32 million). The first quarter is usually the softest in the course of the year. In Q1/24 the soft operating cash flow was mainly driven by temporarily higher working capital, in particular due to nursing budget related receivables built ups at Helios Germany. Group operating cash flow margin was 0.0% (Q1/23: 0.6%). Free cash flow before acquisitions, dividends and lease liabilities decreased to -€194 million (Q1/23: -€180 million). Free cash flow after acquisitions, dividends and lease liabilities improved to -€103 million (Q1/23: -€258 million).

Fresenius Kabi’s operating cash flow increased to €157 million (Q1/23: €21 million) with a margin of 7.7% (Q1/23: 1.1%) mainly driven by an improved working capital management.

Fresenius Helios’ operating cash flow decreased to -€117 million (Q1/23: €108 million) and was impacted by higher working capital in particular driven by temporary nursing budget related receivables built-ups at Helios Germany. The operating cash flow margin was -3.7% (Q1/23: 3.5%).

Fresenius Vamed’s operating cash flow improved to -€10 million (Q1/23: -€68 million) with a margin of -1.8% (Q1/23: -11.7%).

The cash conversion rate (CCR), which is defined as the ratio of adjusted free cash flow1 to EBIT before special items was 1.0 in Q1/24 (LTM) (Q1/23: 0.9 LTM). This positive development is due to the increased cash flow focus across the Group.

1 Cash flow before acquisitions and dividends; before interest, tax, and special items

Group leverage

Group debt decreased by 8% (8% in constant currency) to €14,504 million (Dec. 31, 2023: € 15,830 million) mainly related to the repayment of debt. Group net debt increased by 2% (2% in constant currency) to € 13,485 million (Dec. 31, 2023: € 13,268 million) which is mainly related to the cash flow development at Fresenius Helios, particularly driven by temporary receivables built ups related to the nursing budget at Helios in Germany.

As of March 31, 2024, the net debt/EBITDA ratio was 3.75x1,2 (Dec. 31, 2023: 3.76x1,2), a further reduction compared to Q4/23 and mainly driven by the good EBITDA development. Compared to Q1/23 (3.96x1,2) this is a 21 bps reduction.

Fresenius expects the net debt/EBITDA3 ratio to be within the self-imposed corridor of 3.0 to 3.5x by the end of 2024. This is expected to be driven by reducing net debt and by the operational performance at the Operating Companies.

ROIC increased to 5.5% in Q1/24 (Q1/23: 5.2%) mainly due to the EBIT improvement. The Operating Companies improved ROIC to 5.8% (Q1/23: 5.5%).

1 At average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures, including lease liabilities, including Fresenius Medical Care dividend

2 Before special items

3 At expected average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures; excluding further potential acquisitions/divestitures; before special items; including lease liabilities, including Fresenius Medical Care dividend

For a detailed overview of special items please see the reconciliation tables at Financial Results.

Operating Company Fresenius Kabi

Revenue increased by 9% in constant currency (3% reported) to €2,051 million (Q1/23: €1,991 million). The reported revenue growth is mainly driven by negative currency translation effects related to the US dollar and the hyperinflation in Argentina. Organic growth was 9%1. This strong performance was driven in particular by the Biopharma business as well as by Nutrition.

Revenue of the Growth Vectors (MedTech, Nutrition and Biopharma) increased by 4% (14% in constant currency) to €1,089 million (Q1/23: €1,051 million). Organic growth was outstanding at 13%. In Nutrition, organic growth of 8% benefited from the good development in the US and was driven by many other international markets. Whereas China continued to be impacted by indirect effects of the government’s countrywide anti-corruption campaign and direct effects of the soft economy. Biopharma showed excellent organic growth of 117% driven by successful product launches in Europe and the US, as well as licensing agreements. MedTech showed organic growth of 1% given the high prior-year level.

1 Organic growth rate adjusted for accounting effects related to Argentina hyperinflation.

2 Before special items

Growth rates adjusted for Argentina hyperinflation.

Revenue in the Pharma (IV Drugs & Fluids) business increased by 2% (4% in constant currency; organic growth: 5%) and amounted to €962 million (Q1/23: €940 million). The solid organic growth was mainly driven by the positive development across many regions including the US.

EBIT1 of Fresenius Kabi increased by 7% (8% in constant currency) to €310 million (Q1/23: €289 million) mainly due to the good revenue development, the EBIT break-even result of the Biopharma business, and ongoing progress of the cost saving initiatives. EBIT margin1 was 15.1% (Q1/23: 14.5%) and thus within the structural EBIT margin band.

EBIT1 of the Growth Vectors increased by 29% (constant currency: 17%) to €124 million (Q1/23: €96 million) due to the EBIT break-even result of the Biopharma business and the good revenue development. EBIT1 margin was 11.4% (Q1/23: 9.2%).

EBIT1 in the Pharma business increased 4% (constant currency: 6%) to €206 million (Q1/23: €197 million) due to the very well-progressing cost saving initiatives and the good revenue development. EBIT1 margin was 21.4% (Q1/23: 21.0%).

1 Before special items

Growth rates adjusted for Argentina hyperinflation.

For a detailed overview of special items please see the reconciliation tables at Financial Results.

Operating Company Fresenius Helios

Revenue increased by 6% (5% in constant currency) to €3,184 million (Q1/23: €3,066 million). Organic growth was 5%.

Revenue of Helios Germany increased by 4% (in constant currency: 4%) to €1,903 million (Q1/23: €1,828 million), mainly driven by solid admissions numbers and favourable price effects. Organic growth was 4%.

Revenue of Helios Spain increased by 10% (8% in constant currency) to €1,281 million (Q1/23: €1,170 million) driven by ongoing strong activity levels and positive price effects. Organic growth was 7%1. The clinics in Latin America also showed a good performance.

EBIT2 of Fresenius Helios increased by 14% (14% in constant currency) to €353 million (Q1/23: €311 million) with an EBIT margin2 of 11.1% (Q1/23: 10.1%).

EBIT of Helios Germany increased by 32% to €205 million (Q1/23: €155 million) with an EBIT margin of 10.8% (Q1/23: 8.5%) in particular driven by the phasing of the Government relief funding for higher energy costs as well as the good revenue development and the progressing cost savings program.

1 Before special items

Growth rates adjusted for the divestment of the fertility services group Eugin and the hospital stake in Peru

For a detailed overview of special items please see the reconciliation tables at Financial Results.

EBIT1 of Helios Spain decreased by 6% (7% in constant currency) to €149 million (Q1/23: €157 million). EBIT1 was impacted by the phasing due to the calendar variation related to the Easter week and related lower activities and mix effects as well as a high prior-year level. Despite the Easter effect, the EBIT margin1 was 11.6% (Q1/23: 13.4%).

As part of the portfolio optimization, the sale of the fertility services group Eugin was completed on January 31, 2024. The divestment of the majority stake in the hospital Clínica Ricardo Palma hospital in Lima, Peru, was completed on April 23, 2024. The sale marks Fresenius’ exit from the Peruvian hospital market.

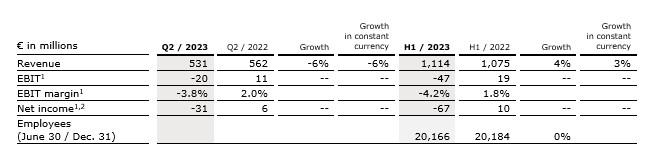

Fresenius Vamed

Further progress was made in Q1/24 with the far-reaching restructuring program to increase Fresenius Vamed’s profitability which was initiated in 2023.

Revenue from continued business was €514 million in Q1/24. Organic growth of the continued business increased 1% driven by the positive development of the Services business offsetting the negative effects of the Project business. Total revenue of Fresenius Vamed was €561 million (Q1/23: €583 million) and declined by 4% (-4% in constant currency).

EBIT1 was at €2 million in Q1/24 (Q1/231: -€27 million), thus showing a significant year-over-year improvement and making it the third consecutive quarter of positive EBIT. The EBIT margin1 in Q1/24 was 0.4% (Q1/231: -4.6%).

The ongoing transformation resulted in negative special items of €47 million in Q1/24 mainly related to cessation of activities, asset re-evaluations and restructuring costs resulting in write-downs and provisions. The negative special items were predominantly booked as non-cash items.

1 Before special items

Growth rates adjusted for the divestment of the fertility services group Eugin and the hospital stake in Peru

Group and segment outlook for 20241

Fresenius raises its outlook for FY/24 based on the excellent first quarter and improved prospects for the ramainder of the year.

For 2024, Group organic revenue growth2 is now expected to grow between 4% to 7% (previous: 3% to 6%). Group constant currency EBIT3,4 is expected to grow in the rage of 6% to 10% (previous: 4% to 8%).

Fresenius Kabi now expects organic revenue growth in a mid-to high-single-digit percentage range in 2024 (previous: mid-single-digit percentage range). The EBIT margin4 is now expected to be in a range of 15% to 16% (previously: around 15%) (structural margin band: 14% to 17%).

Fresenius Helios expects organic revenue to grow in a low to mid-single digit percentage range in 2024. The EBIT margin4 is expected to be within the structural margin band of 9% to 11%.

The adjustment of the Group outlook also reflects the fact that the forecast is now given without Fresenius Vamed, i.e. exclusively for the Operating Companies Fresenius Kabi and Fresenius Helios. Following the announcement of the planned divestment of Fresenius Vamed's rehabilitation business, Fresenius has initiated its structured exit from its Investment Company Fresenius Vamed.

1 For the prior-year basis please see table “Basis for Guidance for 2024”

2 2023 base: €20,307 million

3 2023 base: €2,266 million

4 Before special items

Basis for Guidance for 2024

This release contains forward-looking statements that are subject to various risks and uncertainties. Future results could differ materially from those described in these forward-looking statements due to certain factors, e.g. changes in business, economic and competitive conditions, regulatory reforms, results of clinical trials, foreign exchange rate fluctuations, uncertainties in litigation or investigative proceedings, the availability of financing and unforeseen impacts of international conflicts. Fresenius does not undertake any responsibility to update the forward-looking statements in this release.

- Fresenius achieves the raised outlook for FY/23. Strong fourth quarter with continued good development of the Operating Companies Fresenius Kabi and Fresenius Helios and progress in the turnaround of the Investment Company Fresenius Vamed.

- Group 2024 outlook: Organic revenue growth expected between 3% and 6%; EBIT expected to grow between 4% and 8%.

- Improvement leverage ratio: expected to be within the target corridor of 3.0x to 3.5x by the end of 2024.

- Revenue of €22.3 billion in FY/23: Strong organic Group revenue growth of 6%; Group EBIT increased 2% in constant currency to €2.3 billion; excellent Group operating cashflow totaled €2.1 billion.

- Group cost savings target significantly exceeded by ~40% in 2023 – FY/25 structural productivity savings target raised to ~€400 million at EBIT level (before: ~€350 million).

- Group revenue increased organically by 5% in Q4; Group EBIT increased by 8% in constant currency.

- Fresenius Kabi with excellent organic revenue growth of 7% in Q4 at top-end of structural growth band and EBIT margin of 14.1% within structural band.

- Fresenius Helios with strong organic revenue growth of 5% in Q4 at top-end of structural growth band and excellent EBIT margin of 11.6 % well above structural margin band.

- Fresenius Vamed’s transformation progressing well; ongoing operational improvement with positive EBIT in second consecutive quarter.

- Ongoing divestments: Sale of fertility services group Eugin successfully completed in January 2024.

If no timeframe is specified, information refers to Q4/2023.

An overview of the results for Q4/2023 and the 2023 financial year - before and after special items – is available on our website.

Following the deconsolidation of Fresenius Medical Care, Group financial figures are presented in accordance with IAS 28 (at equity method) since December 1, 2023. Prior-year figures have been adjusted due to the application of IFRS 5 to the deconsolidated operations of Fresenius Medical Care.

Information on the performance indicators are available on our website at https://www.fresenius.com/alternative-performance-measures.

Consolidated results for FY/23 as well as for FY/22 in-clude special items. These concern: revaluations of biosimilars contingent purchase price liabilities, expenses associated with the Fresenius cost and efficiency program, impacts related to the war in Ukraine, transaction costs for mAbxience and Ivenix, hyperinflation in Türkiye, retroactive duties, costs in relation to the change of legal form of Fresenius Medical Care, the transformation of Fresenius Vamed, legacy portfolio adjustment, effects from the valua-tion of the investment in Fresenius Medical Care in ac-cordance with IFRS 5, and expenses PPA equity method Fresenius Medical Care. The special items shown within the reconciliation tables are reported in the Corpo-rate/Other segment.

Conference call and Audio webcast

As part of the publication of the results for FY/23, a conference call will be held on February 21, 2024 at 1:30 p.m. CET (7:30 a.m. EST). All investors are cordially invited to follow the conference call in a live audio webcast at https://www.fresenius.com/investors. Following the call, a replay will be available on our website.

Michael Sen, CEO of Fresenius: “We took decisive actions in fiscal year 2023 and put Fresenius back on track. #FutureFresenius is driving improvements throughout the company and creating value. We added focus, simplified the structure, and delivered better financial performance. We will build on that momentum to further grow our businesses and accelerate earnings growth driven by the Operating Companies Fresenius Kabi and Fresenius Helios. Fresenius is uniquely positioned to address the rising demand for healthcare leveraging innovations also in digitalization and AI. We are deepening our purpose of Advancing Patient Care.”

2024 Strategic priorities

After a year of significant structural progression in the Group and improved operating performance, Fresenius’ priorities in 2024 will focus on financial progression. This includes driving down leverage, execute on raised cost savings target and a rigorous focus on capital efficiency and returns. This bundle of measures is expected to translate into accelerated earnings growth in 2024 and beyond.

Fresenius is uniquely positioned to benefit from the mega trends of the healthcare sector, including growing and ageing populations, and digitalization. With its leading position in the European private hospital market and at a vast number of ambulatory clinics, the company has direct access to about 26 million patients. In addition, innovative MedTech devices and an integrated end-to-end Biopharma platform enable crucial therapies for the future. These strong platforms form a highly robust, earnings-enhancing business model in attractive growth areas.

Deconsolidation of Fresenius Medical Care successfully completed