- Fresenius Kabi with continued good growth in Q1/19

- Helios Germany stabilized; Helios Spain with continued dynamic growth

- Fresenius Medical Care with strong financial performance supported by agreements that materialized earlier than planned

- Growth investments on track

- Group guidance confirmed despite expected earnings dilution from NxStage

1 Adjusted for IFRS 16 effect

2 Q1/18 adjusted for divestitures of Care Coordination activities at FMC

3 Net income attributable to shareholders of Fresenius SE & Co. KGaA

Group guidance for 2019 confirmed

After closing the NxStage acquisition on February 21, the related sales and earnings contributions are now included in the Group guidance. Despite the expected earnings dilution from NxStage, Fresenius confirms its FY/19 guidance. Fresenius projects sales growth1 of 3% to 6% in constant currency. Net income2,3 growth is expected to be ~0% in constant currency.

Including the NxStage acquisition which is increasing the net debt/EBITDA ratio in 2019 by ~30 basis points and excluding IFRS 16, Fresenius now expects year-end 2019 net debt/EBITDA ratio to be at the upper-end of the original self-imposed target corridor of 2.5 to 3.0x.

Due to the adoption of the IFRS 16 accounting standard (“IFRS 16 effect”), Fresenius increases its self-imposed target corridor of 2.5x to 3.0x net debt/EBITDA to 3.0x to 3.5x.

1 On a comparable basis: FY/18 base: €33,009 million; FY/18 adjusted for divestitures of Care Coordination activities at FMC (H1/18); FY/19: adjusted for IFRS 16 effect

2 Net income attributable to shareholders of Fresenius SE & Co. KGaA

3 On a comparable basis: FY/18 base: €1,872 million; FY/18 before special items and adjusted for divestitures of Care Coordination activities at FMC (H1/18); FY/19: before special items (transaction-related expenses, expenses associated with the cost optimization program at FMC, revaluations of biosimilars contingent liabilities); adjusted for IFRS 16 effect

4 Both net debt and EBITDA calculated at expected annual average exchange rates; excluding further potential acquisitions

For a detailed overview of special items and adjustments please see the reconciliation tables on pages 19-22 of the PDF file.

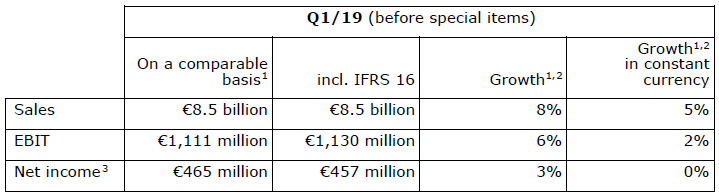

5% sales growth1 in constant currency

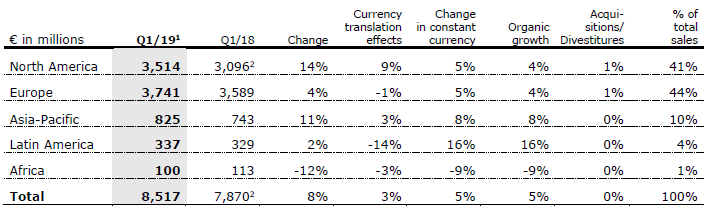

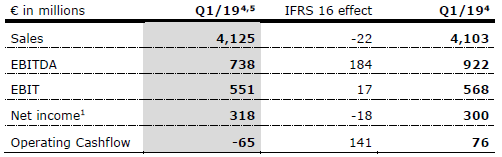

Group sales were €8,495 million including an IFRS 16 effect of -€22 million. Group sales1 on a comparable basis increased by 8% (5% in constant currency) to €8,517 million (Q1/18: €7,870 million). Organic sales growth was 5%. Acquisitions/divestitures contributed net 0% to growth. Positive currency translation effects of 3% were mainly driven by the appreciation of the U.S. dollar against the euro.

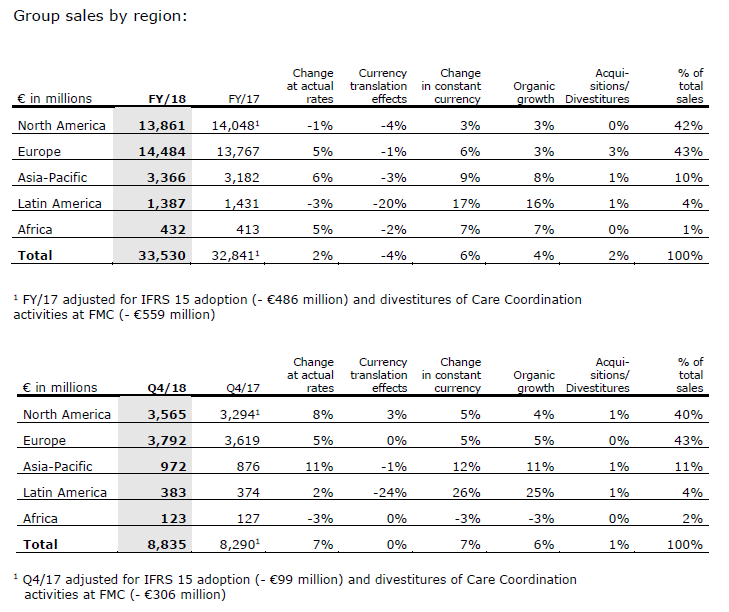

Group sales by region:

1 On a comparable basis: Q1/18 adjusted for divestitures of Care Coordination activities at FMC; Q1/19 adjusted for IFRS 16 effect

For a detailed overview of special items and adjustments please see the reconciliation tables on pages 19-22 of the PDF file.

Net income1,2 growth flat in constant currency

Group EBITDA before special items was €1,701 million including an IFRS 16 effect of €220 million. Group EBITDA2 on a comparable basis increased by 6% (3% in constant currency) to €1,481 million (Q1/18: €1,394 million).

Group EBIT before special items was €1,130 million including an IFRS 16 effect of €19 million. Group EBIT2 on a comparable basis increased by 6% (2% in constant currency) to €1,111 million (Q1/18: €1,050 million). The EBIT margin2 on a comparable basis was 13.0% (Q1/18: 13.3%). Reported Group EBIT was €1,115 million.

Group net interest before special items was -€181 million including an IFRS 16 effect of -€48 million. On a comparable basis, net interest2 improved to -€133 million (Q1/18: -€139 million) mainly due to lower rates for refinancing activities. Reported Group net interest was -€184 million.

Group tax rate before special items and adopting IFRS 16 was 23.3%. Group tax rate2 on a comparable basis was 23.4% (Q1/18: 20.9%). The prior-year was positively influenced by one-time effects related to the adoption of the U.S. tax reform.

Noncontrolling interest before special items was €271 million including an IFRS 16 effect of €13 million. Noncontrolling interest2 on a comparable basis was €284 million (Q1/18: €270 million), of which 94% was attributable to the noncontrolling interest in Fresenius Medical Care.

Group net income1 before special items was €457 million including an IFRS 16 effect of -€8 million. Group net income1,2 on a comparable basis increased by 3% (0% in constant currency) to €465 million (Q1/18: €451million). Reported Group net income1,3 was €453 million.

Earnings per share1 before special items was €0.82 including an IFRS 16 effect of -€0.02.

Earnings per share1 before special items was €0.82 including an IFRS 16 effect of -€0.02. Earnings per share1,2 on a comparable basis increased by 3% (0% in constant currency) to €0.84 (Q1/18: €0.81). Reported Earnings per share1,3 was €0.81.

1 Net income attributable to shareholders of Fresenius SE & Co. KGaA

2 On a comparable basis: Q1/19 before special items and adjusted for IFRS 16 effect; Q1/18 adjusted for divestitures of Care Coordination activities at FMC

3 After special items and including IFRS 16 effect

For a detailed overview of special items and adjustments please see the reconciliation tables on pages 19-22 of the PDF file.

Continued investment in growth

2019 is an investment year for the Fresenius Group. Fresenius is making good progress in all of its investment initiatives to secure long-term sustainable growth. Spending on property, plant and equipment was €441 million (Q1/18: €380 million), primarily for the modernization and expansion of dialysis clinics, production facilities as well as hospitals and day clinics. This corresponds to 5% of sales.

Total acquisition spending was €1,923 million (Q1/18: €192 million), mainly for the acquisition of NxStage.

Cash flow development

Group operating cash flow was €289 million including an IFRS 16 effect of €171 million. On a comparable basis, Group operating cash flow was €118 million (Q1/18: €236 million) with a margin of 1.4% (Q1/18: 2.9%). After a strong Q4/18, operating cash flow was impacted by working capital changes at Fresenius Kabi, for example by some phasing of payments and stockbuild to prepare for a possible Brexit. Moreover, as in previous years’ first quarters, operating cash flow was influenced by the seasonality in invoicing at Fresenius Medical Care North America. Fresenius does not expect these temporary effects to have a significant impact on FY/19 cash flow.

Given the effects described above in combination with increasing investments, free cash flow before acquisitions and dividends adjusted for IFRS 16 was -€339 million (Q1/18: - €155 million). Free cash flow after acquisitions and dividends adjusted for IFRS 16 was -€2,282 million (Q1/18: -€389 million). The IFRS 16 effect amounts to €171 million respectively. Correspondingly, cash flow from financing activities declined by €171 million.

Solid balance sheet structure

The Group’s total assets were €64,985 million including an IFRS 16 effect of €5,669 million. Adjusted for IFRS 16, Group total assets1 increased by 5% (3% in constant currency) to €59,316 million (Dec. 31, 2018: €56,703 million). Current assets1 grew by 1% (0% in constant currency) to €14,958 million (Dec. 31, 2018: €14,790 million). Non-current assets1 increased by 6% (5% in constant currency) to €44,358 million (Dec. 31, 2018: € 41,913 million).

Total shareholders’ equity was €25,830 million including an IFRS 16 effect of -€167 million. Adjusted for IFRS 16, total shareholders’ equity1 increased by 4% (2% in constant currency) to €25,997 million (Dec. 31, 2018: €25,008 million). The equity ratio was 39.7%. Adjusted for IFRS 16, the equity ratio was 43.8% (Dec. 31, 2018: 44.1%).

Group debt was €26,378 million including an IFRS 16 effect of €5,836 million. Adjusted for IFRS 16, Group debt1 increased by 8% to €20,542 million (8% in constant currency) (Dec. 31, 2018: € 18,984 million). Group net debt was €24,835 million including an IFRS 16 effect of €5,836 million. Adjusted for IFRS 16, Group net debt1 increased by 17% (16% in constant currency) to € 18,999 million (Dec. 31, 2018: € 16,275 million) mainly due to the acquisition of NxStage by Fresenius Medical Care and the negative free cash flow.

As of March 31, 2019, the net debt/EBITDA ratio increased to 3.091,2,3 (December 31, 2018: 2.712,3). Excluding the acquisition of NxStage the net debt/EBITDA ratio was 2.831,2,3 as of March 31, 2019. Including the IFRS 16 effect, the reported net debt/EBITDA ratio increased to 3.532,3.

1 Adjusted for IFRS 16 effect

2 At LTM average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures

3 Before special items

For a detailed overview of special items and adjustments please see the reconciliation tables on pages 19-22 of the PDF file.

Business Segments

Fresenius Medical Care (Figures according to Fresenius Medical Care Investor News)

Fresenius Medical Care is the world's largest provider of products and services for individuals with renal diseases. As of March 31, 2019, Fresenius Medical Care was treating 336,716 patients in 3,971 dialysis clinics. Along with its core business, the company provides related medical services in the field of Care Coordination.

- 6% sales1,2 growth in constant currency

- Earnings supported by agreements that materialized earlier than planned

- Outlook confirmed

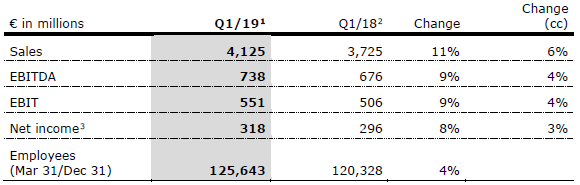

Adjusted for the Q1/18 contribution from the divested Care Coordination activities, the effect of the adoption of the IFRS 16 accounting standard (“IFRS 16 effect”) and the contribution from NxStage, sales increased by 11% (6% at constant currency) to €4,125 million (Q1/18: €3,725 million). Organic sales growth was 6%. Positive currency translation effects of 5% were mainly related to the appreciation of the U.S. dollar against the euro.

Health Care Services sales1,2 increased by 12% (6% at constant currency) to €3,316 million (Q1/18: €2,958 million). Health Care Products sales1,2 increased by 5% (4% at constant currency) to €809 million (Q1/18: €767 million).

In North America, sales1,2 increased by 14% (5% in constant currency) to €2,879 million (Q1/18: €2,523 million). Health Care Services sales1,2 increased by 14% (6% in constant currency) to €2,679 million (Q1/18: €2,339 million).

1 On an adjusted basis: before expenses associated with the cost optimization program, the IFRS 16 effect, excluding effects from NxStage transaction

2 Q1/18 adjusted for divestitures of Care Coordination activities

3 Net income attributable to shareholders of Fresenius Medical Care AG & Co. KGaA

For a detailed overview of special items and adjustments please see the reconciliation tables on pages 19-22 of the PDF file.

Sales2 outside North America increased by 4% (6% in constant currency) to €1,246 million (Q1/18: €1,202 million). Health Care Services sales2 increased by 3% (8% in constant currency) to €637 million (Q1/18: €619 million). Health Care Product sales2 adjusted increased by 4% (5% in constant currency) to €609 million (Q1/18: €583 million).

Fresenius Medical Care’s EBIT3 increased by 9% (4% in constant currency) to €551 million (Q1/18: €506 million). The EBIT margin3 decreased to 13.4% (Q1/18: 13.6%).

Net income1,3 increased by 8% (3% in constant currency) to €318 million (Q1/18: €296 million).

Operating cash flow was €76 million (Q1/18: -€45 million) with a margin of 1.8% (Q1/18: -1.1%). The increase was mainly driven by the adoption of the IFRS 16 accounting standard leading to a reclassification of the repayment portion of rent to financing activities (€141 million). Adjusted for the IFRS 16 effect, operating cash flow was -€65 million.

For FY/19, Fresenius Medical Care expects adjusted sales to grow by 3% to 7%2,6 in constant currency. Net income1 is expected to develop in the range of -2% to +2%3,7 in constant currency.

For further information, please see Fresenius Medical Care’s Investor News at www.freseniusmedicalcare.com.

1 Net income attributable to shareholders of Fresenius Medical Care AG & Co. KGaA

2 Q1/18 adjusted for divestitures of Care Coordination activities; Q1/19 adjusted for IFRS 16 effects, excluding effects from NxStage transaction

3 Q1/18 before special items and after adjustments; Q1/19 before special items (before transaction-related expenses, expenses associated with the cost optimization program), adjusted for IFRS 16 effect, excluding effects from NxStage transaction

4 Before special items (operating cash flow after special items)

5 Adjusted for IFRS 16 effect

6 FY/18 base: €16,026 million

7 FY/18 base: €1,341 million

For a detailed overview of special items and adjustments please see the reconciliation tables on pages 19-22 of the PDF file.

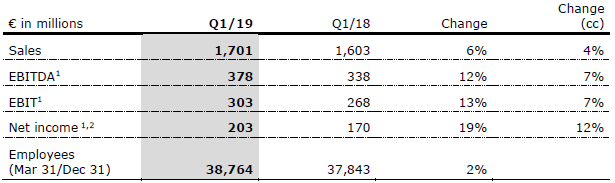

Fresenius Kabi

Fresenius Kabi offers intravenously administered generic drugs, clinical nutrition and infusion therapies for seriously and chronically ill patients in the hospital and outpatient environments. The company is also a leading supplier of medical devices and transfusion technology products. In the biosimilars business, Fresenius Kabi develops products with a focus on oncology and autoimmune diseases.

- 4% organic sales growth and 7% EBIT1 growth in constant currency

- High prior-year base impacts organic sales growth in North America

- FY/19 outlook confirmed

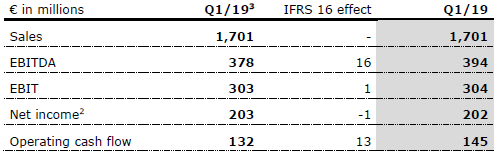

Sales increased by 6% (4% in constant currency) to €1,701 million (Q1/18: €1,603 million). Organic sales growth was 4%. Positive currency translation effects of 2% were mainly related to the appreciation of the U.S. dollar against the euro.

Sales in Europe grew by 3% (organic growth: 3%) to €573 million (Q1/18: €557 million). Sales in North America increased by 5% (decreased organically by 2% from a high prior-year basis) to €623 million (Q1/18: €591 million). Sales in Asia-Pacific increased by 13% (organic growth: 11%) to €341 million (Q1/18: €301 million). Sales in Latin America/Africa increased by 6% (organic growth: 18%) to €164 million (Q1/18: €154 million).

EBIT1 increased by 13% (7% in constant currency) to €303 million (Q1/18: €268 million) with an EBIT margin1 of 17.8% (Q1/18: 16.7%).

Net income1,2 increased by 19% (12% in constant currency) to €203 million (Q1/18: €170 million).

Operating cash flow3 was €132 million (Q1/18: €226 million). After a strong Q4/18, operating cash flow was impacted by working capital changes, for example by some phasing of payments and stockbuild to prepare for a possible Brexit. The cash flow margin was 7.8% (Q1/18: 14.1%).

Fresenius Kabi confirms its outlook for FY/19 and expects organic sales growth4 of 3% to 6% and EBIT growth5 in constant currency of 3% to 6%.

1 On a comparable basis: before special items and adjusted for IFRS 16 effect

2 Net income attributable to shareholders of Fresenius SE & Co. KGaA

3 Adjusted for IFRS 16 effect, before special items (operating cash flow after special items)

4 On a comparable basis: FY/18 base: €6,544 million; FY/19 before special items (acquisition-related expenses, revaluations of biosimilars contingent liabilities) and adjusted for IFRS 16 effect

5 On a comparable basis: FY/18 base: €1,139 million; FY/18 before special items; FY/19 before special items (acquisition-related expenses, revaluations of biosimilars contingent liabilities) and adjusted for IFRS 16 effect.

For a detailed overview of special items and adjustments please see the reconciliation tables on pages 19-22 of the PDF file.

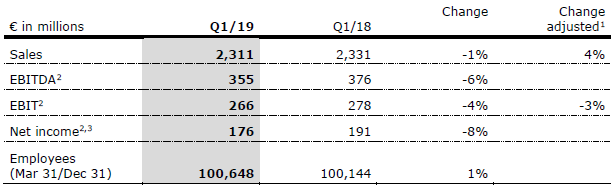

Fresenius Helios

Fresenius Helios is Europe's leading private hospital operator. The company comprises Helios Germany and Helios Spain (Quirónsalud). Helios Germany operates 86 hospitals, ~125 outpatient centers and treats approximately 5.3 million patients annually. Quirónsalud operates 47 hospitals, 56 outpatient centers and around 300 occupational risk prevention centers, and treats approximately 13.3 million patients annually.

- 4% organic sales growth

- Helios Germany stabilized; Helios Spain with continued dynamic growth

- FY/19 outlook confirmed

Sales decreased by 1% (increased by 4%1; organic growth: 4%) to €2,311 million (Q1/18: €2,331 million).

Sales of Helios Germany decreased by 6% (increased by 1%1; organic growth: 2%) to €1,485 million (Q1/18: €1,574 million). Sales were impacted by a decline in admissions in Germany, partially due to the transfer of the post-acute care business from Helios to Vamed, a shortage of nurses at selected intensive care units and a less pronounced flu season. The admission decline was more than compensated by positive price effects.

Helios Spain increased sales by 9% (organic growth: 9%) to €826 million (Q1/18: €757 million), mainly driven by the private sector. The occupational risk prevention business also had a valuable contribution. Performance in Q1/18 was impacted by the Easter holidays.

1 Adjusted for the post-acute care business transferred to Fresenius Vamed as of July 1, 2018

2 Adjusted for IFRS 16 effect

3 Net income attributable to shareholders of Fresenius SE & Co. KGaA

For a detailed overview of special items and adjustments please see the reconciliation tables on pages 19-22 of the PDF file.

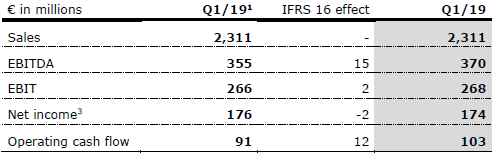

EBIT1 of Fresenius Helios decreased by 4% (-3%2) to €266 million (Q1/18: €278 million) with an EBIT margin of 11.5% (Q1/18: 11.9%).

EBIT1 of Helios Germany decreased by 16% (-14%2) to €149 million (Q1/18: €177 million). The EBIT margin improved sequentially by 50 bps to 10.0% (Q4/18: 9.5%). The development of Helios Germany is impacted by the admissions decline and the investments for preparatory structural measures.

EBIT1 of Helios Spain increased by 16% to €119 million (Q1/18: €103 million), mainly due to the strong operating performance with an EBIT margin of 14.4% (Q1/18: 13.6%).

Net income1,3 decreased by 8% to €176 million (Q1/18: €191 million).

Operating cash flow1 was €91 million (Q1/18: €97 million) with a margin of 3.9% (Q1/18: 4.2%). The decrease is mainly attributable to the increase in days sales outstanding (DSO).

Fresenius Helios confirms its outlook for FY/19 and expects organic sales growth of 2% to 5% and an EBIT1 growth of -5% to -2%.

1 Adjusted for IFRS 16 effect

2 Adjusted for the post-acute care business transferred to Fresenius Vamed as of July 1, 2018

3 Net income attributable to shareholders of Fresenius SE & Co. KGaA

For a detailed overview of special items and adjustments please see the reconciliation tables on pages 19-22 of the PDF file.

Fresenius Vamed

Fresenius Vamed manages projects and provides services for hospitals and other health care facilities worldwide and is a leading post-acute care provider in Central Europe. The portfolio ranges along the entire value chain: from project development, planning, and turnkey construction, via maintenance and technical management to total operational management.

- Excellent organic sales growth of 31%

- Order backlog at all-time high ‒ strong foundation for future growth

- FY/19 outlook confirmed

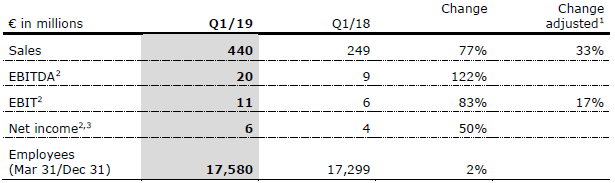

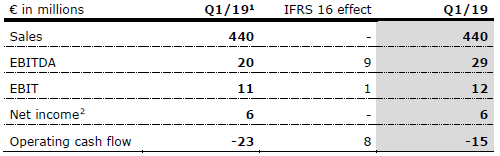

Sales increased by 77% (33%1) to €440 million (Q1/18: €249 million). Organic sales growth was 31%, acquisitions contributed 2% to growth. Both the project and the service business showed strong momentum. Sales of the project business increased by 17% to €108 million (Q1/18: €92 million). Sales in the service business grew by 111% (41%1) to €332 million (Q1/18: €157 million), supported by an intensified collaboration with Fresenius Helios.

In Q1/19, EBIT2 increased by 83% (83%2 in constant currency) to €11 million (Q1/18: €6 million) with an EBIT margin of 2.5% (Q1/18: 2.4%). EBIT2 additionally adjusted for the acquisition of the German post-acute care business was €7 million with an EBIT margin of 2.1%.

Net income2,3 increased by 50% to €6 million (Q1/18: €4 million).

Order intake increased by 47% to €383 million (Q1/18: €260 million). As of March 31, 2019, order backlog reached a new all-time high of €2,698 million (Dec 31, 2018: €2,420 million).

Operating cash flow2 increased by 45% to €-23 million (Q1/18: €-42 million) with a margin of -5.2% (Q1/18: -16.9%).

Fresenius Vamed confirms its outlook for FY/19 and expects organic sales growth of ~10% and EBIT growth2 of 15% to 20%.

1 Adjusted for German post-acute care business acquired from Fresenius Helios as of July 1, 2018

2 Adjusted for IFRS 16 effect

3 Net income attributable to shareholders of VAMED AG

For a detailed overview of special items and adjustments please see the reconciliation tables on pages 19-22 of the PDF file.

Conference Call

As part of the publication of the results for the first quarter 2019, a conference call will be held on May 2, 2019 at 1:30 p.m. CET (7:30 a.m. EST). All investors are cordially invited to follow the conference call in a live broadcast over the Internet at www.fresenius.com/investors. Following the call, a replay will be available on our website.

For additional information on the performance indicators used please refer to our website www.fresenius.com/alternative-performance-measures.

This release contains forward-looking statements that are subject to various risks and uncertainties. Future results could differ materially from those described in these forward-looking statements due to certain factors, e.g. changes in business, economic and competitive conditions, regulatory reforms, results of clinical trials, foreign exchange rate fluctuations, uncertainties in litigation or investigative proceedings, and the availability of financing. Fresenius does not undertake any responsibility to update the forward-looking statements in this release.

- Delivered on FY/18 Group targets

- Fresenius Kabi to show continued growth

- Helios Germany impacted by regulatory changes and initiatives to secure medium-term growth; Helios Spain to show continuous dynamic growth

- 26th consecutive dividend increase proposed

- Healthy growth targets for 2020 – 2023; consistent with expectations from December 2018

1 Growth rate adjusted for IFRS 15 adoption and divestitures of Care Coordination activities (Q4/17 base: €8,290 million; FY/17 base: €32,841 million)

2 Before special items and after adjustments

3 Net income attributable to shareholders of Fresenius SE & Co. KGaA

For a detailed overview of special items and adjustments please see the reconciliation tables on pages 21-24 of the pdf file.

Group expectations for FY/19 confirmed

For FY/19, Fresenius projects sales growth1 of 3% to 6% in constant currency. Net income2,3 growth is expected to be ~0% in constant currency. NxStage is not included in this guidance because the acquisition is not closed yet and Fresenius does not expect a significant impact on its Group guidance metrics. This guidance is in line with the expectations announced on December 6, 2018.

Fresenius expects its year-end 2019 net debt/EBITDA4 ratio to be broadly stable over the year-end 2018 figure.

Fresenius intends to further increase its dividend for FY 2019.

Healthy growth targets5 for 2020 – 2023

Based on the expected financial results for FY/19, Group sales are projected to grow organically with a compounded annual growth rate (CAGR) of 4% to 7% in 2020 to 2023. Group net income2 is projected to increase organically with a CAGR of 5% to 9% in 2020 to 2023. Fresenius expects its launched and contemplated sales growth and efficiency improvement initiatives as well as the expected break-even of Fresenius Kabi’s biosimilars business to drive an acceleration of Group earnings growth over that period. Small and medium-sized acquisitions are expected to contribute an incremental CAGR of approx. 1%-point to both sales and net income growth.

1 FY/18 base: €33,009 million; FY/18 adjusted for divestitures of Care Coordination activities at FMC (H1/18); FY/19: adjusted for IFRS 16 effects; excluding effects from pending acquisition of NxStage by FMC

2 Net income attributable to shareholders of Fresenius SE & Co. KGaA

3 FY/18 base: €1,872 million; FY/18 before special items and after adjustments; FY/19 before special items (transcation-related expenses, expenses associated with the cost optimization program at FMC, revaluations of biosimilars contingent liabilities); adjusted for IFRS 16 effects; excluding effects from pending acquisition of NxStage by FMC

4 Both net debt and EBITDA calculated at expected annual average exchange rates; excluding effects from pending acquisition of NxStage by FMC; excluding further potential acquisitions; adjusted for IFRS 16 effects

5 Before special items

For a detailed overview of special items and adjustments please see the reconciliation tables on pages 21-24 of the pdf file.

26th consecutive dividend increase proposed

Consistent with Fresenius’ stated dividend policy, the Management Board will propose to the Supervisory Board a 7% increase in the dividend for FY/18 to €0.80 per share (2017: €0.75). The proposed total dividend payout to Fresenius SE & Co. KGaA shareholders amounts to €445 million.

6% sales growth in constant currency1

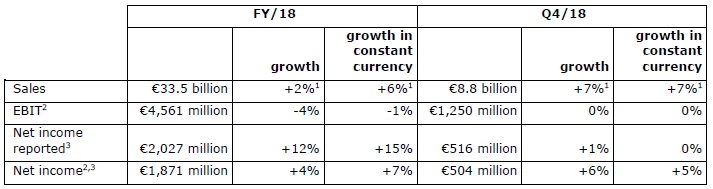

Group sales1 increased by 2%1 (6%1 in constant currency) to €33,530 million (FY/17: €32,841 million). Organic sales growth was 4%1. Acquisitions/divestitures contributed net 2%1 to growth. Negative currency translation effects of 4%1 were mainly driven by the devaluation of the U.S. dollar and the Argentinian peso against the euro.

In Q4/18, Group sales1 increased by 7%1 (7%1 in constant currency) to €8,835 million (Q4/17: €8,290 million). Organic sales1 growth was 6%1. Acquisitions/divestitures contributed net 1%1 to growth. There were no meaningful currency translation effects.

7% net income1,2 growth in constant currency

Group EBITDA2 decreased by 3%2 (0%2 in constant currency) to €5,991 million (FY/17: €6,174 million). Group EBIT2 decreased by 4%2 (-1%2 in constant currency) to €4,561 million (FY/17: €4,746 million). The EBIT margin2 was 13.6% (FY/17: 14.5%). Group EBIT2 before expenses for the further development of the biosimilars business decreased by 2%2 (increased by 1%2 in constant currency) to €4,727 million. In FY/17, the compensation for treatments of U.S. war veterans (“VA agreement”) had contributed €87 million as a one-time effect. Group EBIT2 excluding the VA agreement and expenses for the further development of the biosimilars business increased by 3% in constant currency.

In Q4/18, Group EBIT2 was broadly stable year-over-year2 (broadly stable2 in constant currency) at €1,250 million (Q4/17: €1,244 million), with an EBIT margin2 of 14.1% (Q4/17: 15.0%). Group EBIT2 excluding the prior-year VA agreement and expenses for the further development of the biosimilars business was also broadly stable year-over-year2 in constant currency.

Group net interest2 was -€570 million (FY/17: -€630 million). The decrease was mainly driven by refinancings at lower rates, lower debt, currency effects as well as proceeds from the divestitures of Care Coordination activities at Fresenius Medical Care.

The decrease of the Group tax rate2 to 22.0% (FY/17: 27.9%) was mainly due to the U.S. tax reform and some related one-time effects at Fresenius Medical Care and Fresenius Kabi. In Q4/18, the Group tax rate2 was 22.6% (Q4/17: 28.0%).

Noncontrolling interest2 was €1,240 million (2017: €1,164 million), of which 94% was attributable to the noncontrolling interest in Fresenius Medical Care.

1Net income attributable to shareholders of Fresenius SE & Co. KGaA

2Before special items and after adjustments

Group net income1,2 increased by 12% (15% in constant currency) to €2,027 million (FY/17: €1,814 million), mainly due to gains related to divestitures of Care Coordination activities at Fresenius Medical Care. Earnings per share1,2 increased by 12% (15% in constant currency) to €3.65 (FY/17: €3.27). In Q4/18, Group net income1,2 increased by 1% (0% in constant currency) to €516 million (Q4/17: €511 million). Earnings per share1,2 increased by 1% (0% in constant currency) to €0.93 (Q4/17: €0.92).

Group net income1,3 before special items increased by 3% (6% in constant currency) to €1,871 million (FY/17: €1,816 million). Earnings per share1,3 increased by 3% (6% in constant currency) to €3.37 (FY/17: €3.28). In Q4/18, Group net income1,3 increased by 3% (3% in constant currency) to €504 million (Q4/17: €487 million). Earnings per share1,3 increased by 3% (3% in constant currency) to €0.91 (Q4/17: €0.88).

Group net income1,4 before special items and after adjustments increased by 4% (7% in constant currency) to €1,871 million (FY/17: €1,804 million). Earnings per share1,4 increased by 3% (6% in constant currency) to €3.37 (FY/17: €3.26). In Q4/18, Group net income1,4 increased by 6% (5% in constant currency) to €504 million (Q4/17: €477 million). Earnings per share1,4 increased by 6% (5% in constant currency) to €0.91 (Q4/17: €0.86).

Group net income1,4,5 before expenses for the further development of the biosimilars business increased by 8% (11% in constant currency) to €1,991 million (2017: €1,847 million). Earnings per share1,4,5 increased by 8% (11% in constant currency) to €3.58 (2017: €3.33). In Q4/18, Group net income1,4,5 increased by 6% (6% in constant currency) to €542 million (Q4/17: €510 million). Earnings per share1,4,5 increased by 5% (5% in constant currency) to €0.97 (Q4/17: €0.92).

1Net income attributable to shareholders of Fresenius SE & Co. KGaA

2After special items

3Before special items

4Before special items and after adjustments

5Before expenses for the further development of the biosimilar business

Continued investment in growth

Spending on property, plant and equipment was €2,163 million (FY/17: €1,828 million), primarily for the modernization and expansion of dialysis clinics, production facilities as well as hospitals and day clinics. This corresponds to 6% of sales.

Total acquisition spending was €1,086 million (FY/17: €6,852 million). FY/17 spending had included the acquisition of Quirónsalud as well as the acquisition of the biosimilars business of Merck KGaA.

Cash flow development

Group operating cash flow decreased by 5% to €3,742 million (FY/17: €3,937 million) with a margin of 11.2% (FY/17: 11.6%). In FY/17 Fresenius Medical Care had received a ~€200 million payment under the VA agreement. The FY/18 cash flow was impacted by a change in working capital items at Fresenius Helios, the earnings decrease at Helios Germany and negative currency translation effects. Operating cash flow in Q4/18 increased by 7% to €1,193 million (Q4/17: €1,116 million) with a margin of 13.5% (Q4/17: 12.8%).

Given the effects described above in combination with growing investments, free cash flow before acquisitions and dividends decreased to €1,665 million (FY/17: €2,232 million). Free cash flow after acquisitions and dividends was €1,374 million (FY/17: -€4,557 million).

Solid balance sheet structure

The Group’s total assets increased by 7% (5% in constant currency) to €56,703 million (Dec. 31, 2017: €53,133 million). Current assets grew by 17% (17% in constant currency) to €14,790 million (Dec. 31, 2017: €12,604 million). Non-current assets increased by 3% (2% in constant currency) to €41,913 million (Dec. 31, 2017: €40,529 million).

Total shareholders’ equity increased by 15% (13% in constant currency) to €25,008 million (Dec. 31, 2017: €21,720 million). The equity ratio increased to 44.1% (Dec. 31, 2017: 40.9%).

Group debt was broadly stable (decreased by 2% in constant currency) at €18,984 million (Dec. 31, 2017: €19,042 million). Group net debt decreased by 6% (-8% in constant currency) to €16,275 million (Dec. 31, 2017: €17,406 million) mainly due to the proceeds from divestitures of Care Coordination activities at Fresenius Medical Care.

As of December 31, 2018, the net debt/EBITDA ratio was 2.711,2 (December 31, 2017: 2.841,2). Excluding the proceeds from divestitures of Care Coordination activities the net debt/EBITDA ratio was 2.911,2.

1At LTM average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures, excluding effects from pending acquisition of NxStage by FMC

2Before special items

Business Segments

Fresenius Medical Care

Fresenius Medical Care is the world's largest provider of products and services for individuals with renal diseases. As of December 31, 2018, Fresenius Medical Care was treating 333,331 patients in 3,928 dialysis clinics. Along with its core business, the company provides related medical services in the field of Care Coordination.

- 7% comparable sales growth in constant currency in Q4/18

- 9% comparable2 net income increase in constant currency in Q4/18

- Attractive share buyback program for 2019 and 2020

- Outlook for FY/19 (in constant currency): 3% to 7% adjusted sales growth3 and adjusted net income development4 in range of -2% to +2% expected

1Excluding VA agreement Q4/18: 6%; FY/18: 4%

2Net income attributable to shareholders of Fresenius Medical Care AG & Co. KGaA

3FY/18 base: €16,026 million; FY/18 adjusted for divestitures of Care Coordination activities; FY/19 adjusted for IFRS 16 effects, excluding effects from pending NxStage transaction

4FY/18 base: €1,341 million; FY/18 before special items and after adjustments; FY/19 before special items (before transcation-related expenses, expenses associated with the cost optimization program), adjusted for IFRS 16 effects, excluding effects from pending NxStage transaction

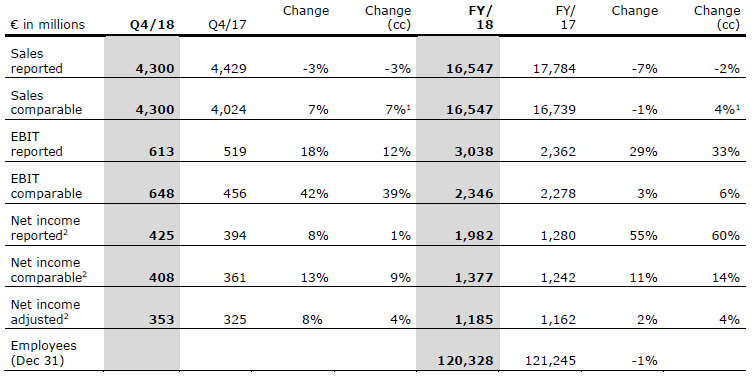

Sales decreased by 7% (-2% in constant currency) to €16,547 million (FY/17: €17,784 million). Organic sales growth was 4%. Currency translation effects reduced sales by 5%. The adoption of IFRS 15 reduced sales by 3%.

With the FY/17 base additionally adjusted for divestitures of Care Coordination activities, sales decreased by 1% (increased by 4% in constant currency).

In Q4/18, sales decreased by 3% (-3% in constant currency) to €4,300 million (Q4/17: €4,429 million). Organic sales growth was 6%. The adoption of IFRS 15 reduced sales by 2%. Q4/17 base additionally adjusted for divestitures of Care Coordination activities, sales in Q4/18 increased by 7% (7% in constant currency).

Health Care services sales1 (dialysis services and care coordination) decreased by 2% (increased by 4% in constant currency) to €13,264 million (FY/17: €13,487 million). Health Care product sales increased by 1% (5% in constant currency) to €3,283 million (FY/17: €3,252 million).

In North America, sales1 decreased by 2% (increased by 2% in constant currency) to €11,570 million (FY/17: €11,834 million). Health Care services sales1 decreased by 2% (increased by 2% in constant currency) to €10,725 million (FY/17: €10,991 million). Excluding the FY/17 effect from the VA Agreement (€94 million), Health Care services sales1 increased by 3% in constant currency. Health Care product sales of €845 million (FY/17: €843 million) were on the prior-year level (increased by 5% in constant currency).

1On a comparable basis

Sales outside North America increased by 1% (8% in constant currency) to €4,962 million (FY/17: €4,890 million). Health Care services sales increased by 2% (11% in constant currency) to €2,539 million (FY/17: €2,496 million). Health Care product sales increased by 1% (5% in constant currency) to €2,423 million (FY/17: €2,394 million).

Fresenius Medical Care’s EBIT increased by 29% (33% in constant currency) to €3,038 million (FY/17: €2,362 million), mainly driven by gains related to divestitures of Care Coordination activities. The EBIT margin increased to 18.4% (FY/17: 13.3%). EBIT on a comparable basis increased by 6% in constant currency and EBIT margin increased to 14.2% (FY/17: 13.6%).

In Q4/18, EBIT increased by 18% (12% in constant currency) to €613 million (Q4/17: €519 million). The EBIT margin increased to 14.3% (Q4/17: 11.7%). EBIT on a comparable basis increased by 42% (increased by 39% in constant currency) and EBIT margin increased to 15.1% (Q4/17: 11.3%).

Net income1 increased by 55% (60% in constant currency) to €1,982 million (FY/17: €1,280 million). Net income1 growth on a comparable basis was 14% in constant currency. Adjusted net income1 growth was 4% in constant currency.

In Q4/18, net income1 increased by 8% (1% in constant currency) to €425 million (Q4/17: €394 million). Net income1 growth on a comparable basis was 9% in constant currency. Adjusted net income1 growth was 4% in constant currency.

Operating cash flow was €2,062 million (FY/17: €2,192 million). The cash flow margin increased to 12.5% (FY/17: 12.3%). In Q4/18, operating cash flow was €698 million (Q4/17: €528 million). The cash flow margin increased to 16.2% (Q4/17: 11.9%).

For FY/19, Fresenius Medical Care expects adjusted sales to grow by 3% to 7%2 in constant currency. Net income1 is expected to develop in the range of -2% to +2%3 in constant currency in 2019.

For 2020, Fresenius Medical Care expects adjusted sales as well as adjusted net income to grow at a mid to high single digit rate, both at constant currency.

For further information, please see Fresenius Medical Care’s Press Release at www.freseniusmedicalcare.com.

1Net income attributable to shareholders of Fresenius Medical Care AG & Co. KGaA

2FY/18 base: €16,026 million; FY/18 adjusted for divestitures of Care Coordination activities (H1/18); FY/19 adjusted for IFRS 16 effects, excluding effects from pending NxStage transaction

3FY/18 base: €1,341 million; FY/18 before special items and after adjustments; FY/19 before special items (before transaction-related expenses, expenses associated with the cost optimization program), adjusted for IFRS 16 effects, excluding effects from pending NxStage transaction

Fresenius Kabi

Fresenius Kabi offers intravenously administered generic drugs, clinical nutrition and infusion therapies for seriously and chronically ill patients in the hospital and outpatient environments. The company is also a leading supplier of medical devices and transfusion technology products. In the biosimilars business, we are developing products with a focus on oncology and autoimmune diseases.

- 7% organic sales growth and 10% EBIT1 growth in constant currency (excl. biosimilars expenses) in FY/18

- Operating cash flow at all-time high

- FY/19 outlook: 3% to 6% organic sales growth5 and 3% to 6% EBIT6 growth in constant currency expected

1Before special items

2Before expenses for the further development of the biosimilars business: Q4/18: 8%; FY/18: 10%

3Net income attributable to shareholders of Fresenius SE & Co. KGaA

4Before expenses for the further development of the biosimilars business: Q4/18: 20%; FY/18: 21%

5FY/18 base: €6,544 million; FY/19 adjusted for IFRS 16 effects

6FY/18 base: €1,139 million; FY/18 before special items including expenditures for further development of biosimilars business (€120 million after tax); FY/19 before special items (before transaction-related expenses, revaluations of biosimilars contingent liabilities), adjusted for IFRS 16 effects

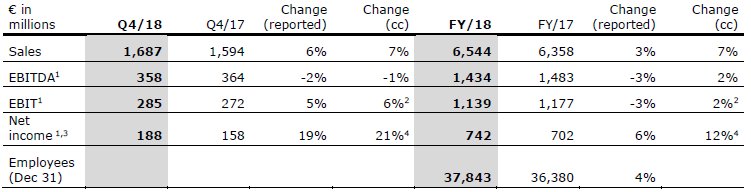

Sales increased by 3% (7% in constant currency) to €6,544 million (FY/17: €6,358 million). Organic sales growth was 7%. Strong negative currency translation effects of 4% were mainly related to the devaluation of the U.S. dollar, the Argentinian peso and the Brazilian real against the euro. In Q4/18, sales increased by 6% (7% in constant currency) to €1,687 million (Q4/17: €1,594 million). Organic sales growth was 7%.

Sales in Europe grew by 2% (organic growth: 3%) to €2,248 million (FY/17: €2,214 million). In Q4/18, sales in Europe increased by 2% (organic growth: 3%) to €590 million.

Sales in North America increased by 3% (organic growth: 8%) to €2,359 million (FY/17: €2,290 million). In Q4/18, sales increased by 8% (organic growth: 5%) to €599 million (Q4/17: €554 million).

Sales in Asia-Pacific increased by 9% (organic growth: 12%) to €1,300 million (FY/17: €1,196 million). In Q4/18, sales increased by 11% (organic growth: 13%) to €336 million (Q4/17: €302 million).

Sales in Latin America/Africa decreased by 3% (increased organically by 13%) to €637 million (FY/17: €658 million). In Q4/18, sales increased by 2% (organical growth: 18%) to €162 million (Q4/17: €159 million).

EBIT1 decreased by 3% (increased by 2% in constant currency) to €1,139 million (FY/17: €1,177 million) with an EBIT margin1 of 17.4% (FY/17: 18.5%). In Q4/18, EBIT1 increased by 5% (6% in constant currency) to €285 million (Q4/17: €272 million) with an EBIT margin1 of 16.9% (Q4/17: 17.1%).

EBIT1 before expenses for the further development of the biosimilars business increased by 5% (10% in constant currency) to €1,305 million (FY/17: €1,237 million) with an EBIT margin1 of 19.9% (FY/17: 19.5%). In Q4/18, EBIT1 before expenses for the further development of the biosimilars business increased by 6% (8% in constant currency) to €338 million (Q4/17: €318 million) with an EBIT margin1 of 20.0% (Q4/17: 19.9%).

Net income1,2 increased by 6% (12% in constant currency) to €742 million (FY/17: €702 million). In Q4/18, net income1,2 increased by 19% (21% in constant currency) to €188 million (Q4/17: €158 million).

Operating cash flow increased by 3% to on an all-time-high of €1,040 million (2017: €1,010 million), mainly driven by a strong operational performance. The cash flow margin was 15.9% (2017: 15.9%).

For FY/19, Fresenius Kabi expects organic sales growth3 of 3% to 6% and EBIT growth4 in constant currency of 3% to 6%.

1Before special items

2Net income attributable to shareholders of Fresenius SE & Co. KGaA

3FY/18 base: €6,544 million; FY/19 adjusted for IFRS 16 effects

4FY/18 base: €1,139million; FY/18 before special items including expenditures for further development of biosimilars business (€120 million after tax); FY/19 before special items (before acquisition-related expenses, revaluations of biosimilars contingent liabilities), adjusted for IFRS 16 effects

Fresenius Helios

Fresenius Helios is Europe's leading private hospital operator. The company comprises Helios Germany and Helios Spain (Quirónsalud). Helios Germany operates 86 hospitals, ~125 outpatient centers and treats approximately 5.3 million patients annually. Quirónsalud operates 47 hospitals, 57 outpatient centers and around 300 occupational risk prevention centers, and treats approximately 13.3 million patients annually.

- 4% organic sales growth in Q4/18

- DRG catalogue effects and preparatory initiatives for regulatory changes continue to weigh on Helios Germany

- Helios Spain with dynamic growth

- FY/19 outlook3: 2% to 5% organic sales growth and EBIT decline of -5% to -2% expected

As of July 1, 2018 Fresenius Helios transferred its German post-acute care business to Fresenius Vamed. To allow a like-for-like comparison, we also provide sales and EBIT growth rates adjusted for the effects of this transaction.

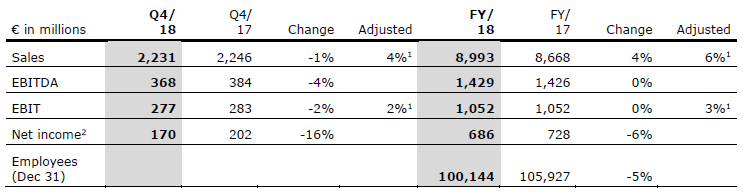

Fresenius Helios increased sales by 4% (6%1) to €8,993 million (FY/17: €8,668 million). Organic sales growth was 3%. In Q4/18, sales decreased by 1% (increased by 4%1; organic growth: 4%) to €2,231 million (Q4/17: €2,246 million).

Sales of Helios Germany decreased by 2% (increased by 2%1; organic growth: 2%) to €5,970 million (FY/17: €6,074 million). In Q4/18, sales decreased by 5% (increased by 3%1; organic growth: 3%) to €1,439 million (Q4/17: €1,512 million). Sales were impacted by a decline in admissions, inter alia due to an unexpectedly high fluctuation among doctors and a shortage of nursing staff as well as a trend towards outpatient treatments. The volume decline was offset by DRG inflator increases and better results from the negotiations with our payors.

Helios Spain increased sales by 17% (organic growth: 6%) to €3,023 million (FY/17: €2,594 million), mainly due to an excellent operating performance and an additional month of consolidation (Quirónsalud is consolidated since February 1, 2017). In Q4/18 Helios Spain increased sales by 8% (organic growth: 7%) to €792 million (Q4/17: €734 million).

Fresenius Helios EBIT remained unchanged (increased by 3%1) at €1,052 million (FY/17: €1,052 million) with a margin of 11.7% (FY/17: 12.1%). In Q4/18, EBIT decreased by 2% (increased by 2%1) to €277 million (Q4/17: €283 million) with a margin of 12.4% (Q4/17: 12.6%).

EBIT of Helios Germany decreased by 14% (-10%1) to €625 million (FY/17: €725 million) with a margin of 10.5% (FY/17: 11.9%). In Q4/18, EBIT decreased by 22% (-15%1) to €137 million (Q4/17: €176 million) with a margin of 9.5% (Q4/17: 11.6%). The significant fixed cost base in the hospital business has a strong operating leverage effect on EBIT as market dynamics and sales development slow down. The development of Helios Germany is impacted by additional catalogue effects, preparatory structural measures for expected regulatory requirements (e.g. clustering) and a lack of privatization opportunities in the German market. An unexpectedly high fluctuation among doctors and a shortage of nursing staff have an additional negative impact on the earnings development.

EBIT of Helios Spain increased by 26% to €413 million (FY/17: €327 million), mainly due to the strong operating performance and the additional month of consolidation, with a margin of 13.7% (FY/17: 12.6%). In Q4/18, EBIT increased by 19% to €127 million (Q4/17: €107 million) with a margin of 16.0% (Q4/17: 14.6%).

Net income2 of Fresenius Helios decreased by 6% to €686 million (FY/17: €728 million). In Q4/18, net income2 decreased by 16% to €170 million (Q4/17: €202 million).

Operating cash flow was €554 million (FY/17: €733 million) with a margin of 6.2% (FY/17: 8.5%). The decrease is mainly attributable to the earnings decrease at Helios Germany and the changes in working capital.

For FY/19, Fresenius Helios expects organic sales growth of 2% to 5% and an EBIT3 decline of -5% to -2%.

1Adjusted for German post-acute care business transferred to Fresenius Vamed

2Net income attributable to shareholders of Fresenius SE & Co. KGaA

3Adjusted for IFRS 16 effects

Fresenius Vamed

Fresenius Vamed manages projects and provides services for hospitals and other health care facilities worldwide and is a leading post-acute care provider in Central Europe. The portfolio ranges along the entire value chain: from project development, planning, and turnkey construction, via maintenance and technical management to total operational management.

- Excellent organic sales growth of 16% in FY/18

- Order intake at all-time high - strong foundation for future growth

- FY/19 outlook: ~10% organic sales growth and 15% to 20% EBIT growth3 expected

As of July 1, 2018 Fresenius Helios transferred its German post-acute care business to Fresenius Vamed. To allow for a like-for-like comparison, we also provide sales and EBIT growth rates adjusted for the effects of this transaction.

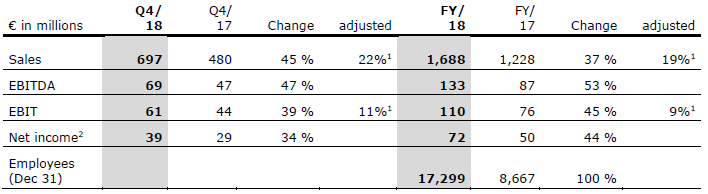

Sales increased by 37% (19%1) to €1,688 million (FY/17: €1,228 million). Organic sales growth was 16% with a strong momentum in both the project and service businesses as well as increased sales from services for Fresenius Helios. Sales of the project business increased by 17% to €712 million (FY/17: €606 million). Sales in the service business grew by 57% (20%1) to €976 million (FY/17: €622 million). In Q4/18, sales increased by 45% (22%1; organic growth: 20%) to €697 million (Q4/17: €480 million).

EBIT increased by 45% (9%1) to €110 million (FY/17: €76 million) with a margin of 6.5% (FY/17: 6.2%). In Q4/18, EBIT increased by 39% (11%1) to €61 million (Q4/17: €44 million) with a margin of 8.8% (Q4/17: 9.2%).

Net income2 increased by 44% to €72 million (FY/17: €50 million). In Q4/18, net income2 increased by 34% to €39 million (FY/17: €29 million).

Order intake increased by 12% to €1,227 million (FY/17: €1,096 million) and reached a new all-time high. As of December 31, 2018, order backlog was €2,420 million (December 31, 2017: €2,147 million).

For FY/19, Fresenius Vamed expects organic sales growth in the range of ~10% and EBIT growth3 of 15% to 20%.

1Without German post-acute care business acquired from Fresenius Helios

2Net income attributable to shareholders of VAMED AG

3Including the German post-acute care business acquired from Fresenius Helios, adjusted for IFRS 16 effects

Conference Call

As part of the publication of the results for fiscal year 2018, a conference call will be held on February 20, 2019 at 2 p.m. CET (8 a.m. EST). All investors are cordially invited to follow the conference call in a live broadcast over the Internet at www.fresenius.com/investors. Following the call, a replay will be available on our website.

This release contains forward-looking statements that are subject to various risks and uncertainties. Future results could differ materially from those described in these forward-looking statements due to certain factors, e.g. changes in business, economic and competitive conditions, regulatory reforms, results of clinical trials, foreign exchange rate fluctuations, uncertainties in litigation or investigative proceedings, and the availability of financing. Fresenius does not undertake any responsibility to update the forward-looking statements in this release.

Current Group expectations for FY 2019

Based on the current status of the Group’s budget process and its FY 2018 guidance, Fresenius expects mid-single digit organic sales growth for FY 2019. Group net income1,2, however, is expected to be broadly stable over FY 2018. Fresenius continues to seek both sales growth and efficiency improvement initiatives in order to enhance these expectations.

Current business segment expectations for FY 20193

For FY 2019, Fresenius Medical Care currently broadly assumes solid comparable4 sales growth and the comparable4 net income to be around the level of FY 2018.

Given its outstanding financial performance in FY 2018, Fresenius Kabi will enter 2019 from a tough comparison basis. In general anticipation of easing drug shortage benefits and meaningful expenses for the further development of its biosimilars portfolio Fresenius Kabi expects mid-single digit organic sales growth and low- to mid-single digit EBIT5 growth in constant currency.

Within Fresenius Helios’ expectation of low- to mid-single digit organic sales growth, Helios Spain continues to grow faster than Helios Germany. Helios Spain’s expected mid-single-digit EBIT growth will not fully offset the headwinds at Helios Germany resulting from regulatory changes and already started countermeasures. Thus, in aggregate, Fresenius Helios currently expects EBIT contraction at a low- to mid-single digit rate.

Fresenius Vamed expects underlying6 growth rates similar to previous years.

Current Group medium-term expectations

Given its current expectations for FY 2018 and FY 2019, Fresenius now believes its ambitious Group targets for 2020 will not be met.

From 2020 onwards, Fresenius now expects sustainable organic Group sales growth in the mid-single digits. Group net income7 is expected to grow organically slightly faster than sales. Upon Fresenius Kabi’s biosimilars business breaking even, Fresenius expects an acceleration of Group earnings growth. Unlike previous mid-term targets, these expectations exclude the effect of small- to medium-sized acquisitions.

In addition to the significant R&D and business development investments in FY 2017 and FY 2018, Fresenius expects record investments in 2019 in both, capex and opex. These investments will further strengthen the basis for sustainable mid-term growth and are testament to Fresenius’ confidence in the dynamic growth opportunities in all of its business segments and end-markets.

Stephan Sturm, CEO of Fresenius, said: “We remain highly confident that Fresenius is on track to continue growing healthily over the medium and long term. Our updated expectations reflect the significant changes made to our portfolio over the last two years. They do not reflect acquisitions, which, however, will remain an important source of growth going forward. Further strengthened by the investments we will make in our businesses next year, Fresenius will be even better positioned for the coming decade.”

Acquisitions

Current expectations include the NxStage acquisition by Fresenius Medical Care and exclude any effects related to Akorn, Inc. While mid-term expectations exclude the effects of small- to medium-sized acquisitions, Fresenius will continue to pursue its strategy of selective acquisitions in order to complement organic growth.

Growing dividend

For FY 2018, Fresenius expects to propose a dividend increase in line with earnings growth8, consistent with its stated dividend policy. The Company intends to further increase its dividend for FY 2019.

Next steps

Fresenius will announce detailed FY 2019 financial guidance and mid-term targets with the release of its FY 2018 results on February 20, 2019.

Conference Call

A conference call will be held on December 7, 2018 at 8 a.m. CET (2 a.m. EDT). All investors are cordially invited to follow the conference call in a live broadcast over the Internet at www.fresenius.com/investors. Following the call, a replay will be available shortly on our website.

# # #

For additional information on the performance indicators used please refer to our website at https://www.fresenius.com/alternative-performance-measures.

# # #

1In constant currency, before special items and effects of IFRS 16, incl. expenses for the further development of the biosimilars business, H1/18 adjusted for divestitures of Care Coordination activities. 2019 including NxStage operating results.

2Net income attributable to shareholders of Fresenius SE & Co. KGaA

3Business segment expectations before effects of IFRS 16

4“comparable” is on a constant currency basis and reflects an adjustment for those effects that are as per FMC’s view not related to FMC’s operating business performance such as, for example, the effects of IFRS 16, sizeable portfolio changes like the divestiture of Sound Inpatient Physicians Holdings or the pending acquisition of NxStage Medical Inc. or other effects of one-time nature like FCPA-related charges or the cost of the 2018 U.S. ballot initiatives. For the preliminary indicative 2019 guidance the “comparable” 2018 basis translates roughly at current currencies for sales in a range of €15,850 – 16,050 million and for net income in a range of €1,350 – 1,365 million. This is subject to fluctuations in the currency rates in the fourth quarter of 2018.

5Before special items, including expenses for the further development of the biosimilars business

6Before transfer of German post-acute care business from Fresenius Helios

7Net income attributable to shareholders of Fresenius SE & Co. KGaA; before special items

8Net income attributable to shareholders of Fresenius SE & Co. KGaA; in constant currency, before special items, incl. expenses for the further development of the biosimilars business, H2/17 adjusted for divestitures of Care Coordination activities

This release contains forward-looking statements that are subject to various risks and uncertainties. Future results could differ materially from those described in these forward-looking statements due to certain factors, e.g. changes in business, economic and competitive conditions, regulatory reforms, results of clinical trials, foreign exchange rate fluctuations, uncertainties in litigation or investigative proceedings, and the availability of financing. Fresenius does not undertake any responsibility to update the forward-looking statements in this release.

- Excellent performance of Fresenius Kabi across all regions and product categories

- Fresenius Medical Care’s sales and earnings growth below the Company’s expectations

- Preparatory initiatives for expected regulatory requirements and decline in admissions impact Helios Germany; Helios Spain with steady yet dynamic growth

- Strong momentum in both Vamed’s project and service businesses

Group guidance for 2018 confirmed and narrowed

As announced on October 16, 2018 Fresenius confirms and narrows its Group guidance1 for FY/18. This is mainly driven by an excellent development of Fresenius Kabi, which partially offset the lower than expected sales and earnings contributions of Fresenius Medical Care and Helios Germany. Group sales are expected to increase at the low end of the original 5% to 8%2 guidance range (in constant currency). Fresenius expects net income1,3,4 growth at the low end of the original 6% to 9% guidance range (in constant currency). Excluding expenditures for the further development of the biosimilars business, net income1,3,5 growth is projected at the low end of the original ~10% to 13% guidance range (in constant currency).

1 2018 before special items (excluding effects related to the Akorn and NxStage transactions, gains from divestitures of Care Coordination activities and increase of FCPA provision)

2 FY/17 base adjusted for IFRS 15 adoption (-€486 million) and divestitures of Care Coordination activities (-€558 million) at Fresenius Medical Care

3 Net income attributable to shareholders of Fresenius SE & Co. KGaA

4 FY/17 base: €1,804 million; FY/18 before special items; including contributions to the campaigns in the U.S. opposing state ballot initiatives at Fresenius Medical Care; including expenditures for further development of the biosimilars business at Fresenius Kabi (€43 million after tax in FY/17 and ~€120 million after tax in FY/18)

5 FY/17 base: €1,847 million; FY/18 before special items; including contributions to the campaigns in the U.S. opposing state ballot initiatives at Fresenius Medical Care; excluding expenditures for further development of the biosimilars business at Fresenius Kabi (€43 million after tax in FY/17 and ~€120 million after tax in FY/18)

If no timeframe is specified, information refers to Q1-3/18

Q3/18:

- Sales: €8.2 billion (+3%1, +4% in constant currency1)

- EBIT2: €1,112 million (+0%, +0% in constant currency)

- EBIT2 (excl. biosimilars business): €1,153 million (+3%, +2% in constant currency)

- Net income2,3: €445 million (+8%, +8% in constant currency)

- Net income2,3 (excl. biosimilars business): €474 million (+13%, +13% in constant currency)

Q1-3/18:

- Sales: €24.7 billion (+1%1, +5% in constant currency1)

- EBIT2: €3,311 million (-5%, -1% in constant currency)

- EBIT2 (excl. biosimilars business): €3,424 million (-3%, +2% in constant currency)

- Net income2,3: €1,367 million (+3%, +7% in constant currency)

- Net income2,3 (excl. biosimilars business): €1,449 million (+8%, +12% in constant currency)

1 Growth rates adjusted for IFRS 15 adoption and divestitures of Care Coordination activities (Q3/17 base: €7,927 million; Q1-3/17 base: €24,551 million)

2 Before special items (before expenses related to the Akorn transaction, gains from divestitures of Care Coordination activities and increase of FCPA provision); growth rates: 2017 base adjusted for divestitures of Care Coordination activities

3 Net income attributable to shareholders of Fresenius SE & Co. KGaA

For a detailed overview of special items please see the reconciliation tables on pages 19-20 in the PDF document.

5% sales growth in constant currency1

Group sales increased by 1%1 (5%1 in constant currency) to €24,695 million (Q1-3/17: €25,191 million). Organic sales growth was 4%. Acquisitions/divestitures contributed net 1% to growth. Negative currency translation effects of 4% were mainly driven by the devaluation of the U.S. dollar and the Chinese yuan against the euro. In Q3/18, Group sales increased by 3%1 (4%1 in constant currency) to €8,192 million (Q3/17: €8,297 million). Organic sales growth was 4%. Acquisitions/divestitures had no net contribution to growth. Currency translation effects reduced sales by 1%.

1 Growth rates adjusted for IFRS 15 adoption and divestitures of Care Coordination activities at Fresenius Medical Care (Q1-3/17 base: €24,551 million; Q3/17 base: €7,927 million)

Group sales by region:

7% net income1,2,3 growth in constant currency

Group EBITDA2 decreased by 4%3 (0%3 in constant currency) to €4,375 million (Q1-3/17: €4,579 million). Group EBIT2 decreased by 5%3 (-1%3 in constant currency) to €3,311 million (Q1-3/17: €3,522 million). The EBIT margin2 was 13.4% (Q1 3/17: 14.0%). Group EBIT2 before expenses for the further development of the biosimilars business decreased by 3%3 (increased 2%3 in constant currency) to €3,424 million. In the prior-year period the compensation for treatments of U.S. war veterans (“VA agreement”) contributed €88 million as a one-time effect. Group EBIT2 excluding the VA agreement and expenses for the further development of the biosimilars business increased by 4% in constant currency.

In Q3/18, Group EBIT3 was broadly stable year-over-year3 (broadly stable3 in constant currency) at €1,112 million (Q3/17: €1,129 million), with an EBIT margin2 of 13.6% (Q3/17: 13.6%). Group EBIT2 excluding the prior-year VA agreement and expenses for the further development of the biosimilars business increased by 2%3 in constant currency.

Group net interest2 was -€436 million (Q1-3/17: -€484 million). The decrease is mainly driven by currency effects as well as refinancing activities and the divestitures of Care Coordination activities.

The decrease of the Group tax rate before special items to 22.0% (Q1-3/17: 28.1%) was mainly due to the U.S. tax reform and some one time effects in Q3 at Fresenius Medical Care and Fresenius Kabi. In Q3/18, the Group tax rate2 was 21.4% (Q3/17: 27.4%).

Noncontrolling interest2 was €876 million (Q1-3/17: €854 million), of which 95% was attributable to the noncontrolling interest in Fresenius Medical Care.

1 Net income attributable to shareholders of Fresenius SE & Co. KGaA

2 Before special items

3 Base 2017 base adjusted for divestitures of Care Coordination activities

For a detailed overview of special items please see the reconciliation tables on pages 19-20 in the PDF document.

Group net income1,2 increased by 3%3 (7%3 in constant currency) to €1,367 million (Q1 3/17: €1,329 million). Earnings per share1,2 increased by 3%3 (7%3 in constant currency) to €2.46 (Q1-3/17: €2.40). In Q3/18, Group net income1,2 increased by 8%3 (8%3 in constant currency) to €445 million (Q3/17: €413 million). Earnings per share1,2 increased by 7%3 (7%3 in constant currency) to €0.80 (Q3/17: €0.75).

Group net income1,2,4 before expenses for the further development of the biosimilars business increased by 8%3 (12%3 in constant currency) to €1,449 million (Q1-3/17: €1,339 million). Earnings per share1,2,4 increased by 8%3 (12%3 in constant currency) to €2.61 (Q1-3/17: €2.42). In Q3/18, Group net income1,2,4 increased by 13%3 (13%3 in constant currency) to €474 million (Q3/17: €423 million). Earnings per share1,2,4 increased by 12%3 (12%3 in constant currency) to €0.85 (Q3/17: €0.77).

Group net income2,5 after special items increased by 16% (by 21% in constant currency) to €1,511 million (Q1-3/17: €1,303 million), mainly due to gains related to divestitures in Care Cordination activities at Fresenius Medical Care. Earnings per share2,5 increased by 16% (21% in constant currency) to €2.72 (Q1-3/17: €2.35). In Q3/18, Group net income2,5 increased by 6% (4% in constant currency) to €419 million (Q3/17: €396 million). Earnings per share2,5 increased by 6% (4% in constant currency) to €0.75 (Q3/17: €0.71).

1 Before special items

2 Net income attributable to shareholders of Fresenius SE & Co. KGaA

3 2017 base adjusted for divestitures of Care Coordination activities

4 Before expenses for the further development of the biosimilars business

5 After special items

For a detailed overview of special items please see the reconciliation tables on pages 19-20 in the PDF document.

Continued investment in growth

Spending on property, plant and equipment was €1,370 million (Q1-3/17: €1,137 million), primarily for the modernization and expansion of dialysis clinics, production facilities as well as hospitals and day clinics. This corresponds to 5.5% of sales.

Total acquisition spending was €876 million (Q1-3/17: €6,662 million). The prior-year period included the acquisition of Quirónsalud.

Cash flow development

Group operating cash flow decreased by 15% to €2,405 million (Q1-3/17: €2,821 million) with a margin of 9.7% (Q1-3/2017: 11.2%). The decrease is mainly due to two effects at Fresenius Medical Care in North America: Receipt of a ~€200 million payment under the VA agreement in the prior-year period as well as increased accounts receivable related to the addition of calcimimetics into the Medicare ESRD payment bundle. In addition, negative currency translation effects weighed on the cash flow development in Q1-3/18. Operating cash flow in Q3/18 increased by 1% to €1,149 million (Q3/17: €1,138 million), with a margin of 14.0% (Q3/17: 13.7%).

Given the effects described above and growing investments, free cash flow before acquisitions and dividends decreased to €1,049 million (Q1-3/17: €1,705 million). Free cash flow after acquisitions and dividends was €1,172 million (Q1-3/17: -€5,233 million).

Solid balance sheet structure

The Group’s total assets increased by 5% (4% in constant currency) to €55,723 million (Dec. 31, 2017: €53,133 million). Current assets grew by 16% (16% in constant currency) to €14,593 million (Dec. 31, 2017: €12,604 million). Non-current assets increased by 1% (broadly stable in constant currency) to €41,130 million (Dec. 31, 2017: € 40,529 million).

Total shareholders’ equity increased by 10% (9% in constant currency) to €23,998 million (Dec. 31, 2017: €21,720 million). The equity ratio increased to 43.1% (Dec. 31, 2017: 40.9%).

Group debt was broadly stable unchanged (decreased by 1% in constant currency) at €18,961 million (Dec. 31, 2017: € 19,042 million). Group net debt decreased by 5% (-6% in constant currency) to € 16,505 million (Dec. 31, 2017: € 17,406 million) mainly due to the proceeds from divestitures of Care Coordination activities.

As of September 30, 2018, the net debt/EBITDA ratio was 2.751,2 (December 31, 2017: 2.841,2). Excluding the proceeds from divestitures of Care Coordination activities the net debt/EBITDA ratio was 2.961,2. At year-end 2018, Fresenius now expects the FY/18 net debt/EBITDA1,2 ratio to be on a comparable level to year-end 2017.

1 At LTM average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures, excluding Akorn and NxStage transactions

2 Before special items

Business Segments

Fresenius Medical Care

Fresenius Medical Care is the world's largest provider of products and services for individuals with renal diseases. As of September 30, 2018, Fresenius Medical Care was treating 329,085 patients in 3,872 dialysis clinics. Along with its core business, the company provides related medical services in the field of Care Coordination.

- 3% comparable1 sales growth in constant currency in Q3

- -2% adjusted4,6 net income decrease in constant currency in Q3

- Outlook for FY/18 adjusted

Sales decreased by 8% (-2% in constant currency) to €12,247 million (Q1-3/17: €13,355 million). Organic sales growth was 3%. Currency translation effects reduced sales by 7%. The adoption of IFRS 15 reduced sales by 3%. Q1-3/17 base additionally adjusted for divestitures of Care Coordination activities, sales decreased by 4% (increased by 3% in constant currency).

1 Adjusted for IFRS 15 implementation; base adjusted for divested Care Coordination activities

2 Excluding VA agreement Q3: 3%; Q1-3: 4%

3 Excluding gains from divestitures of Care Coordination activities, increase of FCPA provision, ballot initiatives, divested Care Coordination activities in Q3/2017; including Natural disaster costs and VA agreement

4 Net income attributable to shareholders of Fresenius Medical Care AG & Co. KGaA

5 Consistent with guidance, i.e. excluding gains from divestitures of Care Coordination activities, increase of FCPA provision, ballot initiatives, , divested Care Coordination activities; including Natural disaster costs, the effect of the U.S. Tax Reform and including VA agreement

6 Consistent with guidance, i.e. excluding gains from divestitures of Care Coordination activities, the effect of the U.S. Tax Reform, VA agreement, FCPA provision, ballot initiatives, divested Care Coordination activities, Natural disaster costs

In Q3/18, sales decreased by 6% (-6% in constant currency) to €4,058 million (Q3/17: €4,336 million). Organic sales growth was 3%. The adoption of IFRS 15 reduced sales by 3%. Q3/17 base additionally adjusted for divestitures of Care Coordination activities, sales in Q3/18 increased by 2% (increased by 3% in constant currency).

Health Care services sales (dialysis services and care coordination) decreased by 4%1 (increased by 3%1 in constant currency) to €9,852 million (Q1-3/17: €10,950 million). With €2,395 million (Q1-3/17: €2,405 million), Health Care product sales were on prior-year’s level (increased by 5% in constant currency).

In North America, sales decreased by 5%1 (increased by 1%1 in constant currency) to €8,589 million (Q1-3/17: €9,715 million). Health Care services sales decreased by 6%1 (increased by 1%1 in constant currency) to €7,978 million (Q1-3/17: €9,086 million). Excluding the 2017 effect from the VA Agreement (€96 million), Health Care services sales increased by 2%1 in constant currency. Health Care product sales decreased by 3% (increased by 4% in constant currency) to €610 million (Q1-3/17: €629 million).

Sales outside North America increased by 1% (7% in constant currency) to €3,648 million (Q1-3/17: €3,628 million).

Health Care services sales increased by 1% (9% in constant currency) to €1,873 million (Q1-3/17: €1,864 million). Health Care product sales increased by 1% (5% in constant currency) to €1,774 million (Q1-3/17: €1,764 million).

Fresenius Medical Care’s EBIT increased by 32% (39% in constant currency) to €2,425 million (Q1-3/17: €1,843 million), driven by the divestitures of Care Coordination activities. The EBIT margin increased to 19.8% (Q1-3/17: 13.8%). EBIT on a comparable basis decreased by 2% in constant currency and EBIT margin was 13.9% (Q1-3/17: 14.3%).

In Q3/18, EBIT decreased by 13% (-20% in constant currency) to €527 million (Q3/17: €609 million). The EBIT margin decreased to 13.0% (Q3/17: 14.0%). EBIT on a comparable basis increased by 5% (increased by 4% in constant currency) and EBIT margin increased to 15.1% (Q3/17: 14.8%).

1 Growth rate adjusted for IFRS 15 implementation and divested Care Coordination activities

Net income1 increased by 76% (86% in constant currency) to €1,557 million (Q1-3/17: €886 million). Adjusted net income1 growth was 4% in constant currency. Net income1 growth on a comparable basis was 16% in constant currency.

In Q3/18, net income1 decreased by 8% (-17% in constant currency) to €285 million (Q3/17: €309 million). Adjusted net income1 growth was -2% in constant currency. Net income1 growth on a comparable basis was 19% in constant currency.

Operating cash flow was €1,220 million (Q1-3/17: €1,664 million). The cash flow margin was 10.0% (Q1-3/17: 12.5%). The decrease is mainly due to two effects in North America: Receipt of a ~€200 million payment under the VA agreement in the prior-year period as well as increased accounts receivable related to the addition of calcimimetics into the Medicare ESRD payment bundle. In Q3/18, operating cash flow was €609 million (Q3/17: €612 million), mainly driven by higher tax payments and discretionary contributions to pension plan assets in the U.S., almost fully offset by decreases in accounts receivable. The cash flow margin was 15.0% (Q3/17: 14.1%).

Fresenius Medical Care revised its outlook for FY/18 as the business development in Q3/18 was below the company’s expectations. Fresenius Medical Care now expects sales growth of 2% to 3%2 in constant currency (previously: 5% to 7%2). On a comparable basis3, Fresenius Medical Care now expects FY/18 net income1 to increase by 11% to 12%3 in constant currency (previously: 13% to 15%3). On an adjusted basis4, Fresenius Medical Care now expects FY/18 net income1 to increase by 2% to 3%4 in constant currency (previously: 7% to 9%4).

For further information, please see Fresenius Medical Care’s Investor News at www.freseniusmedicalcare.com.

1 Net income attributable to shareholders of Fresenius Medical Care AG & Co. KGaA

2 2017 base: €16,739 million (adjusted for IFRS 15 adoption (-€486 million) and divestitures of Care Coordination activities (-€558 million))

3 2017 base: €1,242 million, excluding H2/17 net income of divestited Care Coordination activities (-€38 million); 2018 including benefits of the U.S. tax reform but excluding gains from divestitures of Care Coordination activities, contributions to the campaigns in the U.S. opposing state ballot initiatives at Fresenius Medical Care and FCPA provision

4 2017 base: €1,162 million, excluding H2/17 net income of divested Care Coordination activities (-€38 million), the effect of the U.S. tax reform, natural disaster costs, FCPA provision and effects of the agreement with the U.S. Departments of Veterans Affairs and Justice (VA agreement); 2018 excluding benefits of the U.S. tax reform, gains from divestitures of Care Coordination activities, contributions to the campaigns in the U.S. opposing state ballot initiatives and FCPA provision

Fresenius Kabi

Fresenius Kabi offers intravenously administered generic drugs, clinical nutrition and infusion therapies for seriously and chronically ill patients in the hospital and outpatient environments. The company is also a leading supplier of medical devices and transfusion technology products. In the biosimilars business, we are developing products with a focus on oncology and autoimmune diseases.

- 8% organic sales growth and 14% EBIT1 growth in constant currency (excl. biosimilars expenses) in Q3

- Sales outlook confirmed and strengthened: top end of 4% to 7% organic sales growth expected

- EBIT outlook raised: 1% to 3%5 EBIT growth in constant currency expected (~9% to 11%6 excl. biosimilars expenses)

Sales increased by 2% (increased by 7% in constant currency) to €4,857 million (Q1-3/17: €4,764 million). Organic sales growth was 7%. Strong negative currency translation effects (-5%) were mainly related to the devaluation of the U.S. dollar, the Brazilian real and the Argentinian peso against the euro. In Q3/18, sales increased by 6% (8% in constant currency) to €1,650 million (Q3/17: €1,562 million). Organic sales growth was 8%.

Sales in Europe grew by 1% (organic growth: 3%) to €1,658 million (Q1-3/17: €1,635 million). In Q3/18, sales were unchanged (organic growth: 1%) at €538 million.

1 Before special items

2 Before expenses for the further development of the biosimilars business: Q3/18: 14%; Q1-3/18: 11%

3 Net income attributable to shareholders of Fresenius SE & Co. KGaA

4 Before expenses for the further development of the biosimilars business: Q3/18: 31%; Q1-3/18: 22%

5 FY/17 base: €1,177 million; before special items, including expenditures for the further development of the biosimilars business (€60 million in FY/17 and ~€160 million in FY/18)

6 FY/17 base: €1,237 million; before special items, excluding expenditures for the further development of the biosimilars business (€60 million in FY/17 and ~€160 million in FY/18)

For a detailed overview of special items please see the reconciliation tables on page 19 - 20 in the PDF document.

Sales in North America increased by 1% (organic growth: 8%) to €1,760 million (Q1-3/17: €1,736 million). In Q3/18, sales increased by 13% (organic growth: 12%) to €620 million (Q3/17: €549 million).

Sales in Asia-Pacific increased by 8% (organic growth: 12%) to €964 million (Q1-3/17: €894 million). In Q3/18, sales increased by 8% (organic growth: 9%) to €337 million (Q3/17: €312 million). Sales in Latin America/Africa decreased by 5% (organic growth: 11%) to €475 million (Q1-3/17: €499 million). In Q3/18, sales decreased by 5% (organic growth increased by 13%) to €155 million (Q3/17: €163 million).

EBIT1 decreased by 6% (increased by 1% in constant currency) to €854 million (Q1-3/17: €905 million) with an EBIT margin1 of 17.6% (Q1-3/17: 19.0%). In Q3/18, EBIT1 increased by 5% (5% in constant currency) to €297 million (Q3/17: €283 million) with an EBIT margin1 of 18.0% (Q3/17: 18.1%).

EBIT1 before expenses for the further development of the biosimilars business increased by 5% (11% in constant currency) to €967 million (Q1-3/17: €919 million) with an EBIT margin1 of 19.9% (Q1-3/17: 19.3%). In Q3/18, EBIT1 before expenses for the further development of the biosimilars business increased by 14% (14% in constant currency) to €338 million (Q3/17: €297 million) with an EBIT margin1 of 20.5% (Q3/17: 19.0%).

Net income1,2 increased by 2% (9% in constant currency) to €554 million (Q1-3/17: €544 million). In Q3/18, net income1,2 increased by 21% (21% in constant currency) to €199 million (Q3/17: €165 million).

Operating cash flow increased by 28% to €820 million (Q1-3/17: €640 million). The cash flow margin grew to 16.9% (Q1-3/17: 13.4%). In Q3/18, operating cash flow increased by 49% to €366 million (Q3/17: €245 million) with a cash flow margin of 22.2% (Q3/2017: 15.7%) mainly driven by a strong operational performance and working capital improvements.

1 Before special items

2 Net income attributable to shareholders of Fresenius SE & Co. KGaA

For a detailed overview of special items please see the reconciliation tables on page 19 - 20 of the PDF document.

Based on the strong development in Q3/18 Fresenius Kabi confirms and strengthens its organic sales growth guidance of 4% to 7% and now expects to reach the top end of this range.