Today, Fresenius published its 2025 Annual Report. As announced in late February 2026, 2025 marked another strong year of performance and the launch of the current phase of the #FutureFresenius strategy: Rejuvenate. Despite headwinds, the healthcare group achieved its outlook, which was raised twice during the year. Group revenue before special items rose to €22.6 billion, with organic growth of 7%, while constant currency Core EPS (excluding FMC) increased by 12%.

“Over the past three years, we have successfully implemented our #FutureFresenius strategy and created a new Fresenius that is innovative, relevant, resilient, and adaptable. At the same time, we have significantly bolstered our company’s economic strength. We aim to build on this strong foundation,” said Michael Sen, Chairman of the Management Board of Fresenius.

The 2025 Annual Report demonstrates how Fresenius is creating sustainable value for all stakeholders by executing its #FutureFresenius strategy. It includes the Sustainability Statement in accordance with the European Sustainability Reporting Standards (ESRS), and is available as a PDF and as an interactive online version in German and English. The online report features additional business stories and includes a video statement from CEO Michael Sen.

FY/25 – Strong organic revenue and excellent Core EPS growth; REJUVENATE phase spurs profitable growth, drives stronger balance sheet, and creates significant value.

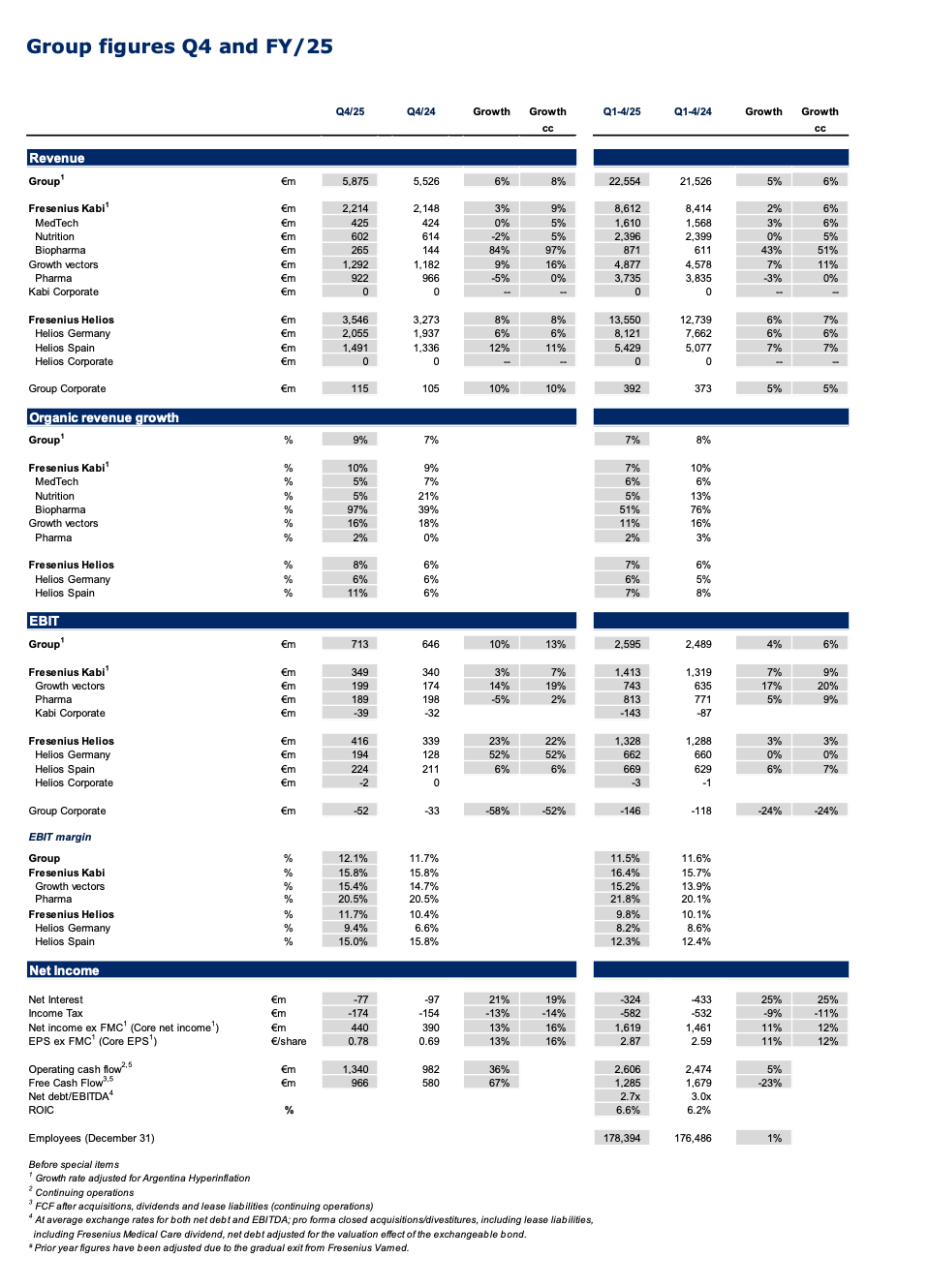

- Group revenue1 at €22,554 million with organic growth of 7%1,2 reflecting the consistent execution across Fresenius Kabi and Fresenius Helios.

- Group EBIT1 at €2,595 million with 6%3 growth in constant currency driven in particular by Fresenius Kabi’s Growth Vectors and the strong performance of Fresenius Helios in Spain; Group EBIT margin1 at 11.5% despite significant headwinds.

- Core EPS1,4 increased by 12%3 in constant currency to €2.87 based on strong operating results and significantly decreased interest expense.

- Structural EBIT margin ambition increased for Fresenius Kabi to 17 to 19% (previously 16 to 18%)

- Constant currency Core EPS growth1,4 established as new guidance metric is expected to be in the range of 5 to 10% in FY/26; organic revenue growth2 projected to be in the range of 4 to 7% in FY/26.

- Net debt/EBITDA ratio improved by 30 bp to 2.7x1,5, well within the self- imposed target corridor of 2.5 to 3.0x; driven by cash flow delivery leading to significant debt reduction.

- Dividend proposal of €1.05 per share; year-on-year increase of 5%, in line with the Company's dividend payout ratio of 30 to 40%.

Q4/25 – Closing the year with an outstanding quarter; excellent organic revenue and EBIT growth; excellent operating cashflow.

- Group revenue1 at €5,875 million with organic growth of 9%1,2 driven by contributions from both, Fresenius Kabi and Fresenius Helios.

- Group EBIT1 at €713 million with constant currency growth of 13%3 on the back of the continued powerful operating performance at Fresenius Kabi and the expected strong acceleration at Fresenius Helios; Group EBIT margin1 improved by 40 bp to 12.1%.

- Core EPS1,4 growth in constant currency of 16%3 further accelerated to €0.78, driven by consistent operating strength and lower interest expenses.

- Operating cashflow of €1,340 million, a year-on-year increase of 36% driven by disciplined capex spending and focus on net working capital at Fresenius Kabi, and Fresenius Helios successfully driving receivables collection.

Michael Sen, CEO of Fresenius: "2025 was a pivotal year for Fresenius. With disciplined execution of our #FutureFresenius strategy and a strong performance from Team Fresenius, we met our upgraded full-year guidance by delivering another quarter of competitive growth, increasing organic revenue by 9%, EBIT by 13% and Core EPS by 16% at constant currency. 2025 capped a year of continued momentum across the Company: We further strengthened the balance sheet, and upgraded our guidance, while preparing the business through targeted investment for the next phase of growth. All of this leads to a proposed dividend of €1.05 per share, underscoring our commitment to creating shareholder value. With #FutureFresenius we have transformed our Company, positioning ourselves to deliver future success in a new world order. Looking ahead, we enter 2026 with strong foundations and clear priorities. We are confident in our ability to deliver profitable, sustainable growth with the guidance of organic revenue growth of 4% to 7% and constant currency Core EPS growth of 5% to 10%, while continuing to create long term value across the healthcare ecosystem for patients, customers, partners, and shareholders."

Guidance for Fiscal Year 20261

Fresenius Group6: organic revenue growth2 in the range of 4% to 7%; constant currency Core EPS1,4 growth expected in the range of 5% to 10%; EBIT margin9 of ~11.5%.

Fresenius Kabi7: organic revenue growth3 in the mid- to high-single-digit percentage range; EBIT margin1 of 16.5% to 17.0%.

Structural EBIT margin1 ambition raised to 17% to 19% (previously 16% to 18%) following Kabi’s rigorous strategy execution leading to consistent margin expansion over the past several years.

Fresenius Helios8: organic revenue growth in the mid-single-digit percentage range; EBIT margin of 10.0% to 10.5%.

Assumptions to guidance: The company acknowledges that the prevailing trends of fast- moving macroeconomic and geopolitical environment continue, resulting in increased volatility and a higher level of operational uncertainty. The guidance does not take into account potential extreme scenarios that could affect the company, its peers, and the healthcare sector as a whole. Potential implications of the United States Supreme Court ruling as of February 20, 2026, are currently being evaluated but cannot be fully assessed at this stage and are hence not reflected in the FY/26 guidance.

Dividend proposal of €1.05 per share reflects capital allocation priorities

Fresenius remains fully commitment to delivering attractive shareholder returns. For fiscal year 2025, the Company will propose a dividend of €1.05 per share. This corresponds to a payout ratio of 37%, at the upper half of the 30% to 40% range of core net income1,4 , as specified in the Fresenius Financial Framework.

Fresenius Group – Business development FY and Q4/2025

FY/25: Strong performance despite significant macroeconomic headwinds; twice upgraded guidance delivered.

Organic revenue1 grew 7%2 reaching the top-end of the 5% to 7% guide while the 6%3 constant currency Group EBIT growth before special items secured the midpoint of the guided range of 4% to 8%. The Company achieved this despite significant headwinds including the impact from the absence of energy relief funding at Fresenius Helios, the Volume Based Procurement (VBP) of the nutrition product Ketosteril in China at Fresenius Kabi, as well as FX effects and U.S. tariffs.

Q4/25: Closing the year with an outstanding quarter which led to an increase of Group organic revenue1 growth of 9%2 and revenues reaching €5,875 million.

Group EBIT before special items amounted to €713 million, a significant acceleration with an increase of 13%3 in constant currency fuelled by Fresenius Kabi’s continued powerful operating performance and the expected strong development at Fresenius Helios. The strong acceleration at Helios is due to the very strong top-line development and was supported by strong execution on the Performance Program in Q4/25 as well as the positive effects from the surcharge on invoices of publicly insured patients recognized under other operating income. At Kabi, the operating leverage and additional productivity gains more than compensated the impact from the VBP of the nutrition product Ketosteril in China, and some targeted investments.

Group EBIT margin1 improved by 40 bp to 12.1%.

Group Core net income1,4 increased by 16%3 in constant currency to €440 million strongly outpacing revenue growth. The good operating performance of both, Fresenius Kabi and Fresenius Helios, further productivity gains as well as the decreased year-over-year interest expenses drove this performance.

Group Core earnings per share1,4 rose by 16%3 in constant currency to €0.78.

Operating Companies – Business development FY and Q4/25

Fresenius Kabi

FY/25: Consistent financial performance delivered over the course of the year with excellent organic revenue growth of 7% at the top-end of the structural growth band and an EBIT margin expansion of 70 bps to 16.4%.

Q4/25: Strong finish to the year with organic growth well above the structural growth band of 4% to 7%; Growth Vectors driving the performance headed by continued Biopharma strength; EBIT margin reflects targeted investments, and year-end effects.

Organic revenue growth of 10%2 in Q4 driven by the Growth Vectors and led by Biopharma with strong product roll-outs; revenue rose to €2,214 million, making it the highest quarterly revenue amount in Fresenius Kabi’s history; growth as reported was significantly impacted by currency translation effects, primarily from the US Dollar and the Argentinian Peso.

- Growth Vectors with 16% organic revenue2 growth; Biopharma 97%, MedTech 5%, and Nutrition 5%

- Biopharma revenue: €265 million, mainly driven by the tocilizumab biosimilar Tyenne ramp up in Europe and the U.S.; uptake of Otulfi with first sales from the exclusive distribution agreement with CivicaScript in the U.S.

- MedTech revenue: €425 million with broad-based growth across all regions and segments, Transfusion & Cell Therapy (TCT) and Infusion and Nutrition Systems (INS) both showed solid growth.

- Nutrition revenue: €602 million driven by strong underlying growth in Europe and Latin America; more than offset the impact from the VBP tender on nutrition product Ketosteril in China.

- Pharma revenue: €922 million, organic revenue increased by 2%2 driven by Europe, with good volumes and price mix; U.S. volume growth more than compensated for pricing pressures.

- EBIT1 of Fresenius Kabi increased to €349 million or 7%3 at constant currency. The performance reflected the operating leverage and the benefit of productivity gains that more than offset the impact of the Ketosteril tender in China and the adverse impact from U.S. tariffs, particularly in MedTech. The performance in the quarter also reflected targeted investments. The EBIT margin1 was 15.8%.

- EBIT1 of the Growth Vectors increased by 19%3 in constant currency and amounted to €199 million; EBIT margin1 improved by 70 bps to 15.4%, making further progress toward Kabi’s structural margin band target.

- EBIT1 of Pharma increased 2%3 in constant currency to €189 million driven by Europe and the U.S. as well as by ongoing cost efficiencies. EBIT margin1 at 20.5%.

Fresenius Helios

FY/25: Fresenius Helios delivered organic revenue growth of 7% driven by solid activity growth and favourable pricing in Germany and Spain; EBIT margin1 of 9.8% consistent with the target for FY/25.

Q4/25: Fresenius Helios with very strong organic revenue growth and outstanding year-on-year margin improvement.

8% organic revenue growth in Q4 mainly driven by year-over-year activity levels increase at both, Helios Germany and Helios Spain, and positive pricing; revenue increased by 8% in constant currency to €3,546 million.

- Helios Germany’s organic revenue growth at 6%, reflecting good admission growth and positive pricing; revenues at €2,055 million.

- Helios Spain with organic revenue growth of 11% to €1,491 million driven by strong activity levels and end-of-year payor settlements.

- EBIT1 of Fresenius Helios at €416 million with 22% growth at constant currency. The acceleration at Helios reflects the very strong top-line development and was fuelled by the significant ramp up of the Performance Program in Q4/25 and the positive effects from the surcharge on invoices of publicly insured patient in Germany recognized under other operating income.

EBIT margin1 of Fresenius Helios improved by 130 bp to 11.7%. - EBIT1 of Helios Germany increased by 52% to €194 million reflecting the significant ramp up of the Performance Program in Q4/25 and the positive effects from the surcharge on invoices of publicly insured patient in Germany;

EBIT margin1 improved by 280 bp to 9.4% compared to Q4/2024. - EBIT1 of Helios Spain increased by 6% in constant currency to €224 million; EBIT margin1 at 15.0% reflects some year-end effects as well as the good topline development.

- Helios Performance Programme delivering substantial cost savings in Q4/25 adding up to the expected roughly €100 million contributions in FY/25.

1 Before special items

2 Organic growth rate adjusted for accounting effects related to Argentina hyperinflation

3 Growth rate adjusted for Argentina hyperinflation

4 Excluding Fresenius Medical Care

5 At average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures, including lease liabilities, including Fresenius Medical Care dividend, net debt adjusted for the valuation effect of the exchangeable bond

6 2025 base: €22,554 million (revenue), €2.87 (Core EPS1,4)

7 2025 base: €8,612 million (revenue) and €1,413 million (EBIT)

8 2025 base: €13,550 million (revenue) and €1,328 million (EBIT)

9 This metric (EBIT margin) is provided solely for modelling purposes and does not form part of the official guidance; 2025 Base: €2,595 million

Conference call and Audio webcast

As part of the publication of the Q4 and FY 2025 results, a conference call will be held on February 25, 2026 at 1:30 p.m. CET / 7:30 a.m. EST. All investors are cordially invited to follow the conference call in a live audio webcast at https://www.fresenius.com/investors. Following the call, a replay will be available on our website.

Contact for shareholders

Investor Relations phone: + 49 6172 608-24 87

e-mail: ir-fre@fresenius.com

Note on the presentation of financial figures

- If no timeframe is specified, information refers to Q4/2025.

- Consolidated results for Q4 and FY 2025 as well as for Q4 and FY 2024 include special items. An overview of the results for Q4 and FY 2025 - before and after special items – is available on our website.

- Growth rates in constant currency of Fresenius Kabi are adjusted. Adjustments relate to the hyperinflation in Argentina. Accordingly, constant currency growth rates of the Fresenius Group are also adjusted.

- Information on the performance indicators is available on our website at https://www.fresenius.com/alternative-performance-measures.

This release contains forward-looking statements that are subject to various risks and uncertainties. Future results could differ materially from those described in these forward-looking statements due to certain factors, e.g. changes in business, economic and competitive conditions, regulatory reforms, results of clinical trials, foreign exchange rate fluctuations, uncertainties in litigation or investigative proceedings, the availability of financing and unforeseen impacts of international conflicts. Fresenius does not undertake any responsibility to update the forward-looking statements in this release.

Fresenius SE & Co. KGaA Registered Office: Bad Homburg, Germany / Commercial Register: Amtsgericht Bad Homburg, HRB 11852 Chairman of the Supervisory Board: Wolfgang Kirsch

General Partner: Fresenius Management SE Registered Office: Bad Homburg, Germany / Commercial Register: Amtsgericht Bad Homburg, HRB 11673 Management Board: Michael Sen (Chairman), Pierluigi Antonelli, Sara Hennicken, Robert Möller, Dr. Michael Moser Chairman of the Supervisory Board: Wolfgang Kirsch

Q3/2025: Strong organic revenue and excellent EPS growth; EBIT growth guidance raised

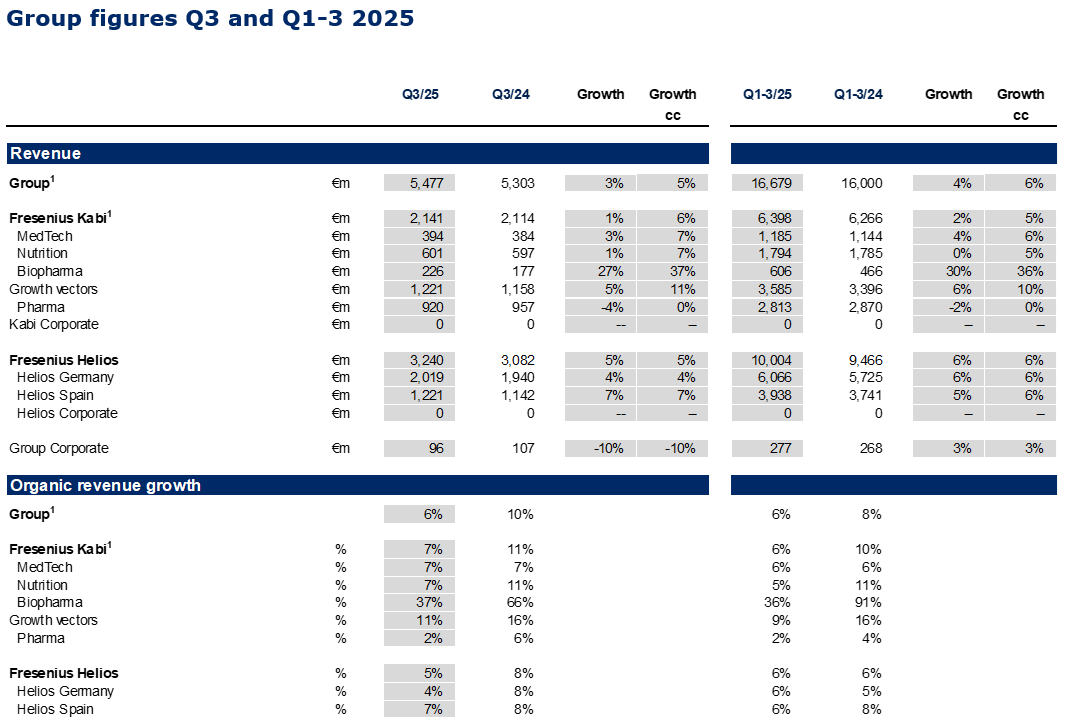

- Group revenue1 at €5,477 million with organic growth of 6%1,2 driven by consistent delivery across Fresenius Kabi and Fresenius Helios.

- Group EBIT1 at €574 million with 6%3 growth in constant currency; growth accelerated from Q2/2025 driven by the strong operating performance at Fresenius Kabi, and a solid development at Fresenius Helios despite usual seasonality in Spain and the high prior-year base due to energy relief payments in Germany; Group EBIT margin1 improved to 10.5%.

- Core EPS1,4 increased by excellent 14%3 in constant currency to €0.62 based on strong operating results and significantly decreased interest expense.

- Net debt/EBITDA ratio at 3.0x1,5 within the self-imposed target corridor driven by strong cash flow delivery.

1 Before special items

2 Organic growth rate adjusted for accounting effects related to Argentina hyperinflation

3 Growth rate adjusted for Argentina hyperinflation

4 Excluding Fresenius Medical Care

5 At average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures, including lease liabilities, including Fresenius Medical Care dividend, net debt adjusted for the valuation effect of the equity-neutral exchangeable bond

Michael Sen, CEO of Fresenius: "Fresenius is accelerating with purpose, and our transformation is delivering tangible results. Our disciplined execution and performance-oriented culture have resulted in 14% growth in Core EPS, a 6% increase in organic revenue growth, and margin improvements, enabling us to raise our full-year EBIT guidance to 4%-8%. Fresenius Kabi and Fresenius Helios continue to perform well, while investments in digital health and advanced therapies are reshaping patient care. Despite the current macroeconomic environment, we continue to perform and meet our commitments. With Rejuvenate now driving measurable progress and a clear focus on patient care, we are creating sustainable value for patients, partners, and shareholders – today and into the future."

Guidance raised for Fiscal Year 20251

Based on the strong earnings growth in Q1-3/2025, Fresenius raised the Group EBIT growth guidance:

Fresenius Group2 : organic revenue growth3 in the range of 5 to 7%; constant currency EBIT growth4 now expected in the range of 4% to 8% (previous: 3 to 7%)

Fresenius Kabi5 : organic revenue growth3 in the mid- to high-single-digit percentage range; EBIT margin of 16.0% to 16.5%

Fresenius Helios6 : organic revenue growth in the mid-single-digit percentage range; EBIT margin around 10%

The strong performance in Q1-3/2025 gives the scope to deliberately take some investments in Q4/2025, for example in R&D. This is in line with Fresenius’ strategic roadmap for the Rejuvenate phase to upgrade core and scale platforms and with a view on future performance, i.e. investing in further long-term profitable growth.

1 Before special items

2 2024 base: €21,526 million (revenue) and €2,489 million (EBIT)

3 Organic growth rate adjusted for accounting effects related to Argentina hyperinflation

4 Growth rate adjusted for Argentina hyperinflation

5 2024 base: €8,414 million (revenue) and €1,319 million (EBIT)

6 2024 base: €12,739 million (revenue) and €1,288 million (EBIT)

Assumptions to guidance: When Fresenius gave guidance in February 2025, the company acknowledged the fast-moving macro-economic and geopolitical environment, resulting in a higher level of operational uncertainty. Fresenius’ guidance continues to reflect current factors and known uncertainties such as impacts from tariffs to the extend they can currently be assessed. The guidance does not take into account potential extreme scenarios that could affect the company, its peers, and the healthcare sector as a whole.

Fresenius Group – Business development Q3/2025

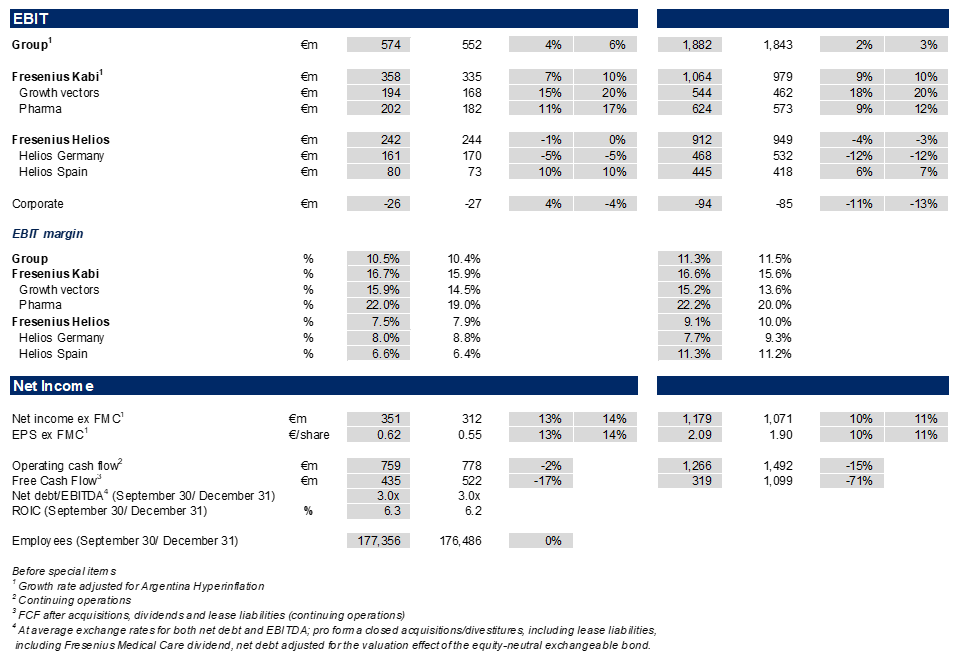

In Q3/2025, the strong operating performance at Fresenius Kabi, and solid development at Fresenius Helios led to consistent Group organic revenue1 growth of 6%2 with revenues reaching €5,477 million.

Group EBIT before special items amounted to €574 million, a sequential acceleration with an increase of 6%3 in constant currency despite the absence of energy relief payments at Helios Germany, the usual seasonality at the Spanish hospital business in the third quarter, and the impact of the Volume Based Procurement of the nutrition product Ketosteril in China at Fresenius Kabi. Group EBIT margin1 improved to 10.5% (Q3/24: 10.4%). The Helios Performance Programme is advancing with material contributions expected in Q4/2025 with likely some spill-over into 2026. The strong Q3/2025 EBIT development was additionally supported by positive phasing effects.

Group net income1,4 increased by excellent 14%3 in constant currency to €351 million strongly outpacing revenue growth. The good operating performance of the core businesses, further productivity gains at Fresenius Kabi and strict cost discipline at Fresenius Helios drove this strong performance, and was supported by the significantly decreased year-over-year interest expenses. In the third quarter alone, interest expenses decreased by €35 million.

Core Earnings per share1,4 rose by excellent 14%3 in constant currency to €0.62.

1 Before special items

2 Organic growth rate adjusted for accounting effects related to Argentina hyperinflation

3 Growth rate adjusted for Argentina hyperinflation

4 Excluding Fresenius Medical Care

Operating Companies – Business development Q3/2025

Fresenius Kabi showed strong organic growth at the upper end of the structural growth range with Growth Vectors driving the performance, headed by continued Biopharma strength; EBIT margin above the 2025 guidance range supported by productivity gains and some contributions realized earlier than originally expected.

Organic revenue growth of 7%1 driven by the Growth Vectors, also benefitting from some inflation related pricing effects in Argentina; disciplined execution on product rollouts led to contributions already realized in Q3/2025 that were originally expected for Q4; revenue increased to €2,141 million; growth as reported was negatively impacted by currency effects; increase in constant currency of 6%2.

- Growth Vectors with excellent organic revenue1 growth of 11%: MedTech 7%, Nutrition 7%, Biopharma 37%.

- Nutrition revenue: €601 million driven by strong growth in all regions except China; Latin America and Europe contributing nicely; continued strong market demand in the U.S. for lipid emulsions; China declined albeit slightly less than anticipated with respect to the Volume Based Procurement (VBP) tender impact on nutrition product Ketosteril.

- Biopharma revenue: €226 million with growth mainly driven by the tocilizumab biosimilar Tyenne ramp up in Europe and the U.S.; first delivery of Tyenne vials for the EU market from fully vertically integrated supply chain; exclusive distribution contract for ustekinumab biosimilar Otulfi with CivicaScript in the U.S., first sales expected in Q4/2025.

- MedTech revenue: €394 million with broad-based growth across all regions, Transfusion & Cell Therapy (TCT) and Infusion and Nutrition Systems (INS) both showed solid growth.

- Pharma revenue: €920 million, organic revenue at solid 2%1 growth relative to a strong prior-year base; good volume demand and disciplined pricing in Europe, as well as continued growth in I.V. solutions in the U.S.

1 Organic growth rate adjusted for accounting effects related to Argentina hyperinflation

2 Growth rate adjusted for Argentina hyperinflation

- EBIT1 of Fresenius Kabi with 10%2 constant currency increase to €358 million driven by operating leverage and productivity gains; despite the effects of the tender for Ketosteril in China, EBIT margin1 increased to 16.7% mainly driven by the significant margin expansion of the Growth Vectors compared to the prior-year quarter and the excellent profitability at Pharma. The strong performance year-to-date gives the scope to deliberately take some targeted investments in Q4/2025, for example in R&D.

- EBIT1 of the Growth Vectors increased by very strong 20%2 in constant currency and amounted to €194 million; EBIT margin1 improved by 140 bps to 15.9%, moving close to Kabi’s structural margin band.

- EBIT1 of Pharma increased 17%2 in constant currency to €202 million driven by Europe and the U.S as well as by ongoing productivity gains. EBIT margin1 at 22.0%.

Fresenius Helios with strong organic revenue growth; sequential margin improvement at Helios Germany driven by progressing Performance Programme; EBIT margin at Helios Spain as expected reflecting the usual seasonality; EBIT growth supported by earlier than expected contributions.

Strong 5% organic revenue growth driven by year-over-year activity levels increase at both, Helios Germany and Helios Spain; revenue increased by 5% in constant currency to €3,240 million.

- Helios Germany’s organic revenue growth was solid at 4% despite the elevated prior year revenue base resulting from technical reclassifications, reflecting strong admission growth and positive price effects; revenues at €2,019 million.

- Helios Spain with strong organic revenue growth of 7% to €1,221 million driven by good activity growth year-over-year, particularly in the ORP business, and price effects.

- EBIT1 of Fresenius Helios at €242 million and thus at constant currency growth broadly in line with the prior-year quarter; overall the EBIT development was impacted by the high prior-year base related to the energy relief payments in Germany as well as to the usual seasonality in Spain in the third quarter. This was partially compensated by the advancements of the performance program in Germany; EBIT margin1 of Fresenius Helios was at 7.5%.

- EBIT1 of Helios Germany decreased by -5% to €161 million against the high prior-year base which included energy relief funds; EBIT margin1 is walking up its way standing at 8.0% compared to 7.5% in Q2/2025 and 6.6% in Q4/2024, which was the first quarter without energy relief funds.

- EBIT1 of Helios Spain increased by 10% in constant currency to €80 million; EBIT margin1 at 6.6%, impacted by the summer season.

- Helios performance programme is advancing; material contributions expected in Q4/2025 with likely some spill-over into 2026 as some of the levers are process-related and will take time to deliver and realize benefits.

1 Before special items

2 Growth rate adjusted for Argentina hyperinflation

Conference call and Audio webcast

As part of the publication of the Q3/2025 results, a conference call will be held on November 5, 2025 at

1:30 p.m. CEST / 7:30 a.m. EDT. All investors are cordially invited to follow the conference call in a live audio webcast at https://www.fresenius.com/investors. Following the call, a replay will be available on our website.

Contact for shareholders

Investor Relations

Telephone: + 49 61 72 6 08-24 87

Telefax: + 49 61 72 6 08-24 88

E-mail: ir-fre@fresenius.com

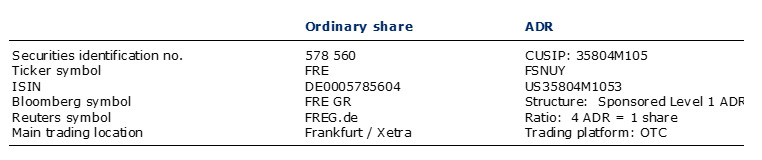

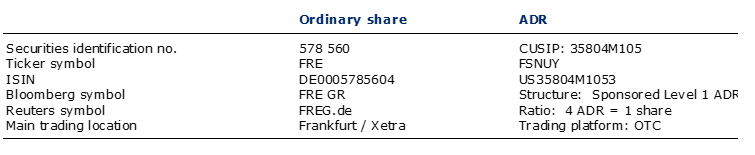

Information on Fresenius share and ADRs

Note on the presentation of financial figures

- If no timeframe is specified, information refers to Q3/2025.

- Consolidated results for Q3/2025 as well as for Q3/2024 include special items. An overview of the results for Q3/2025 - before and after special items – is available on our website.

- Growth rates in constant currency of Fresenius Kabi are adjusted. Adjustments relate to the hyperinflation in Argentina. Accordingly, constant currency growth rates of the Fresenius Group are also adjusted.

- Information on the performance indicators is available on our website at https://www.fresenius.com/alternative-performance-measures.

This release contains forward-looking statements that are subject to various risks and uncertainties. Future results could differ materially from those described in these forward-looking statements due to certain factors, e.g. changes in business, economic and competitive conditions, regulatory reforms, results of clinical trials, foreign exchange rate fluctuations, uncertainties in litigation or investigative proceedings, the availability of financing and unforeseen impacts of international conflicts. Fresenius does not undertake any responsibility to update the forward-looking statements in this release.

Q2/2025: Ongoing strong revenue and EPS growth, guidance for organic revenue growth raised

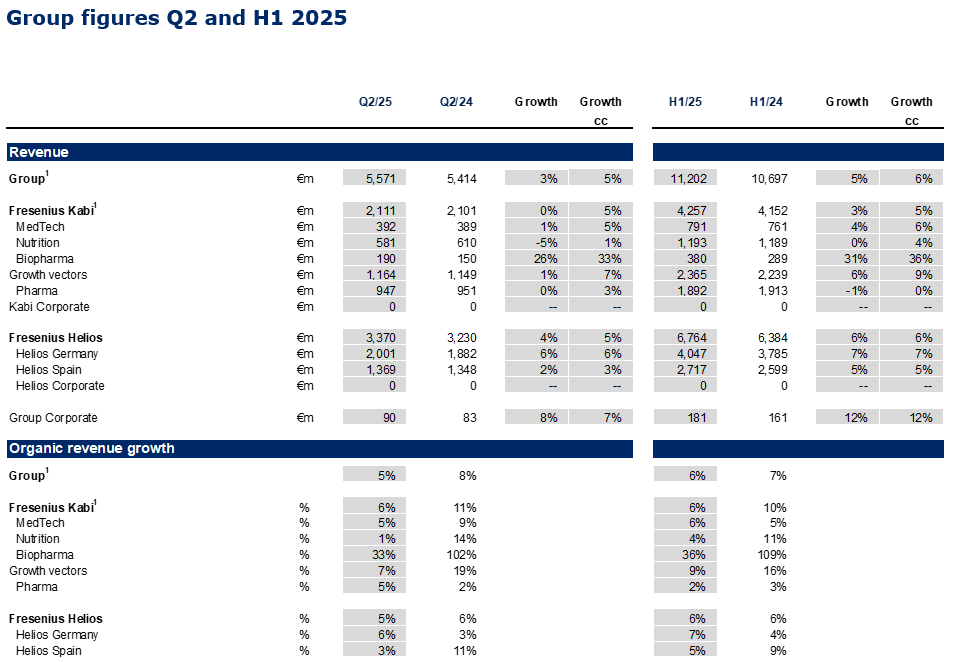

- Group revenue1 at €5,571 million with organic growth of 5%1,2 driven by consistent delivery across the core businesses Fresenius Kabi and Fresenius Helios as well as ongoing execution of #FutureFresenius.

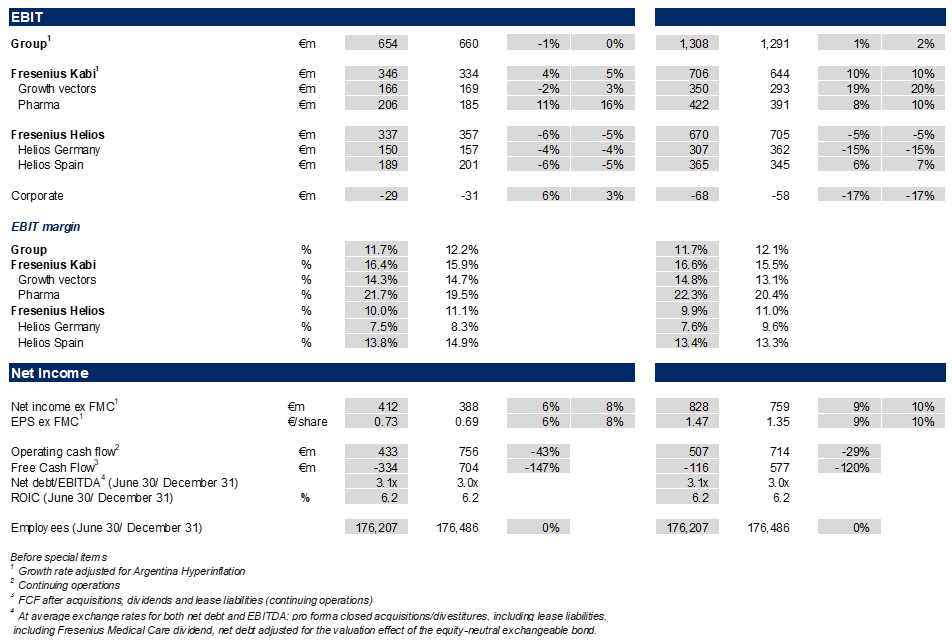

- Group EBIT1 broadly stable3 in constant currency at €654 million impacted by the headwinds from ceased energy relief payments at Helios Germany and the loss of the volume-based procurement tender for the nutrition product Ketosteril in China at Fresenius Kabi; Group EBIT margin1 at 11.7%.

- Net income1,4 with strong 8%3 growth in constant currency to €412 million outpacing revenue growth.

- EPS1,4 rose by strong 8%3 in constant currency to €0.73 demonstrating continued bottom-line delivery based on operating strength and significantly decreased interest expenses.

- Net debt/EBITDA ratio at 3.1x1,5 driven by resumed dividend payment in Q2/25.

- Pro rata sale of Fresenius Medical Care shares to maintain current stake in response to the announced Fresenius Medical Care share buyback program.

1Before special items

2Organic growth rate adjusted for accounting effects related to Argentina hyperinflation

3Growth rate adjusted for Argentina hyperinflation

4Excluding Fresenius Medical Care

5At average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures, including lease liabilities, including Fresenius Medical Care dividend, net debt adjusted for the valuation effect of the equity-neutral exchangeable bond

Michael Sen, CEO of Fresenius: “Fresenius has demonstrated a resilient and consistent performance in the first half of 2025, with another quarter of strong momentum reflected by 8% Core EPS growth. Fresenius Kabi and Fresenius Helios continue to deliver strong results despite macroeconomic challenges, thanks to our focused strategy and disciplined execution. This performance enables us to raise our guidance, increasing our full-year expectations for revenue growth to between 5% and 7%. #FutureFresenius is paying off.

Our ambitions remain unchanged: Our current strategy phase Rejuvenate will focus on organic growth through disciplined capital allocation - upgrading our core, and scaling our platforms to enhance performance further. We are committed to delivering profitable growth through targeted investments in health and digital innovation, which together will create and enhance value for our stakeholders."

Guidance raised for Fiscal Year 20251

Based on the consistent growth at the top-end of the 2025 guidance in H1/25, organic revenue guidance was raised:

Fresenius Group2: organic revenue growth3 now expected in the range of 5 to 7% (previous: 4 to 6%); constant currency EBIT growth4 in the range of 3% to 7%

Fresenius Kabi5: organic revenue growth3 in the mid- to high-single-digit percentage range; EBIT margin of 16.0% to 16.5%

Fresenius Helios6: organic revenue growth in the mid-single-digit percentage range; EBIT margin around 10%

Assumptions to guidance: When Fresenius gave guidance in February, the company acknowledged the fast-moving macro-economic and geopolitical environment, resulting in a higher level of operational uncertainty. Fresenius’ guidance continues to reflect current factors and known uncertainties such as impacts from tariffs to the extend they can currently be assessed. The guidance does not take into account potential extreme scenarios that could affect the company, its peers, and the healthcare sector as a whole.

1Before special items

22024 base: €21,526 million (revenue) and €2,489 million (EBIT)

3Organic growth rate adjusted for accounting effects related to Argentina hyperinflation

4Growth rate adjusted for Argentina hyperinflation

52024 base: €8,414 million (revenue) and €1,319 million (EBIT)

62024 base: €12,739 million (revenue) and €1,288 million (EBIT)

Fresenius Group – Business development Q2/25

In Q2/2025, the good operating performance of Fresenius Kabi and Fresenius Helios led to a 5%1 Group organic revenue increase to €5,571 million.

As expected, Group EBIT before special items was broadly stable3 in constant currency, and amounted to €654 million. This is related to the headwinds from the absence of energy relief payments at Helios Germany and the Volume Based Procurement of the nutrition product Ketosteril in China at Fresenius Kabi. Despite the negative effects, Group EBIT margin was 11.7% (Q2/24: 12.2%). The Helios Performance Programme is advancing with increasing contributions expected in the second half of the year.

Earnings per share2,4 rose by a strong 8%3 in constant currency to €0.73, driven by the operating strength and the significantly decreased interest expenses.

Following the announcement of Fresenius Medical Care AG (FME) in June 2025 to initiate a share buyback program, Fresenius intends to sell shares of FME on a pro rata basis to maintain its current stake of around 28.6% in FME. The final size and tranching of the sale of shares will be determined based on the structure of the share buyback program of FME. As previously announced, Fresenius remains a committed shareholder and will retain no less than 25 per cent plus one share of FME.

Fresenius will use the proceeds to invest in its core business in line with the #FutureFresenius strategy and Fresenius' stated capital allocation priorities, including further strengthening the balance sheet, reducing leverage, and delivering shareholder value and long-term growth.

1Organic growth rate adjusted for accounting effects related to Argentina hyperinflation

2Before special items

3Growth rate adjusted for Argentina hyperinflation

4Excluding Fresenius Medical Care

Operating Companies – Business development Q2/25

Fresenius Kabi delivered a strong performance; Growth Vectors with ongoing momentum, continued Biopharma strength; licensing agreement to commercialize a proposed vedolizumab biosimilar candidate

Organic revenue growth of 6%3 mainly driven by the Growth Vectors and the good contribution from Pharma; reflecting the less pronounced positive Argentina pricing effects; revenue was broadly flat at €2,111 million due to currency effects; increased by 5%2 in constant currency.

- Growth Vectors with good organic revenue3 increase of 7%: MedTech 5%, Nutrition 1%, Biopharma 33%.

- Nutrition revenue: €581 million, growth clearly influenced by the tender impact from the Volume Based Procurement (VBP) on Ketosteril in China (ex Ketosteril healthy organic growth in line with ambition range), good development in Latin America and Europe; in the U.S. ongoing successful roll-out of lipid emulsions.

- Biopharma revenue: €190 million, positive development mainly driven by the Tyenne biosimilar ramp up in Europe and the U.S. as well as Idacio; denosumab biosimilars Conexxence® (denosumab-bnht) and Bomyntra® (denosumab-bnht) launched in the U.S. and approved in Europe; expansion of autoimmune biosimilars portfolio: licensing agreement with Polpharma Biologics to commercialize a proposed vedolizumab biosimilar candidate (excluding region MENA).

- MedTech revenue: €392 million, increase driven by the expansion in Cell Therapy in the U.S., and solid growth in Europe.

- Pharma revenue: €947 million, strong organic revenue development3 with 5% growth based on good volumes including I.V. fluids in the U.S., and Europe with favourable pricing.

- EBIT1 of Fresenius Kabi with 5%2 constant currency increase to €346 million, driven by the strong margin development of the Pharma, MedTech and Biopharma business and ongoing improvements in the cost base. The EBIT margin1 was at the upper end of the guidance range at 16.4% despite transaction exchange rate effects and headwinds on the Nutrition business in China.

- EBIT1 of the Growth Vectors increased 3%2 in constant currency against the backdrop of the Ketosteril effect, and amounted to €166 million; EBIT margin1 at 14.3%.

- EBIT1 of Pharma increased 16%2 in constant currency to €206 million. EBIT margin1 was strong at 21.7% due to ongoing cost savings and some one-timers.

Fresenius Helios with solid organic revenue growth; expected softness in profitability at Helios Germany partially offset by good development at Helios Spain; Helios Performance Programme is advancing.

Strong 5% organic revenue growth driven by Helios Germany (6% organic growth); Helios Spain at 3% organic growth (H1/25: 5%) linked to the Easter effect, which resulted into less activity at the beginning of Q2/25 and impacted growth predominantly at Helios Spain; revenue before special items increased by 5% in constant currency to €3,370 million.

- Helios Germany with revenue1 of €2,001 million; growth mainly driven by price effects, as well as good activity levels and case mix.

- Helios Spain with revenue of €1,369 million, impacted by the Easter timing and currency translation effects related to the clinics in Latin America. The clinics in Latin America showed a good operational performance.

- EBIT1 of Fresenius Helios as expected declined -5% in constant currency to €337 million impacted by the absence of energy relief funds in Germany. This expected softness was partially compensated by the excellent profitability at Helios Spain. EBIT margin1 of Fresenius Helios was resilient at 10.0%.

- EBIT1 of Helios Germany decreased by -4% to €150 million against the high prior-year base which included energy relief funds; EBIT margin at 7.5% improved by 90 bps compared to Q4/24 (6.6%), the first quarter without energy relief funds.

- EBIT1 of Helios Spain decreased by -5% in constant currency to €189 million related to a very strong prior-year base and the Easter effect; EBIT margin1 at a strong 13.8%.

- Helios performance programme is advancing; ramp-up in H2/25 expected with more meaningful EBIT contributions, as some of the levers are process-related and will take time to deliver and realize benefits.

1Before special items

2Growth rate adjusted for Argentina hyperinflation.

3Organic growth rate adjusted for accounting effects related to Argentina hyperinflation

Conference call and Audio webcast

As part of the publication of the Q2/2025 results, a conference call will be held on August 6, 2025 at

1:30 p.m. CEST / 7:30 a.m. EDT. All investors are cordially invited to follow the conference call in a live audio webcast at https://www.fresenius.com/investors. Following the call, a replay will be available on our website.

Contact for shareholders

Investor Relations

Telephone: + 49 61 72 6 08-24 87

Telefax: + 49 61 72 6 08-24 88

E-mail: ir-fre@fresenius.com

Information on Fresenius share and ADRs

Note on the presentation of financial figures

- If no timeframe is specified, information refers to Q2/2025.

- Consolidated results for Q2/25 as well as for Q2/24 include special items. An overview of the results for Q2/2025 - before and after special items – is available on our website.

- Growth rates in constant currency of Fresenius Kabi are adjusted. Adjustments relate to the hyperinflation in Argentina. Accordingly, constant currency growth rates of the Fresenius Group are also adjusted.

- The results of Fresenius Helios and accordingly of the Fresenius Group for Q2/24 are adjusted by the sale of the fertility services group Eugin and the divestment of the majority stake in the hospital Clínica Ricardo Palma hospital in Lima, Peru.

- Information on the performance indicators is available on our website at https://www.fresenius.com/alternative-performance-measures.

This release contains forward-looking statements that are subject to various risks and uncertainties. Future results could differ materially from those described in these forward-looking statements due to certain factors, e.g. changes in business, economic and competitive conditions, regulatory reforms, results of clinical trials, foreign exchange rate fluctuations, uncertainties in litigation or investigative proceedings, the availability of financing and unforeseen impacts of international conflicts. Fresenius does not undertake any responsibility to update the forward-looking statements in this release.

Fresenius announced today that the European Commission has granted approval for their denosumab biosimilars Conexxence®* and Bomyntra®* in Europe.

The two approvals cover all indications of the reference products including osteoporosis in postmenopausal women and at-risk men, treatment-related bone loss, prevention of skeletal complications from cancer metastasis to bone, and giant cell tumor of bone.

This milestone marks a significant advancement in Fresenius Kabi’s mission to expand access to high-quality biosimilar therapies. It also reinforces the business’ commitment to strengthening its Biopharma platform, a key pillar of the #FutureFresenius strategy.

*Conexxence and *Bomyntra are registered trademarks of Fresenius Kabi Deutschland GmbH in selected countries.

Fresenius has published the Aide Memoire ahead of its Q2 2025 financial reporting. The Aide Memoire is a summary of relevant information that Fresenius has previously communicated previously to the capital market or otherwise made publicly available . The document may prove helpful in assessing Fresenius' financial performance ahead of the publication of quarterly results.

The Q2 2025 Aide Memoire is now available on the Fresenius Investor Relations website. The results of the second quarter and first half of 2025 of Fresenius SE & Co. KGaA will be published on 6 August 2025. The Quiet Period will start on 24 July 2025.

Q1/2025: Strong top line and excellent EPS growth, outlook confirmed

- Group revenue1 at €5.63 billion with strong organic growth of 7%1,2 driven by consistent delivery of Fresenius Kabi and a strong performance at Fresenius Helios.

- Group EBIT1 at €654 million, increase of 4%3 in constant currency on the back of strong operating performance at Kabi; absence of energy relief payments weighing on Helios Germany; Group EBIT margin1 of 11.6%.

- Net income1,4 grew by an excellent 12%3 in constant currency to €416 million significantly outpacing revenue growth.

- EPS1,4 rose by excellent 12%3 in constant currency to €0.74 resulting from broad based operational strength and lower interest expenses.

- Operating cash flow from continuing operations of €74 million significantly improved year-on-year driven by operating development and increased focus on cash generation.

- Leverage ratio within target corridor: Net debt/EBITDA ratio at 3.0x1,5 showing 80 bps improvement in the last twelve months.

- #FutureFresenius REJUVENATE phase: Pivotal milestone delivered with the reduction of participation in Fresenius Medical Care stake enhancing strategic flexibility while setting basis for long-term profitable growth.

1 Before special items

2 Organic growth rate adjusted for accounting effects related to Argentina hyperinflation.

3 Growth rate adjusted for Argentina hyperinflation.

4 Excluding Fresenius Medical Care

5 At average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures, including lease liabilities, including Fresenius Medical Care dividend, net debt adjusted for the valuation effect of the equity-neutral exchangeable bond.

Michael Sen, CEO of Fresenius: “We've kick-started 2025 with an excellent performance across the business and confirm our full-year guidance. Organic revenue increased by 7% driven by the consistent delivery of Fresenius Kabi and Fresenius Helios. This along with continued improvements in operations and lower interest costs led to an impressive EPS growth of 12%. Following the reduction of our stake in Fresenius Medical Care, a first and pivotal milestone in our history, we now start the REJUVENATE phase of #FutureFresenius from an even stronger position; this step underscores our commitment to creating long-term value. With a strengthened balance sheet and capital allocation priorities to further invest in our growth platforms, while also increasing our US presence, Fresenius is well positioned to deliver future profitable growth and innovation.”

Outlook confirmed for Fiscal Year 20251

Fresenius Group2: organic revenue growth3 of 4% to 6%,

constant currency EBIT growth in the range of 3% to 7%

Fresenius Kabi5: organic revenue growth3 in the mid- to high-single-digit percentage range; EBIT margin of 16.0% to 16.5%

Fresenius Helios6: organic revenue growth in the mid-single-digit percentage range; EBIT margin around 10%

Assumptions to guidance: When Fresenius gave guidance in February, the company acknowledged the fast-moving macro-economic and geopolitical environment, resulting in a higher level of operational uncertainty. Fresenius’ guidance continues to reflect current factors and known uncertainties such as potential impacts from tariffs to the extent they can currently be assessed. The guidance does not take into account potential extreme scenarios that could affect the company, its peers, and the healthcare sector as a whole.

1 Before special items

2 2024 base: €21,526 million (revenue) and €2,489 million (EBIT)

3 Organic growth rate adjusted for accounting effects related to Argentina hyperinflation.

4 Growth rate adjusted for Argentina hyperinflation

5 2024 base: €8,414 million (revenue) and €1,319 million (EBIT)

6 2024 base: €12,739 million (revenue) and €1,288 million (EBIT)

Fresenius Group – Business development Q1/25

Fresenius entered with excellent momentum into the year with strong organic growth above the top-end of the 2025 guidance. The consistent positive delivery of Fresenius Kabi and the strong performance at Fresenius Helios drove a 7%1 Group organic revenue2 increase to €5.63 billion. Due to a continued strong operating performance, Group EBIT before special items increased 4%3 in constant currency to €654 million despite the high prior-year quarter which included energy relief fundings at Helios Germany. Particularly, a strong performance at Kabi and Helios in Spain contributed to the EBIT growth. The Helios Performance Programme delivers some first contributions with more significant contributions expected in the second half of the year. Earnings per share2,4 rose by an excellent 12%3 in constant currency to €0.74, driven by a broad-based operational strength and improved interest costs against the backdrop of a strong cash flow development and successful deleveraging.

In Q1/25, Fresenius reached a pivotal milestone in #FutureFresenius with the reduction of participation in Fresenius Medical Care and the issuance of an exchangeable bond with Fresenius Medical Care shares underlying. These transactions underline Fresenius' clear commitment to long-term value creation and were the first visible signs of the REJUVENATE phase, which will focus on three key aspects in the coming years:

- Upgrade Core: Fresenius will continue to strengthen its core businesses. This includes, for example, reinforcing R&D pipelines, further increasing financial strength, and enhancing corporate culture.

- Scale Platforms: By strategically scaling its (Bio)Pharma, MedTech, and Care Provision platforms, Fresenius can make an important contribution to meeting the challenges facing healthcare systems around the world. The priorities are:

- Driving innovation at (Bio-)Pharma

- Expand MedTech to provide and connect technology solutions for critical clinical areas such as emergency rooms, operating rooms and intensive care units.

- Accelerate digitization of care provision

- Elevate Performance: Overall, REJUVENATE is designed to help the company achieve higher levels of performance and make Fresenius even more innovative and relevant.

1 Organic growth rate adjusted for accounting effects related to Argentina hyperinflation.

2 Before special items

3 Growth rate adjusted for Argentina hyperinflation

4 Excluding Fresenius Medical Care

Operating Companies – Business development Q1/25

Fresenius Kabi delivered a strong start to the year, Biopharma moving close to structural EBIT margin band

- Organic revenue growth of 6%1 clearly driven by the Growth vectors; revenue increased by 5% to €2,146 million; positive Argentina pricing effects continued but less pronounced.

- Growth vectors with strong organic revenue1 increase of 11%: MedTech 7%, Nutrition 7%, Biopharma 40%.

- Nutrition revenue: €612 million, benefited from positive pricing effects in Argentina and the good development in Europe; in the U.S. ongoing successful roll-out of lipid emulsions.

- Biopharma revenue: €190 million, mainly driven by the growth of Tyenne in Europe and the U.S.; launch of Ustekinumab biosimilar Otulfi® in EU and the U.S.; denosumab biosimilars Conexxence® (denosumab-bnht) and Bomyntra® (denosumab-bnht) approved by FDA.

- MedTech revenue: €399 million, driven by strong growth related to the Ivenix pump rollout in the U.S, and broad-based positive development across most regions.

- Pharma revenue: €946 million, flat organic revenue development1 against a high prior-year base; positive pricing development in Europe was offset by a softer development in the U.S. and China.

- China business continued to be impacted by a general economic weakness, price declines in connection with tenders, and hospital budget controls.

- EBIT2 of Fresenius Kabi with 16%3 constant currency increase to €360 million, driven by the strong revenue development of the Growth vectors and ongoing improvements in the cost base. The EBIT-margin2 was very strong at 16.8%, a 170 bps yoy expansion.

- EBIT2 of the Growth Vectors increased 45%3 in constant currency to €184 million against the backdrop of a broad-based positive development; EBIT margin2 at 15.3% increased by 390 bps year-on-year, Biopharma moving close to structural EBIT margin band.

- EBIT2 of Pharma increased 5%3 in constant currency to €216 million. EBIT margin2 was strong at 22.9% driven in particular by ongoing cost savings and a strong pricing development in Europe.

1 Organic growth rate adjusted for accounting effects related to Argentina hyperinflation.

2 Before special items

3 Growth rate adjusted for Argentina hyperinflation.

Fresenius Helios with excellent organic revenue growth; Helios Performance Programme evolving in-line with expectations.

- Very strong 8% organic revenue growth clearly above the structural growth band driven equally by Helios Germany (8% organic growth) and Helios Spain (8% organic growth); From a year-on-year perspective, Q1 also benefitted from the Easter effect falling in the second quarter this year; revenue before special items increased by 8% to €3,394 million.

- Helios Germany with revenue of €2,046 million; growth mainly driven by price effects: positive development of admissions and case mix.

- Helios Spain with revenue of €1,348 million, driven by strong activity levels and favourable price effects. The clinics in Latin America also showed a good performance.

- EBIT1 of Fresenius Helios declined 4% to €333 million as the support from energy relief funds phased out by the end of Q3/24. This expected softness was partially compensated by excellent profitability at Helios Spain. EBIT margin1 was solid at 9.8% driven by Helios Spain with a margin of 13.1% and 23% EBIT growth.

- EBIT1 of Helios Germany decreased by 23% to €157 million against the high prior-year base which included energy relief funds; EBIT margin at 7.7% improved by 110 bps sequentially (Q4/24: 6.6%).

- Helios performance programme delivers some first contributions; ramp-up in H2/25 with more significant EBIT contributions, as some of the levers are process-related and will take time to deliver and realize benefits.

1 Before special items

2 Growth rate adjusted for Argentina hyperinflation.

Conference call and Audio webcast

As part of the publication First Quarter 2025 results, a conference call will be held on May 7, 2025 at 1:30 p.m. CEST / 7:30 a.m. EST. All investors are cordially invited to follow the conference call in a live audio webcast at https://www.fresenius.com/investors. Following the call, a replay will be available on our website.

Contact for shareholders

Investor Relations

Telephone: + 49 61 72 6 08-24 87

Telefax: + 49 61 72 6 08-24 88

E-mail: ir-fre@fresenius.com

Information on Fresenius share and ADRs

Note on the presentation of financial figures

- If no timeframe is specified, information refers to Q1/2024

- Consolidated results for Q1/25 as well as for Q1/24 include special items. An overview of the results for Q1/2025 - before and after special items – is available on our website.

- Growth rates in constant currency of Fresenius Kabi are adjusted. Adjustments relate to the hyperinflation in Argentina. Accordingly, constant currency growth rates of the Fresenius Group are also adjusted.

- The results of Fresenius Helios and accordingly of the Fresenius Group for Q1/24 are adjusted by the sale of the fertility services group Eugin and the divestment of the majority stake in the hospital Clínica Ricardo Palma hospital in Lima, Peru.

- Information on the performance indicators is available on our website at https://www.fresenius.com/alternative-performance-measures.

This release contains forward-looking statements that are subject to various risks and uncertainties. Future results could differ materially from those described in these forward-looking statements due to certain factors, e.g. changes in business, economic and competitive conditions, regulatory reforms, results of clinical trials, foreign exchange rate fluctuations, uncertainties in litigation or investigative proceedings, the availability of financing and unforeseen impacts of international conflicts. Fresenius does not undertake any responsibility to update the forward-looking statements in this release.

Fresenius has completed the divestment of Vamed’s international project business to Worldwide Hospitals Group (WWH), that was announced in February 2025.

The divestment is part of Fresenius’ structured exit from its Investment Company Vamed and enables Fresenius to further increase focus and management capacity on the ongoing progress of its core businesses Fresenius Kabi and Fresenius Helios, in line with #FutureFresenius.

Today, Fresenius published its 2024 Annual Report. As already announced in February, the healthcare group grew profitably in the past year and achieved its outlook, which was raised twice, through consistently good business performance. Group revenue before special items increased to €21.5 billion, with organic growth of 8%. Fresenius was also able to reduce net debt by €2 billion in 2024.

“Our #FutureFresenius program, which we launched at the end of 2022, is having an impact. The “new” Fresenius is much more focused. We are concentrating on Fresenius Kabi and Fresenius Helios. These are growing profitably and under their own steam,” said Michael Sen, Chairman of the Management Board of Fresenius. “Growth, higher margins, more cash, lower debt – all this has created value: From the beginning of October 2022, when we prepared the ReSet, until February 28, 2025, the share price rose by 76%.”

For the first time, the Annual Report includes a sustainability report in accordance with the European Sustainability Reporting Standards (ESRS). This replaces the Non-financial Report of previous Annual Reports and expands and supplements reporting topics and details. In addition, the ESRS report, like the financial report, is audited externally.

The 2024 Annual Report is available in German and English as a PDF file and as an online version.

Further publication and event dates for 2025:

· 04/24/2025: Publication of Sustainability Highlights Magazine

· 05/07/2025: Publication of the financial results for Q1 2025

· 05/23/2025: Annual General Meeting

· 08/06/2025: Publication of the financial results for Q2 2025

· 11/05/2025: Publication of the financial results for Q3 2025

FY/24: Upgraded outlook achieved, consistent financial performance with profitable growth.

- Group revenue1 at €21.5 billion with strong organic growth of 8%1,2

- Group EBIT1 at €2.5 billion, increase of 10%3 in constant currency; EBIT margin1 of 11.6%, 40 bps above prior year

- Net income1,4 grew by 13%3 in constant currency to €1,461 million, outpacing revenue growth

- EPS1,4 grew to €2.59

- Accumulative Group structural productivity savings ahead of plan reached €474 million (planned €400 million)

- Excellent Group operating cash flow of €2.4 billion resulting from focused cash management

- Deleveraging continued, net debt/EBITDA ratio further improved to 3.0x1,5 driven by excellent cash flow. Improvement of more than 70 bps since YE/23

- Dividend proposal of €1.00 per share

Q4/2024: Continued growth and further deleveraging

- Group revenue1 at €5.5 billion with organic growth of 7%1,2 driven by consistent positive development of Kabi and a strong performance at Helios

- Group EBIT1 at €646 million with solid constant currency growth of 7%3 on the back of significant operational improvements at Kabi; end of energy relief payments weighing on Helios Germany; Group EBIT margin1 of 11.7%

- EPS1,4 with outstanding constant currency growth of 29%3 to €0.69, upward impact due to high tax rate in prior-year quarter

- Strong operating cashflow of close to €1 billion in Q4

1 Before special items

2 Organic growth rate adjusted for accounting effects related to Argentina hyperinflation.

3 Growth rate adjusted for Argentina hyperinflation.

4 Excluding Fresenius Medical Care

5 At average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures, including lease liabilities, including Fresenius Medical Care dividend

Michael Sen, CEO of Fresenius: “Thanks to a tremendous team effort, Fresenius delivered outstanding results in 2024 with high-single-digit organic revenue growth and double-digit EBIT and EPS growth. Our growth vectors – Nutrition, MedTech and Biopharma – and consistent performance from Helios paced this strong development. On top of this operating success, we ended the year with a significant reduction in leverage, which is at the lowest level in seven years. The momentum for success will continue through 2025, as we move to the next phase of #FutureFresenius and take the company to the next level of performance. For 2025 we expect 4% to 6% in revenue growth and 3% to 7% in EBIT growth. We have also upgraded our ambition level of the Fresenius Financial Framework. This includes higher margin ambitions for Kabi, and for the Group a lower leverage corridor. We also want to pass on our improving financial strength to our shareholders. Thus, we want to recommend a dividend payment for the year of 1 Euro per share. As we move forward, we continue to focus on performance and delivery. Our mission to save and improve human lives is unwavering: Fresenius is Committed to Life."

Outlook for Fiscal Year 2025

Fresenius Group5: Organic revenue growth1,2 of 4% to 6%,

constant currency EBIT growth3 in the range of 3% to 7%

Fresenius Kabi1: Organic revenue growth2,3 in the mid- to high-single-digit percentage range; EBIT margin of 16.0% to 16.5%

Fresenius Helios4: Organic revenue growth2 in the mid-single-digit percentage range; EBIT margin3 around 10%

Assumptions to guidance: Guidance assumes current factors and known uncertainties, but it does not reflect potential extreme scenarios from a fast-moving geopolitical environment.

1 Before special items

2 Organic growth rate adjusted for accounting effects related to Argentina hyperinflation.

3 Growth rate adjusted for Argentina hyperinflation.

4 Excluding Fresenius Medical Care

5 2024 base: €21,526 million (revenue) and €2,489 million (EBIT)

Fresenius Financial Framework – Ambitions further raised

- Structural EBIT margin3 ambition raised for Kabi to 16 to 18% (previously 14 to 17%).

- Self-imposed leverage target corridor upgraded to 2.5 to 3.0x net debt/EBITDA (previously 3.5 to 3.0x)

New dividend policy reflects capital allocation priorities

Fresenius’ new dividend policy is designed to ensure attractive shareholder returns while at the same time providing strategic flexibility. Going forward, Fresenius will pay out 30 to 40% of its Group core net income excluding Fresenius Medical Care and before special items as dividend. For fiscal year 2024, Fresenius will propose a dividend of €1.00 per share. The dividend proposal is a strong increase over the 2022 base and demonstrates Fresenius’ improving financial strength and its commitment to delivering shareholder value. For fiscal year 2023, Fresenius’ dividend payment was interrupted by legal restrictions due to the receipt of the energy relief payments at Helios in Germany.

1 2024 base: €8,414 million (revenue) and €1,319 million (EBIT)

2 Organic growth rate adjusted for accounting effects related to Argentina hyperinflation.

3 Before special items

4 2024 base: €12,739 million (revenue) and €1,288 million (EBIT)

5 At expected average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures; excluding further potential acquisitions/divestitures; before special items; including lease liabilities, including Fresenius Medical Care dividend

Fresenius Group – Business development FY/24

Fresenius closed fiscal year 2024 with a strong fourth quarter and achieved its twice-upgraded full-year guidance. The consistent positive delivery of Fresenius Kabi and the strong performance at Fresenius Helios, drove an 8%1 year-on-year Group organic revenue1 increase to €21.5 billion. Due to an improved operating business performance, Group EBIT before special items increased 10%3 in constant currency to €2.5 billion. Earnings per share2,4 rose by 13%3 in constant currency to €2.59.

End of 2024, the #FutureFresenius Revitalize phase has been successfully concluded, resulting in significant financial progress driven by a simpler Group structure, improved steering, an optimized portfolio and a refined operating model. In 2025, the focus will be on continued value creation by entering the Rejuvenate phase, which also aims to pursue platform-driven growth. In 2025 the emphasis will be on further debt reduction, delivering higher Kabi margins, drive Helios’ programme and fostering innovation.

A dedicated performance programme for Helios has been set up to increase efficiency and productivity, and to counteract the end of the energy relief funding. The programme is expected to contribute ~€100 million at EBIT level by 2025 at Helios Germany. Combined with further incremental growth of Helios in Germany and Spain, the Fresenius Helios EBIT margin is expected to be around 10% in FY/25. Contributions from the performance programme will be weighted to the second half of 2025, in particular, as some of the levers are process-related and will take time to deliver and realize benefits. Some of the performance measures are likely to materialize fully beyond 2025. This sets an excellent basis for further improving productivity within the 10 to 12% structural margin band in 2026 and beyond.

1 Organic growth rate adjusted for accounting effects related to Argentina hyperinflation.

2 Before special items

3 Growth rate adjusted for Argentina hyperinflation

4 Ex Fresenius Medical Care

Operating Companies – Business development FY/24 and Q4

Fresenius Kabi

In FY/24, Fresenius Kabi delivered consistent financial performance over the course of the year with excellent organic revenue growth of 10% above the top-end of the structural growth band and an impressive EBIT margin expansion of 140 bps to 15.7%.

Q4/24: Fresenius Kabi delivered a strong finish to the year

- Organic revenue growth of 9%1 driven by positive pricing effects, particularly in Argentina, revenue increased by 8% to €2,148 million.

- Growth vectors with strong organic revenue1 increase of 18%: MedTech 7%, Nutrition 21%, Biopharma 39%.

- Nutrition revenue: €614 million, benefited from positive pricing effects in Argentina and the good development in the U.S., driven by the ongoing roll-out of lipid emulsions.

- Biopharma revenue: €144 million, driven by the overall good rollout of Tyenne in Europe and the U.S.

- MedTech revenue: €424 million, driven by a broad-based positive development across most regions, including the U.S. and Europe

- Pharma revenue: €966 million, flat organic revenue development1; the positive development in many regions was offset by a softer development in China.

- China business continued to be impacted by a general economic weakness, price declines in connection with tenders, and indirect effects of the government’s countrywide anti-corruption campaign.

- EBIT2 of Fresenius Kabi grew 21% to €340 million, driven by good revenue development and improved structural productivity. The EBIT-margin2 was 15.8%, a 170 bps expansion.

- EBIT2 of the Growth Vectors increased by 71% on a positive development across the board; EBIT margin2 was 14.7%. EBIT positive in Biopharma in FY/24.

- EBIT2 of Pharma increased by 5% to €198 million. EBIT margin2 was 20.5% driven in particulars by cost discipline.

1 Organic growth rate adjusted for the accounting effects related to Argentina hyperinflation.

2 Before special items

Fresenius Helios

In FY 2024, Fresenius Helios delivered organic revenue growth of 6% driven by solid activity growth and favorable price developments in Germany and Spain. EBIT margin of 10.1%1 within the structural margin band ambition.

Q4/24: Fresenius Helios with strong EBIT development in Spain; end of energy relief payments weighing on Helios Germany

- Strong 6% organic revenue growth at the top-end of structural growth band driven equally by Helios Germany (6% organic growth) and Helios Spain (6% organic growth); revenue before special items increased 6% to €3,273 million.

- Helios Germany with revenue of €1,937 million; growth driven by pricing effects and admissions growth.

- Helios Spain with revenue before special items of €1,336 million, driven by solid activity levels and favourable price effects. The clinics in Latin America also showed a good performance.

- EBIT1 of Fresenius Helios declined 5% to €339 million as the energy relief funds ended in Q4. EBIT margin1 was solid at 10.4% driven by the excellent profitability at Helios Spain with a margin of 15.8% and 15% EBIT growth.

- EBIT1 of Helios Germany decreased by 22% to €128 million as the prior-year quarter was significantly supported by energy relief funds.

- Dedicated Helios performance programme initiated to drive further operational excellence and compensate end of energy relief funding in Germany. Fresenius Helios EBIT margin is expected to be around 10% in FY/25.

1 Before special items

Group figures Q4 & FY 2024

Conference call and Audio webcast

As part of the publication Fourth Quarter and Full Year 2024 results, a conference call will be held on February 26, 2025 at 1:30 p.m. CET (7:30 a.m. EST). All investors are cordially invited to follow the conference call in a live audio webcast at www.fresenius.com/investors. Following the call, a replay will be available on our website.

Contact for shareholders

Investor Relations

Telephone: + 49 61 72 6 08-24 87

Telefax: + 49 61 72 6 08-24 88

E-mail: ir-fre@fresenius.com

Note on the presentation of financial figures

- If no timeframe is specified, information refers to Q4/2024.

- Consolidated results for Q4/24 as well as for Q4/23 include special items. An overview of the results for Q4/2024 - before and after special items – is available on our website.

- The results of Fresenius Helios and accordingly of the Fresenius Group for Q4/24 and Q4/23 are adjusted by the sale of the fertility services group Eugin and the divestment of the majority stake in the hospital Clínica Ricardo Palma hospital in Lima, Peru.

- Growth rates in constant currency of Fresenius Kabi are adjusted. Adjustments relate to the hyperinflation in Argentina. Accordingly, in constant currency growth rates of the Fresenius Group are also adjusted.

- Information on the performance indicators is available on our website at www.fresenius.com/alternative-performance-measures.

This release contains forward-looking statements that are subject to various risks and uncertainties. Future results could differ materially from those described in these forward-looking statements due to certain factors, e.g. changes in business, economic and competitive conditions, regulatory reforms, results of clinical trials, foreign exchange rate fluctuations, uncertainties in litigation or investigative proceedings, the availability of financing and unforeseen impacts of international conflicts. Fresenius does not undertake any responsibility to update the forward-looking statements in this release.