If no timeframe is specified, information refers to Q1-3/2017

Q3/2017:

- Sales: €8.3 billion (+12%, +15% in constant currency)

- EBIT1: €1,129 million (+5%, +9% in constant currency)

- Net income2,3 (adjusted): €423 million (+11%, +14% in constant currency)

- Net income2: €396 million (+4%, +7% in constant currency)

Q1-3/2017:

- Sales: €25.2 billion (+16%, +16% in constant currency)

- EBIT1: €3,522 million (+15%, +15% in constant currency)

- Net income2,3 (adjusted): €1,339 million (+20%, +20% in constant currency)

- Net income2: €1,303 million (+17%, +17% in constant currency)

Stephan Sturm, CEO of Fresenius, said: “We can report another very good quarter, once again boosted by strong sales and earnings growth. The prospects for our businesses remain excellent. We are therefore confirming our guidance and are heading towards yet another record year. From this position of strength, we intend to swiftly close and integrate our strategically important acquisitions. Thus, we are expanding our range of high-quality, affordable healthcare products and services for the benefit of our patients and our company.“

1 Before acquisition-related expenses2 Net income attributable to shareholders of Fresenius SE & Co. KGaA3 Consistent with scope of original guidance: before acquisition-related expenses; before expenditures for further development of biosimilars business

For a detailed overview of adjustments, please see the reconciliation tables on page 15-16 in the pdf document.

2017 Group guidance confirmed

Fresenius confirms its guidance for 2017. Group sales are expected to increase by 15% to 17% in constant currency. Group net income1,2,3 is expected to grow by 19% to 21% in constant currency.

Including the acquisition of Merck KGaA’s biosimilars business and pro forma the acquisition of Akorn, the net debt/EBITDA4 ratio is expected to be approximately 3.3 at the end of 2017.

16% sales growth in constant currency

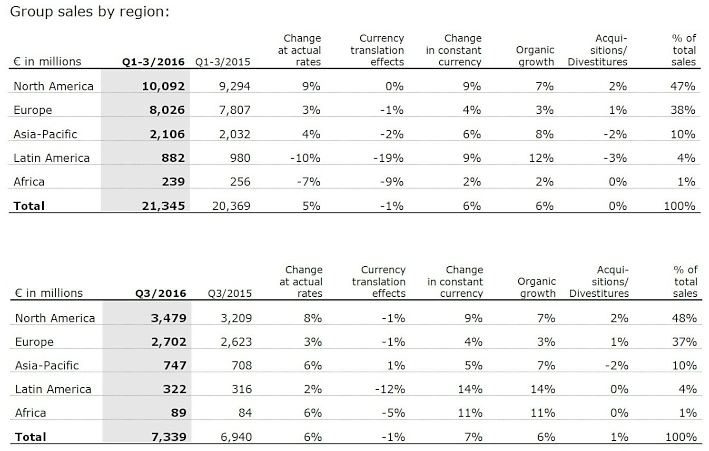

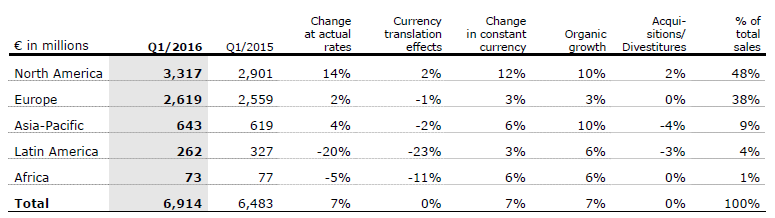

Group sales increased by 16% (16% in constant currency) to €25,191 million (Q1-3/2016: €21,651 million). Organic sales growth was 6%5 while acquisitions contributed 10%. In Q3/2017, Group sales increased by 12% (15% in constant currency) to €8,297 million (Q3/2016: €7,433 million). Negative currency translation effects (-3%) were mainly related to the devaluation of the US dollar. Organic sales growth was 6% while acquisitions contributed 9%.

1 Net income attributable to shareholders of Fresenius SE & Co. KGaA2 Before acquisition-related expenses of ~€50 m3 Before expected expenditures for further development of biosimilars business of ~€60 m4 Net debt and EBITDA at FY average exchange rates; before acquisition-related expenses of ~€50 m; excluding further potential acquisitions5 Excluding effects of Fresenius Medical Care’s agreement with the United States Departments of Veterans Affairs and Justice (VA agreement)

For a detailed overview of adjustments, please see the reconciliation tables on page 15-16 in the pdf document.

20% adjusted net income2,3 growth in constant currency

Group EBITDA4 increased by 16% (16% in constant currency) to €4,579 million (Q1-3/2016: €3,959 million). Group EBIT4 increased by 15% (15% in constant currency) to €3,522 million (Q1-3/2016: €3,058 million) with an EBIT margin4 of 14.0% (Q1-3/2016: 14.1%). In Q3/2017, Group EBIT4 increased by 5% (9% in constant currency) to €1,129 million (Q3/2016: €1,071 million) with an EBIT margin4 of 13.6% (Q3/2016: 14.4%).

Group net interest4 reached -€484 million (Q1-3/2016: -€433 million). The increase is mainly driven by the financing of the Quirónsalud acquisition.

1 Including effects of VA agreement2 Net income attributable to shareholders of Fresenius SE & Co. KGaA3 Consistent with scope of original guidance: before acquisition-related expenses; before expenditures for further development of biosimilars business4 Before acquisition-related expenses

For a detailed overview of adjustments, please see the reconciliation tables on page 15-16 in the pdf document.

The Group tax rate1 was 28.1% (Q1-3/2016: 28.2%). In Q3/2017, the Group tax rate1 decreased to 27.4% (Q3/2016: 27.9%), mainly driven by a re-evaluation of estimated future tax payments at Fresenius Medical Care.

Noncontrolling interest increased to €854 million (Q1-3/2016: €768 million), of which 95% was attributable to the noncontrolling interest in Fresenius Medical Care.

Adjusted Group net income2,3 increased by 20% (20% in constant currency) to €1,339 million (Q1-3/2016: €1,118 million). Adjusted earnings per share2,3 increased by 19% (19% in constant currency) to €2.42 (Q1-3/2016: €2.04). In Q3/2017, adjusted Group net income2,3 increased by 11% (14% in constant currency) to €423 million (Q3/2016: €382 million). Adjusted earnings per share2,3 increased by 11% (14% in constant currency) to €0.77 (Q3/2016: €0.69).

Group net income before acquisition-related expenses1,2 increased by 19% (19% in constant currency) to €1,329 million (Q1-3/2016: €1,118 million). Earnings per share1,2 increased by 18% (18% in constant currency) to €2.40 (Q1-3/2016: €2.04). In Q3/2017, Group net income1,2 increased by 8% (11% in constant currency) to €413 million (Q3/2016: €382 million). Earnings per share1,2 increased by 8% (11% in constant currency) to €0.75 (Q3/2016: €0.69).

Group net income2 increased by 17% (17% in constant currency) to €1,303 million (Q1-3/2016: €1,118 million). Earnings per share2 increased by 15% (15% in constant currency) to €2.35 (Q1-3/2016: €2.04). In Q3/2017, Group net income2 increased by 4% (7% in constant currency) to €396 million (Q3/2016: €382 million). Earnings per share2 increased by 3% (6% in constant currency) to €0.71 (Q3/2016: €0.69).

1 Before acquisition-related expenses2 Net income attributable to shareholders of Fresenius SE & Co. KGaA3 Consistent with scope of original guidance: before acquisition-related expenses; before expenditures for further development of biosimilars business

For a detailed overview of adjustments, please see the reconciliation tables on page 15-16 in the pdf document.

Continued investment in growth

Spending on property, plant and equipment was €1,137 million (Q1-3/2016: €1,059 million), primarily for the modernization and expansion of dialysis clinics, production facilities as well as hospitals and day clinics. Total acquisition spending of €6,662 million (Q1-3/2016: €592 million) was mainly related to the acquisitions of Quirónsalud and Merck KGaA’s biosimilars business.

Strong operating cash flow

Operating cash flow increased by 24% to €2,821 million (Q1-3/2016: €2,273 million). The cash flow margin increased to 11.2% (Q1-3/2016: 10.5%). In Q3/2017, operating cash flow increased by 21% to €1,138 million (Q3/2016: €940 million), with a margin of 13.7% (Q3/2016: 12.6%).

Free cash flow before acquisitions and dividends increased by 41% to €1,705 million (Q1-3/2016: €1,206 million). Free cash flow after acquisitions and dividends was -€5,233 million (Q1-3/2016: €252 million).

Solid balance sheet structure

The Group’s total assets increased by 14% (20% in constant currency) to €53,097 million (Dec. 31, 2016: €46,697 million), mainly due to the acquisition of Quirónsalud. Current assets grew by 10% (16% in constant currency) to €12,870 million (Dec. 31, 2016: €11,744 million). Non-current assets increased by 15% (22% in constant currency) to €40,227 million (Dec. 31, 2016: € 34,953 million).

Total shareholders’ equity grew by 2% (10% in constant currency) to €21,167 million (Dec. 31, 2016: €20,849 million). The equity ratio was 39.9% (Dec. 31, 2016: 44.6%).

Group debt increased by 32% (37% in constant currency) to €19,496 million (Dec. 31, 2016: € 14,780 million), mainly driven by the acquisition financing of Quirónsalud. As of September 30, 2017, the net debt/EBITDA ratio was 2.971,2 (Dec. 31, 2016: 2.331; pro forma Quirónsalud 3.091).

1 Net debt and EBITDA at LTM average exchange rates2 Before acquisition-related expenses

For a detailed overview of adjustments, please see the reconciliation tables on page 15-16 in the pdf document.

Business Segments

Fresenius Medical Care

Fresenius Medical Care is the world's largest provider of products and services for individuals with chronic kidney failure. As of September 30, 2017, Fresenius Medical Care was treating 317,792 patients in 3,714 dialysis clinics. Along with its core business, the company seeks to expand the range of medical services in the field of care coordination.

- Solid Q3 despite impact from natural disasters in North America

- 8% constant currency sales growth in Q3

- 2017 outlook confirmed2

Sales increased by 10% (10% in constant currency, 7% organic) to €13,355 million (Q1-3/2016: €12,153 million). Acquisitions and the agreement with the United States Departments of Veterans Affairs and Justice (VA agreement) contributed 3% in total. In Q3/2017, sales increased by 3% (8% in constant currency, 6% organic) to €4,336 million (Q3/2016: €4,211 million).

Health Care Services sales (dialysis services and care coordination) increased by 11% (10% in constant currency) to €10,950 million (Q1-3/2016: €9,910 million). Product sales increased by 7% (7% in constant currency) to €2,404 million (Q1-3/2016: €2,244 million).

In North America, sales increased by 10% (10% in constant currency) to €9,715 million (Q1-3/2016: €8,828 million). Health Care Services sales grew by 10% (10% in constant currency) to €9,086 million (Q1-3/2016: €8,224 million). Product sales increased by 4% (4% in constant currency) to €629 million (Q1-3/2016: €604 million).

Sales outside North America increased by 9% (10% in constant currency) to €3,628 million (Q1-3/2016: €3,315 million). Health Care Services sales increased by 11% (11% in constant currency) to €1,864 million (Q1-3/2016: €1,686 million). Product sales increased by 8% (8% in constant currency) to €1,764 million (Q1-3/2016: €1,630 million).

1 Net income attributable to shareholders of Fresenius Medical Care AG & Co. KGaA2 Excluding effects of VA agreement and natural disaster costs

EBIT increased by 10% (10% in constant currency) to €1,843 million (Q1-3/2016: €1,679 million). The EBIT margin was 13.8% (Q1-3/2016: 13.8%). In Q3/2017, EBIT was on the prior-year level (increased by 4% in constant currency) at €608 million (Q3/2016: €611 million). Foreign currency effects, lower contributions from the vascular business, higher costs in the pharmacy services business and natural disaster costs in North America negatively impacted EBIT, while organic growth and lower research and development expenses contributed positively. The EBIT margin was 14.0% (Q3/2016: 14.5%).

Net income1 increased by 13% (14% in constant currency) to €886 million (Q1-3/2016: €781 million). Consistent with the original scope of guidance, i.e. excluding the effects of the VA agreement and natural disaster costs, net income1 increased by 8% in constant currency. In Q3/2017, net income1 grew by 2% (6% in constant currency) to €309 million (Q3/2016: €304 million). Excluding the effects of the VA agreement and natural disaster costs, net income1 increased by 5% (8% in constant currency).

Operating cash flow increased by 43% to €1,664 million (Q1-3/2016: €1,160 million). The cash flow margin increased to 12.5% (Q1-3/2016: 9.5%). In Q3/2017, operating cash flow increased by 56% to €612 million (Q3/2016: €393 million) with a cash flow margin of 14.1% (Q3/2016: 9.3%). The increase is primarily attributable to last year’s cash contribution to a pension plan in the United States as well as other working capital items.

Fresenius Medical Care confirms its outlook for 2017. The company expects sales to grow by 8% to 10%2 in constant currency. Net income1,3 is expected to increase by 7% to 9% in constant currency.

For further information, please see Fresenius Medical Care’s Investor News at www.freseniusmedicalcare.com.

1 Net income attributable to shareholders of Fresenius Medical Care AG & Co. KGaA2 Excluding effects of VA agreement3 Excluding effects of VA agreement and natural disaster costs

Fresenius Kabi

Fresenius Kabi offers intravenously administered generic drugs, clinical nutrition and infusion therapies for seriously and chronically ill patients in the hospital and outpatient environments. The company is also a leading supplier of medical devices and transfusion technology products.

- 7% organic sales growth in Q3; positive contributions from all regions

- 11% adjusted EBIT growth2 in constant currency in Q3

- 2017 outlook confirmed

Sales increased by 7% (7% in constant currency, 7% organic) to €4,764 million (Q1-3/2016: €4,457 million). Acquisitions/divestitures had no meaningful impact on sales. In Q3/2017, sales increased by 3% (7% in constant currency, 7% organic) to €1,562 million (Q3/2016: €1,511 million). Negative currency translation effects (-4%) were mainly related to the devaluation of the US dollar and the Chinese yuan against the Euro.

Sales in Europe increased by 4% (5% organic) to €1,635 million (Q1-3/2016: €1,569 million). In Q3/2017, sales increased by 3% (4% organic) to €538 million (Q3/2016: €521 million).

Sales in North America increased by 7% (6% organic) to €1,736 million (Q1-3/2016: €1,628 million). In Q3/2017, sales increased by 1% (7% organic) to €549 million (Q3/2016: €542 million).

Sales in Asia-Pacific increased by 9% (11% organic) to €894 million (Q1-3/2016: €821 million). In Q3/2017, sales increased by 8% (12% organic) to €312 million (Q3/2016: €290 million).

Sales in Latin America/Africa increased by 14% (10% organic) to €499 million (Q1-3/2016: €439 million). In Q3/2017, sales increased by 3% (8% organic) to €163 million (Q3/2016: €158 million).

1 Before acquisition-related expenses2 Consistent with scope of original guidance: before acquisition-related expenses; before expenditures for further development of biosimilars business3 Net income attributable to shareholders of Fresenius SE & Co. KGaA

For a detailed overview of adjustments, please see the reconciliation tables on page 15-16 in the pdf document.

Adjusted EBIT1 increased by 6% (7% in constant currency) to €919 million (Q1-3/2016: €863 million). The adjusted EBIT margin1 was 19.3% (Q1-3/2016: 19.4%). In Q3/2017, adjusted EBIT1 increased by 6% (11% in constant currency) to €297 million (Q3/2016: €281 million), despite expenses related to hurricane Maria on Puerto Rico. The adjusted EBIT margin1 increased to 19.0% (Q3/2016: 18.6%).

EBIT2 increased by 5% (6% in constant currency) to €905 million (Q1-3/2016: €863 million). The EBIT margin2 was 19.0% (Q1-3/2016: 19.4%). In Q3/2017, EBIT2 increased by 1% (6% in constant currency) to €283 million (Q3/2016: €281 million). Given the €14 million expenditure for the further development of the biosimilars business, the EBIT margin2 decreased to 18.1% (Q3/2016: 18.6%).

Adjusted net income1,3 increased by 13% (14% in constant currency) to €554 million (Q1-3/2016: €491 million). In Q3/2017, adjusted net income1,3 increased by 13% (19% in constant currency) to €175 million (Q3/2016: €155 million).

While operating cash flow reached a very strong €640 million, it could not match the exceptional prior-year figure (Q1-3/2016: €661 million). The same applied to the strong margin of 13.4% (Q1-3/2016: 14.8%). In Q3/2017, operating cash flow reached a healthy €245 million (Q3/2016: €322 million) despite a cash prepayment for the biosimilars business and adverse currency translation effects. The cash flow margin was 15.7% (Q3/2016: 21.3%). Excluding the prepayment, operating cash flow was €290 with a margin of 18.6%.

Fresenius Kabi confirms its outlook for 2017 and expects 5% to 7% organic sales growth and EBIT growth in constant currency of 6% to 8%4,5.

1 Consistent with scope of original guidance: before acquisition-related expenses; before expenditures for further development of biosimilars business2 Before acquisition-related expenses3 Net income attributable to shareholders of Fresenius SE & Co. KGaA4 Before acquisition-related expenses of ~€50 m5 Before expected expenditures for further development of biosimilars business of ~€60 mFor a detailed overview of adjustments, please see the reconciliation tables on page 15-16 in the pdf document.

Fresenius Helios

Fresenius Helios is Europe's leading private hospital operator. The company comprises Helios Kliniken in Germany and Quirónsalud in Spain. Helios Kliniken operates 111 hospitals, thereof 88 acute care clinics and 23 post-acute care clinics, and treats more than 5.2 million patients annually. Quirónsalud operates 44 hospitals, 44 outpatient centers and around 300 occupational risk prevention centers, and treats approximately 9.7 million patients per year.

- 47% sales growth (4% excluding Quirónsalud) in Q3

- 33% EBIT increase (9% excluding Quirónsalud) in Q3

- 2017 outlook confirmed

Fresenius Helios increased sales by 47% (4% organic) to €6,422 million (Q1-3/2016: €4,382 million). Acquisitions, mainly Quirónsalud, increased sales by 43%. In Q3/2017, sales increased by 47% (4% organic) to €2,166 million (Q3/2016: €1,470 million).

Sales of Helios Kliniken2 increased by 4% (4% organic) to €4,562 million (Q1-3/2016: €4,382 million). In Q3/2017, sales increased by 4% (4% organic) to €1,524 million (Q3/2016: €1,470 million). Quirónsalud has been consolidated since February 1, 2017 and generated sales of €1,860 million (thereof €642 million in Q3/2017).

Fresenius Helios grew EBIT by 52% to €769 million (Q1-3/2016: €507 million). The EBIT margin increased to 12.0% (Q1-3/2016: 11.6%). In Q3/2017, EBIT increased by 33% to €232 million (Q3/2016: €175 million). The EBIT margin decreased to 10.7% (Q3/2016: 11.9%) due to the anticipated lower contribution of Quirónsalud during the summer months.

EBIT of Helios Kliniken2 increased by 8% to €549 million (Q1-3/2016: €507 million) with a margin of 12.0% (Q1-3/2016: 11.6%). In Q3/2017, EBIT of Helios Kliniken2 increased by 9% to €190 million (Q3/2016: €175 million) with a margin of 12.5% (Q3/2016: 11.9%). EBIT of Quirónsalud was €220 million (thereof €42 million in Q3/2017) with a margin of 11.8% (Q3/2017: 6.5%).

Fresenius Helios increased net income1 by 31% to €526 million (Q1-3/2016: €402 million). In Q3/2017, net income1 increased by 9% to €153 million (Q3/2016: €140 million).

Operating cash flow increased by 28% to €560 million (Q1-3/2016: €437 million) driven by the first-time consolidation of Quirónsalud. The margin was 8.7% (Q1-3/2016: 10.0%).

Fresenius Helios confirms its outlook for 2017 and projects organic sales growth of 3% to 5%2 and sales of ~€8.6 billion (thereof Quirónsalud ~€2.5 billion3). EBIT is expected to increase to €1,020 to €1,070 million (thereof Quirónsalud €300 to 320 million3).

1 Net income attributable to shareholders of Fresenius SE & Co. KGaA2 Helios Kliniken Germany, excluding Quirónsalud3 Quirónsalud consolidated for 11 months

Fresenius Vamed

Fresenius Vamed manages projects and provides services for hospitals and other health care facilities worldwide. The portfolio ranges along the entire value chain: from project development, planning, and turnkey construction, via maintenance and technical management, to total operational management.

- 9% sales growth in service business in Q3

- Project business with strong order intake of €285 million in Q3

- 2017 outlook confirmed

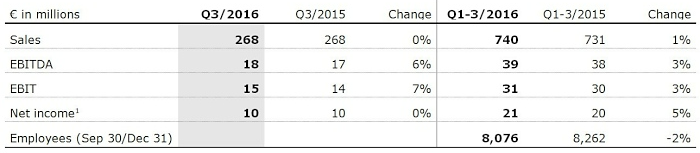

Sales increased by 1% (1% organic) to €748 million (Q1-3/2016: €740 million). Sales in the project business decreased by 7% to €301 million (Q1-3/2016: €325 million). Sales in the service business grew by 8% to €447 million (Q1-3/2016: €415 million). In Q3/2017, sales remained stable at €267 million (Q3/2016: €268 million).

EBIT increased by 3% to €32 million (Q1-3/2016: €31 million). The EBIT margin increased to 4.3% (Q1-3/2016: 4.2%). In Q3/2017, EBIT of €15 million (margin 5.6%) remained unchanged from previous year’s quarter.

Net income1 remained stable at €21 million (Q1-3/2016: €21 million). In Q3/2017, net income1 remained unchanged at €10 million (Q3/2016: €10 million).

Order intake reached a strong €697 million (Q1-3/2016: €674 million). In Q3/2017 order intake increased by 36% to €285 million. As of September 30, 2017, order backlog grew to an all-time high of €2,345 million (December 31, 2016: €1,961 million).

Fresenius Vamed confirms its outlook for 2017 and expects both organic sales growth and EBIT growth in the range of 5% to 10%.

1 Net income attributable to shareholders of VAMED AG

Conference Call

As part of the publication of the results for the first nine months of 2017, a conference call will be held on November 2, 2017 at 2 p.m. CET (9 a.m. EDT). All investors are cordially invited to follow the conference call in a live broadcast over the Internet at www.fresenius.com/investors. Following the call, a replay will be available on our website.

For additional information on the performance indicators, please refer to our website www.fresenius.com/alternative-performance-measures.

Diese Mitteilung enthält zukunftsbezogene Aussagen, die gewissen Risiken und Unsicherheiten unterliegen. Die zukünftigen Ergebnisse können erheblich von den zur Zeit erwarteten Ergebnissen abweichen, und zwar aufgrund verschiedener Risikofaktoren und Ungewissheiten wie zum Beispiel Veränderungen der Geschäfts-, Wirtschafts- und Wettbewerbssituation, Gesetzesänderungen, Ergebnisse klinischer Studien, Wechselkursschwankungen, Ungewissheiten bezüglich Rechtsstreitigkeiten oder Untersuchungsverfahren und die Verfügbarkeit finanzieller Mittel. Fresenius übernimmt keinerlei Verantwortung, die in dieser Mitteilung enthaltenen zukunftsbezogenen Aussagen zu aktualisieren.

Fresenius Helios continues to invest in the expansion and modernization of its hospitals and clinics. HELIOS Clinic Geesthacht, located just east of Hamburg, has opened an extension with 20 additional neurological rehabilitation places for young people. The investment in the specialist clinic for neurology and neurological rehabilitation is €4.6 million. In the state of Saxony, meanwhile, work has started on a new building for the emergency ward at HELIOS Hospital Leisnig. This €3.3 million project is scheduled for completion in autumn 2018.

If no timeframe is specified, information refers to H1/2017

Q2/2017:

- Sales: €8.5 billion (+18%, +17% in constant currency)

- EBIT1: €1,177 million (+14%, +13% in constant currency)

- Net income1,2: €459 million (+21%, +21% in constant currency)

H1/2017:

- Sales €16.9 billion (+19%, +17% in constant currency)

- EBIT1: €2,393 million (+20%, +19% in constant currency)

- Net income1,2: €916 million (+24%, +23% in constant currency)

Stephan Sturm, CEO of Fresenius, said: “We were able to sustain our strong momentum also in the second quarter. Strong increases in sales and earnings have put us well on track to reach our full-year targets. We are very pleased with the business development of Quirónsalud while its integration into Fresenius is proceeding according to plan. A focus in the second half will be to close the acquisitions announced by Fresenius Kabi. Those will put our business on an even broader foundation for future growth.”

1 Before special items2 Net income attributable to shareholders of Fresenius SE & Co. KGaA

2017 Group guidance confirmed

Fresenius confirms its guidance for 2017. Group sales are expected to increase by 15% to 17% in constant currency. Group net income1,2,3 is expected to grow by 19% to 21% in constant currency.

Pro forma the acquisitions of Akorn and Merck KGaA’s biosimilars business, the net debt/EBITDA4 ratio is expected to be approximately 3.3 at the end of 2017.

17% sales growth in constant currency

Group sales increased by 19% (17% in constant currency) to €16,894 million (H1/2016: €14,218 million). Organic sales growth was 6%5. Positive currency translation effects (2%) were mainly related to the appreciation of the U.S. dollar against the Euro. Acquisitions and the agreement with the United States Departments of Veterans Affairs and Justice at Fresenius Medical Care (“VA agreement”) contributed 11%. In Q2/2017, Group sales increased by 18% (17% in constant currency) to €8,532 million (Q2/2016: €7,203 million). Organic sales growth was 5%. Acquisitions contributed 12% while divestitures had no meaningful impact on sales.

1 Before transaction costs of ~€50 million for the acquisitions of Akorn, Inc. and Merck KGaA’s biosimilars business2 Before expected expenditures for the further development of Merck KGaA’s biosimilars business of ~€50 million (expected closing Q3/17)3 Net income attributable to shareholders of Fresenius SE & Co. KGaA4 Calculated at expected FY average exchange rates for both net debt and EBITDA; before transaction costs of ~€50 million; excluding further potential acquisitions5 Excluding effects of VA agreementFor a detailed overview of special items please see the reconciliation tables on page 15 in the PDF document.

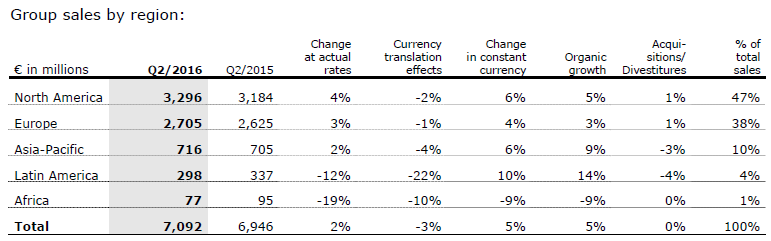

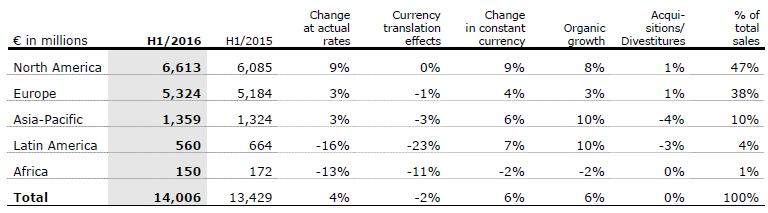

Group sales by region:

23% net income2 growth in constant currency

Group EBITDA3 increased by 20% (18% in constant currency) to €3,098 million (H1/2016: €2,586 million). Group EBIT3 increased by 20% (19% in constant currency) to €2,393 million (H1/2016: €1,987 million). The EBIT margin3 increased to 14.2% (H1/2016: 14.0%). In Q2/2017, Group EBIT3 increased by 14% (13% in constant currency) to €1,177 million (Q2/2016: €1,028 million), with an EBIT margin3 of 13.8% (Q2/2016: 14.3%).

Group net interest reached -€326 million3 (H1/2016: -€291 million), mainly due to the financing of the Quirónsalud acquisition.

The Group tax rate increased to 28.5%3 (H1/2016: 28.3%), mainly driven by the higher proportion of U.S. pre-tax income, primarily due to the VA agreement. In Q2/2017, the Group tax rate was 27.9%3 (Q2/2016: 28.2%).

1 Including effects of VA agreement2 Net income attributable to shareholders of Fresenius SE & Co. KGaA; before special items3 Before special itemsFor a detailed overview of special items please see the reconciliation tables on page 15 in the PDF document.

Noncontrolling interest increased to €562 million (H1/2016: €480 million), of which 96% was attributable to the noncontrolling interest in Fresenius Medical Care.

Group net income1 increased by 24% (23% in constant currency) to €916 million (H1/2016: €736 million). The VA agreement increased net income1 growth by 2%-points. Earnings per share1 increased by 22% (21% in constant currency) to €1.65 (H1/2016: €1.35). In Q2/2017, Group net income1 increased by 21% (21% in constant currency) to €459 million (Q2/2016: €378 million). Earnings per share1 increased by 19% (19% in constant currency) to €0.82 (Q2/2016: €0.70).

1 Net income attributable to shareholders of Fresenius SE & Co. KGaA; before special itemsFor a detailed overview of special items please see the reconciliation tables on page 15 in the PDF document.

Continued investment in growth

Spending on property, plant and equipment was €709 million (H1/2016: €674 million), primarily for the modernization and expansion of dialysis clinics, production facilities as well as hospitals and day clinics. Total acquisition spending of €6,421 million (H1/2016: €505 million) was mainly related to the acquisition of Quirónsalud.

Strong operating cash flow

Operating cash flow increased by 26% to €1,683 million (H1/2016: €1,333 million), mainly driven by the excellent development at Fresenius Medical Care and Fresenius Kabi. The cash flow margin increased to 10.0% (H1/2016: 9.4%). Operating cash flow in Q2/2017 increased by 21% to €1,207 million (Q2/2016: €997 million), with a margin of 14.1% (Q2/2016: 13.8%). As expected, the operating cash flow of Fresenius Medical Care improved considerably in Q2/2017.

Free cash flow before acquisitions and dividends increased by 54% to €998 million (H1/2016: €649 million). Free cash flow after acquisitions and dividends was -€5,645 million

(H1/2016: -€207 million).

Solid balance sheet structure

The Group’s total assets increased by 13% (18% in constant currency) to €52,897 million (Dec. 31, 2016: €46,697 million), mainly due to the acquisition of Quirónsalud. Current assets grew by 9% (14% in constant currency) to €12,799 million (Dec. 31, 2016: €11,744 million). Non-current assets increased by 15% (19% in constant currency) to €40,098 million (Dec. 31, 2016: € 34,953 million).

Total shareholders’ equity grew by 1% (6% in constant currency) to €21,020 million (Dec. 31, 2016: €20,849 million). The equity ratio was 39.7% (Dec. 31, 2016: 44.6%).

Group debt increased by 35% (39% in constant currency) to €19,910 million (Dec. 31, 2016: € 14,780 million), mainly driven by the acquisition financing of Quirónsalud. As of June 30, 2017, the net debt/EBITDA ratio was 3.001 (Dec. 31, 2016: 2.331; pro forma Quirónsalud 3.091).

1 Net debt and EBITDA at LTM average exchange rates; before special itemsFor a detailed overview of special items please see the reconciliation tables on page 15 in the PDF document.

Business Segments

Fresenius Medical Care

Fresenius Medical Care is the world's largest provider of products and services for individuals with chronic kidney failure. As of June 30, 2017, Fresenius Medical Care was treating 315,305 patients in 3,690 dialysis clinics. Along with its core business, the company seeks to expand the range of medical services in the field of care coordination.

- 9% sales growth in constant currency in Q2

- 46% operating cash flow growth in Q2

- 2017 outlook confirmed

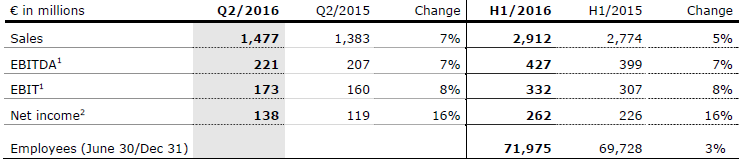

Sales increased by 14% (11% in constant currency, 7% organic) to €9,019 million (H1/2016: €7,942 million). Acquisitions/divestitures and the VA agreement contributed 4% in total. In Q2/2017, sales increased by 11% (9% in constant currency, 6% organic) to €4,471 million (Q2/2016: €4,026 million).

Health Care Services sales (dialysis services and care coordination) increased by 15% (11% in constant currency) to €7,418 million (H1/2016: €6,472 million). Product sales increased by 9% (7% in constant currency) to €1,601 million (H1/2016: €1,470 million).

In North America, sales increased by 14% to €6,600 million (H1/2016: €5,778 million). Health Care Services sales grew by 15% to €6,182 million (H1/2016: €5,383 million). Product sales increased by 6% to €418 million (H1/2016: €395 million).

Sales outside North America increased by 12% (10% in constant currency) to €2,410 million (H1/2016: €2,156 million). Health Care Services sales increased by 14% (11% in constant currency) to €1,236 million (H1/2016: €1,089 million). Product sales increased by 10% (8% in constant currency) to €1,174 million (H1/2016: €1,068 million).

EBIT increased by 16% (13% in constant currency) to €1,235 million (H1/2016: €1,068 million). The EBIT margin was 13.7% (H1/2016: 13.5%). Excluding the VA agreement EBIT increased by 7% (5% in constant currency). In Q2/2017, EBIT increased by 2% (stable in constant currency) to €584 million (Q2/2016: €571 million). The EBIT margin was 13.0% (Q2/2016: 14.2%).

Net income1 increased by 21% (19% in constant currency) to €577 million (H1/2016: €477 million). Excluding the VA agreement net income1 increased by 10% (8% in constant currency). In Q2/2017, net income1 grew by 2% (stable in constant currency) to €269 million (Q2/2016: €264 million).

Operating cash flow increased by 37% to €1,052 million (H1/2016: €767 million). The cash flow margin increased to 11.7% (H1/2016: 9.7%). In Q2/2017, operating cash flow increased by 46% to €882 million (Q2/2016: €604 million) with a cash flow margin of 19.7% (Q2/2016: 15.0%).

Fresenius Medical Care confirms its outlook for 2017. The company expects sales to grow by 8% to 10%2 in constant currency. Net income1,2 is expected to increase by 7% to 9% in constant currency.

1 Net income attributable to shareholders of Fresenius Medical Care AG & Co. KGaA2 Excluding effects of VA agreement

For further information, please see Fresenius Medical Care’s Investor News at www.freseniusmedicalcare.com.

Fresenius Kabi

Fresenius Kabi offers intravenously administered generic drugs, clinical nutrition and infusion therapies for seriously and chronically ill patients in the hospital and outpatient environments. The company is also a leading supplier of medical devices and transfusion technology products.

- 7% organic sales growth in Q2; positive contributions from all regions

- 9% constant currency EBIT growth in Q2

- 2017 outlook confirmed

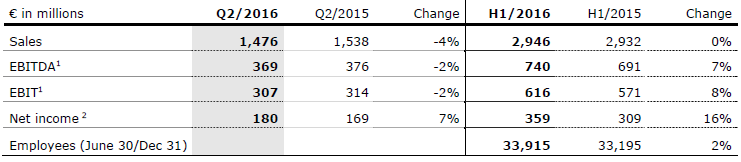

Sales increased by 9% (7% in constant currency, 7% organic) to €3,202 million (H1/2016: €2,946 million). Acquisitions/divestitures had no meaningful impact on sales. In Q2/2017, sales increased by 8% (7% in constant currency and organic) to €1,598 million (Q2/2016: €1,476 million).

Sales in Europe increased by 5% (6% organic) to €1,097 million (H1/2016: €1,048 million). Currency translation effects had no meaningful impact. In Q2/2017, sales increased by 3% (4% organic) to €553 million (Q2/2016: €536 million).

Sales in North America increased by 9% (6% organic) to €1,187 million (H1/2016: €1,086 million). In Q2/2017, sales increased by 11% (9% organic) to €568 million (Q2/2016: €510 million).

Sales in Asia-Pacific increased by 10% (10% organic) to €582 million (H1/2016: €531 million). In Q2/2017, sales increased by 9% (10% organic) to €302 million (Q2/2016: €277 million).

Sales in Latin America/Africa increased by 20% (11% organic) to €336 million (H1/2016: €281 million), mainly due to inflation-driven price increases. In Q2/2017, sales increased by 14% (8% organic) to €175 million (Q2/2016: €153 million).

EBIT1 increased by 7% (6% in constant currency) to €622 million (H1/2016: €582 million). The EBIT margin1 was 19.4% (H1/2016: 19.8%). In Q2/2017, EBIT1 increased by 11% (9% in constant currency) to €309 million (Q2/2016: €279 million). The EBIT margin1 increased to 19.3% (Q2/2016: 18.9%).

Net income2 increased by 13% (11% in constant currency) to €379 million (H1/2016: €336 million). In Q2/2017, net income2 increased by 15% (13% in constant currency) to €188 million (Q2/2016: €163 million).

Operating cash flow increased by 17% to €395 million (H1/2016: €339 million) driven by strong operating results and improved net working capital. The margin increased to 12.3% (H1/2016: 11.5%). In Q2/2017, operating cash flow was €203 million (Q2/2016: €212 million). The cash flow margin was 12.7% (Q2/2016: 14.4%).

Fresenius Kabi confirms its outlook for 2017 and expects 5% to 7% organic sales growth and EBIT growth in constant currency of 6% to 8%3,4.

1 Before special items2 Net income attributable to shareholders of Fresenius SE & Co. KGaA; before special items3 Before transaction costs of ~€50 million for the acquisitions of Akorn, Inc. and Merck KGaA’s biosimilars business4 Before expected expenditures for the further development of Merck KGaA’s biosimilars business of ~€50 million (expected closing Q3/17)For a detailed overview of special items please see the reconciliation tables on page 15 in the PDF document.

Fresenius Helios

Fresenius Helios is Europe's leading private hospital operator. The company comprises HELIOS Kliniken in Germany and Quirónsalud in Spain. HELIOS Kliniken operates 112 hospitals, thereof 88 acute care clinics and 24 post-acute care clinics, and treats more than 5.2 million patients annually. Quirónsalud operates 44 hospitals, 44 outpatient centers and around 300 occupational risk prevention centers, and treats approximately 9.7 million patiens per year.

- 52% sales growth (2% excluding Quirónsalud) in Q2

- 63% EBIT increase (3% excluding Quirónsalud) in Q2

- 2017 outlook confirmed

Sales increased by 46% (4% organic) to €4,256 million (H1/2016: €2,912 million). Acquisitions, mainly Quirónsalud, increased sales by 42%. In Q2/2017, sales increased by 52% (2% organic) to €2,238 million (Q2/2016: €1,477 million).

Sales of HELIOS Kliniken2 increased by 4% (4% organic) to €3,038 million (H1/2016: €2,912 million). In Q2/2017, sales increased by 2% (2% organic) to €1,510 million (Q2/2016: €1,477 million). Quirónsalud is consolidated since February 1, 2017 and generated sales of €1,218 million (thereof €728 million in Q2/2017).

EBIT grew by 62% to €537 million (H1/2016: €332 million). The EBIT margin increased to 12.6% (H1/2016: 11.4%). In Q2/2017, EBIT increased by 63% to €282 million (Q2/2016: €173 million). The EBIT margin increased to 12.6% (Q2/2016: 11.7%).

EBIT of HELIOS Kliniken2 increased by 8% to €359 million with a margin of 11.8% (H1/2016: 11.4%). In Q2/2017, EBIT increased by 3% to €178 million (Q2/2016: €173 million). EBIT of Quirónsalud was €178 million (thereof €104 million in Q2/2017) with a margin of 14.6%.

Net income1 increased by 42% to €373 million (H1/2016: €262 million). In Q2/2017, net income1 increased by 39% to €192 million (Q2/2016: €138 million).

1 Net income attributable to shareholders of Fresenius SE & Co. KGaA2 HELIOS Kliniken Germany, excluding Quirónsalud

Operating cash flow increased by 32% to €304 million (H1/2016: €230 million) driven by the first-time consolidation of Quirónsalud and good operating results. The margin was 7.1% (H1/2016: 7.9%).

Fresenius Helios confirms its outlook for 2017 and projects organic sales growth of 3% to 5%1 and sales of ~€8.6 billion (thereof Quirónsalud: ~€2.5 billion2). EBIT is expected to increase to €1,020 to €1,070 million (thereof Quirónsalud: €300 to 320 million2).

1 HELIOS Kliniken Germany, excluding Quirónsalud2 Quirónsalud consolidated for 11 months

Fresenius Vamed

Fresenius Vamed manages projects and provides services for hospitals and other health care facilities worldwide. The portfolio ranges along the entire value chain: from project development, planning, and turnkey construction, via maintenance and technical management, to total operational management.

- 2% sales growth in Q2 driven by service business

- Project business with strong order intake of €412 million in H1

- 2017 outlook confirmed

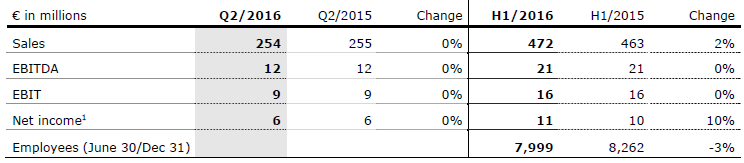

Sales increased by 2% (2% organic) to €481 million (H1/2016: €472 million). Sales in the project business decreased by 6% to €184 million (H1/2016: €195 million). Sales in the service business grew by 7% to €297 million (H1/2016: €277 million). In Q2/2017, sales increased by 2% (1% organic) to €258 million (Q2/2016: €254 million).

EBIT increased by 6% to €17 million (H1/2016: €16 million). The EBIT margin increased to 3.5% (H1/2016: 3.4%). In Q2/2017, EBIT increased by 22% to €11 million (Q2/2016: €9 million) with an EBIT margin of 4.3%.

Net income1 remained unchanged at €11 million. In Q2/2017, net income1 increased by 17% to €7 million (Q2/2016: €6 million).

Order intake reached a strong €412 million, but could not quite match the previous year’s excellent level (H1/2016: €465 million). As of June 30, 2017, order backlog grew to an all-time high of €2,188 million (December 31, 2016: €1,961 million).

Fresenius Vamed confirms its outlook for 2017 and expects both organic sales growth and EBIT growth in the range of 5% to 10%.

1 Net income attributable to shareholders of VAMED AG

Conference Call

As part of the publication of the results for the first half of 2017, a conference call will be held on August 1, 2017 at 2 p.m. CEDT (8 a.m. EDT). All investors are cordially invited to follow the conference call in a live broadcast over the Internet at www.fresenius.com/investors. Following the call, a replay will be available on our website.

For additional information on the performance indicators, please refer to our website www.fresenius.com/alternative-performance-measures.

This release contains forward-looking statements that are subject to various risks and uncertainties. Future results could differ materially from those described in these forward-looking statements due to certain factors, e.g. changes in business, economic and competitive conditions, regulatory reforms, results of clinical trials, foreign exchange rate fluctuations, uncertainties in litigation or investigative proceedings, and the availability of financing. Fresenius does not undertake any responsibility to update the forward-looking statements in this release.

Q1/2017:

• Sales: €8.4 billion (+19%, +17% in constant currency)

• EBIT: €1,216 million (+27%, +25% in constant currency)

• Net income1 : €457 million (+28%, +26% in constant currency)

1 Net income attributable to shareholders of Fresenius SE & Co. KGaA

Stephan Sturm, CEO of Fresenius, said: “Fresenius made an excellent start in 2017. All four business segments developed very well in the first quarter and continue to have healthy growth prospects. That makes us all the more optimistic as we look ahead. From this position of strength, and bolstered by strategically important acquisitions, we are building an even stronger foundation for our long-term success.”

2017 Group earnings guidance raised1,2,3

Based on the Group’s strong Q1 results and ongoing bright prospects for the remainder of the year, Fresenius raises its 2017 Group earnings guidance published in February 2017. Group net income3 on a like-for-like basis, i.e. before effects of the recently announced acquisitions at Fresenius Kabi, is now expected to grow by 19% to 21% in constant currency (previously: 17% to 20%).

Including expenditures for the further development of Merck KGaA’s biosimilars business, which is expected to be acquired in the second half of 2017, Fresenius projects net income3 growth in constant currency within the previous range of 17% to 20%.

Fresenius confirms its sales guidance. Group sales are expected to increase by 15% to 17% in constant currency.

Pro forma the acquisitions of Akorn and Merck KGaA’s biosimilars business, the net debt/EBITDA4ratio is expected to be approximately 3.3 at the end of 2017.

17% sales growth in constant currency

Group sales increased by 19% (17% in constant currency) to €8,362 million (Q1/2016: €7,015 million). Organic sales growth was 7%5. Positive currency translation effects (2%) were mainly related to the appreciation of the US-Dollar against the Euro. Divestitures had no impact on sales. Acquisitions and the €100 million agreement with the United States Departments of Veterans Affairs and Justice at Fresenius Medical Care North America (“VA agreement”) contributed 10%.

1 Before transaction costs of ~€50 million for the acquisitions of Akorn, Inc. and Merck KGaA’s biosimilars business2 Before expected expenditures for the further development of Merck KGaA’s biosimilars business of ~€50 million (expected closing H2/17)3 Net income attributable to shareholders of Fresenius SE & Co. KGaA4 Calculated at expected FY average exchange rates for both net debt and EBITDA; before transaction costs of ~€50 million; excluding further potential acquisitions5 Excluding effects of VA-agreement

Group sales by region:

26% net income1 growth in constant currency

Group EBITDA increased by 26% (23% in constant currency) to €1,560 million (Q1/2016: €1,241 million). Group EBIT increased by 27% (25% in constant currency) to €1,216 million (Q1/2016: €959 million). The EBIT margin increased to 14.5% (Q1/2016: 13.7%).

Group net interest increased to -€157 million (Q1/2016: -€152 million), mainly due to the financing of the Quirónsalud acquisition.

The Group tax rate increased to 29.1% (Q1/2016: 28.4%), mainly driven by the higher proportion of U.S. pre-tax income, primarily due to the VA-agreement.

Noncontrolling interest increased to €294 million (Q1/2016: €220 million), of which 96% was attributable to the noncontrolling interest in Fresenius Medical Care.

Group net income1 increased by 28% (26% in constant currency) to €457 million (Q1/2016: €358 million). The VA-agreement increased net income1 by €18 million or 5%-points. Earnings per share1 increased by 28% (25% in constant currency) to €0.83 (Q1/2016: €0.65).

1 Net income attributable to shareholders of Fresenius SE & Co. KGaA

Continued investment in growth

Spending on property, plant and equipment was €328 million (Q1/2016: €315 million), primarily for the modernization and expansion of dialysis clinics, production facilities and hospitals. Total acquisition spending of €6,083 million (Q1/2016: €204 million) was mainly related to the acquisition of Quirónsalud.

Strong operating cash flow

Operating cash flow increased by 42% to €476 million (Q1/2016: €336 million), mainly driven by the excellent development at Fresenius Kabi and Fresenius Helios. The cash flow margin was 5.7% (Q1/2016: 4.8%).

Free cash flow before acquisitions and dividends increased to €148 million (Q1/2016: €2 million). Free cash flow after acquisitions and dividends was -€5,393 million

(Q1/2016: -€241 million).

Solid balance sheet structure

The Group’s total assets increased by 17% (17% in constant currency) to €54,418 million (Dec. 31, 2016: €46,697 million), mainly due to the acquisition of Quirónsalud. Current assets grew by 11% (12% in constant currency) to €13,077 million (Dec. 31, 2016: €11,744 million). Non-current assets increased by 18% (19% in constant currency) to €41,341 million (Dec. 31, 2016: €?34,953 million).

Total shareholders’ equity grew by 5% (6% in constant currency) to €21,921 million (Dec. 31, 2016: €20,849 million). The equity ratio was 40.3% (Dec. 31, 2016: 44.6%).

Group debt increased by 37% (37% in constant currency) to €20,210 million (Dec. 31, 2016: €?14,780 million), mainly driven by the acquisition financing of Quirónsalud. As of March 31, 2017, the net debt/EBITDA ratio was 2.981,3 (Dec. 31, 2016: 2.331,3/3.091,2,3).

1 Net debt and EBITDA at LTM average exchange rates2 Pro forma Quirónsalud3 Pro forma acquisitions

Increased number of employees

As of March 31, 2017, the number of employees increased by 13% to 263,957 (Dec. 31, 2016: 232,873).

Business segments

Fresenius Medical Care

Fresenius Medical Care is the world's largest provider of products and services for individuals with chronic kidney failure. As of March 31, 2017, Fresenius Medical Care was treating 310,473 patients in 3,654 dialysis clinics. Along with its core business, the company seeks to expand the range of medical services in the field of care coordination.

• 12% sales growth in constant currency (10% excluding the VA-agreement)

• 41% net income growth1 in constant currency (14% excluding the VA-agreement)

• 2017 outlook confirmed

1 Net income attributable to shareholders of Fresenius Medical Care AG & Co. KGaA

Sales increased by 16% (12% in constant currency) to €4,548 million (Q1/2016: €3,916 million). Organic sales growth was 8%. Acquisitions/divestitures and the VA agreement contributed 4% in total.

Health Care services sales (dialysis services and care coordination) increased by 18% (14% in constant currency) to €3,769 million (Q1/2016: €3,199 million). Product sales increased by 8% (6% in constant currency) to €779 million (Q1/2016: €718 million).

In North America, sales increased by 18% (14% excluding the VA-agreement) to €3,375 million (Q1/2016: €2,862 million). Health Care services sales grew by 19% to €3,165 million (Q1/2016: €2,670 million). Product sales increased by 9% to €210 million (Q1/2016: €192 million).

Sales outside North America increased by 11% (8% in constant currency) to €1,169 million (Q1/2016: €1,051 million). Health Care services sales increased by 14% (10% in constant currency) to €604 million (Q1/2016: €528 million). Product sales increased by 8% (6% in constant currency) to €564 million (Q1/2016: €523 million).

EBIT increased by 31% (28% in constant currency) to €651 million (Q1/2016: €497 million). The EBIT margin was 14.3% (Q1/2016: 12.7%). Excluding the VA-agreement (€99 million) EBIT increased by 11% (8% in constant currency).

Net income1 increased by 45% (41% in constant currency) to €308 million (Q1/2016: €213 million). Excluding the VA-agreement (€59 million) net income1 increased by 17% (14% in constant currency).

Operating cash flow increased by 4% to €170 million (Q1/2016: €163 million). The cash flow margin was 3.7% (Q1/2016: 4.2%). The VA-agreement partially offset the impact of seasonality in invoicing at Fresenius Medical Care in North America. Fresenius Medical Care expects that this timing effect will have no meaningful impact on the full year 2017.

Fresenius Medical Care confirms its outlook for 2017. The company expects sales to grow by 8% to 10%2 in constant currency. Net income1,2 is expected to increase by 7% to 9% in constant currency.

1 Net income attributable to shareholders of Fresenius Medical Care AG & Co. KGaA2 Excluding effects of VA-agreementFor further information, please see Fresenius Medical Care’s press release at www.freseniusmedicalcare.com.

Fresenius Kabi

Fresenius Kabi offers intravenously administered generic drugs, clinical nutrition and infusion therapies for seriously and chronically ill patients in the hospital and outpatient environments. The company is also a leading supplier of medical devices and transfusion technology products.

• 7% organic sales growth; positive contributions from all regions

• 2% constant currency EBIT growth despite very strong PY quarter

• 2017 outlook raised: 6% to 8%2,3, EBIT growth in constant currency expected

Sales increased by 9% (organic growth: 7%) to €1,604 million (Q1/2016: €1,470 million). Positive currency translation effects (2%) were mainly related to the appreciation of the US-Dollar against the Euro. Acquisitions/divestitures had no impact on sales.

Sales in Europe increased by 6% (organic growth: 7%) to €544 million (Q1/2016: €512 million). Currency translation effects reduced sales by 1%.

Sales in North America increased by 7% (organic growth: 4%) to €619 million (Q1/2016: €576 million).

Sales in Asia-Pacific increased by 10% (organic growth: 10%) to €280 million (Q1/2016: €254 million).

Sales in Latin America/Africa increased by 26% to €161 million (Q1/2016: €128 million). Organic sales growth was 14%, mainly due to inflation-driven price increases.

EBIT increased by 3% (2% in constant currency) to €313 million (Q1/2016: €303 million). The EBIT margin was 19.5% (Q1/2016: 20.6%).

Net income1 increased by 10% (9% in constant currency) to €191 million (Q1/2016: €173 million).

Operating cash flow increased by 51% to €192 million (Q1/2016: €127 million) driven by strong operating results and improved net working capital. The margin increased to 12.0% (Q1/2016: 8.6%).

Fresenius Kabi raises its outlook for 2017 and now expects EBIT growth in constant currency of 6% to 8%2,3, (previously 5% to 7%). The company confirms its guidance of 5% to 7% organic sales growth.

1 Net income attributable to shareholders of Fresenius SE & Co. KGaA2 Before transaction costs of ~€50 million for the acquisitions of Akorn, Inc. and Merck KGaA’s biosimilars business3 Before expected expenditures for the further development of Merck KGaA’s biosimilars business of ~€50 million (expected closing H2/17)

Fresenius Helios

Fresenius Helios is Europe's leading private hospital operator. The company comprises HELIOS Kliniken in Germany and Quirónsalud in Spain. HELIOS Kliniken operates 112 hospitals, thereof 88 acute care clinics and 24 post-acute care clinics, and treats more than 5.2 million patients annually. Quirónsalud operates 44 hospitals, 43 outpatient centers and around 300 occupational risk prevention centers, and treats approximately 9.7 million patiens per year.

• 5% organic sales growth

• 60% EBIT increase (14% excluding Quirónsalud)

• 2017 outlook confirmed

Sales increased by 41% (organic growth: 5%) to €2,018 million (Q1/2016: €1,435 million). Acquisitions, mainly Quirónsalud, increased sales by 36%. Quirónsalud is consolidated since February 1, 2017. Sales of Quirónsalud were €490 million in February and March 2017.

Sales of HELIOS Kliniken2 increased by 6% (organic growth: 5%) to €1,528 million.

EBIT grew by 60% to €255 million (Q1/2016: €159 million). The EBIT margin increased to 12.6% (Q1/2016: 11.1%).

EBIT of HELIOS Kliniken2 increased by 14% to €181 million with a margin of 11.8% (Q1/2016: 11.1%). EBIT of Quirónsalud was €74 million with a margin of 15.1%.

Net income1 increased by 46% to €181 million (Q1/2016: €124 million).

1 Net income attributable to shareholders of Fresenius SE & Co. KGaA2 HELIOS Kliniken Germany, excluding Quirónsalud

Operating cash flow increased by 179% to €184 million (Q1/2016: €66 million) driven by the first time consolidation of Quirónsalud and good operating results. The margin increased to 9.1% (Q1/2016: 4.6%).

Fresenius Helios confirms its outlook for 2017 and projects organic sales growth of 3% to 5%1 and sales of ~€8.6 billion (thereof Quirónsalud: ~€2.5 billion2). EBIT is expected to increase to €1,020 to €1,070 million (thereof Quirónsalud: €300 to 320 million2).

1 HELIOS Kliniken Germany, excluding Quirónsalud2 Quirónsalud consolidated for 11 months

Fresenius Vamed

Fresenius Vamed manages projects and provides services for hospitals and other health care facilities worldwide. The portfolio ranges along the entire value chain: from project development, planning, and turnkey construction, via maintenance and technical management, to total operational management.

• 2% organic sales growth driven by service business

• Project business with strong order intake of €220 million

• 2017 outlook confirmed

Sales increased by 2% (organic growth: 2%) to €223 million (Q1/2016: €218 million). Sales in the project business decreased by 9% to €77 million (Q1/2016: €85 million). Sales in the service business grew by 10% to €146 million (Q1/2016: €133 million).

EBIT decreased by 14% to €6 million (Q1/2016: €7 million). The EBIT margin decreased to 2.7% (Q1/2016: 3.2%).

Net income1 decreased by 20% to €4 million (Q1/2016: €5 million).

Order intake reached a strong €220 million, could not quite match the previous year’s excellent level (Q1/2016: €237 million). As of March 31, 2017, order backlog grew to a record €2,104 million (December 31, 2016: €1,961 million).

Fresenius Vamed confirms its outlook for 2017 and expects both organic sales growth and EBIT growth in the range of 5% to 10%.

1 Net income attributable to shareholders of VAMED AG

Conference Call

As part of the publication of the results for the first quarter of 2017, a conference call will be held on May 3, 2017 at 2 p.m. CEDT (8 a.m. EDT). All investors are cordially invited to follow the conference call in a live broadcast over the Internet at www.fresenius.com/investors. Following the call, a replay will be available on our website.

# # #

For additional information on the performance indicators used please refer to our website https://www.fresenius.com/alternative-performance-measures.

This release contains forward-looking statements that are subject to various risks and uncertainties. Future results could differ materially from those described in these forward-looking statements due to certain factors, e.g. changes in business, economic and competitive conditions, regulatory reforms, results of clinical trials, foreign exchange rate fluctuations, uncertainties in litigation or investigative proceedings, and the availability of financing. Fresenius does not undertake any responsibility to update the forward-looking statements in this release.

If no timeframe is specified, information refers to fiscal year 2016.

Fiscal year 2016:

- Sales: €29.1 billion

(+5%, +6% in constant currency) - EBIT1: €4,327 million

(+9%, +10% in constant currency) - Net income1,2:€1,593 million

(+12%, +13% in constant currency) - Dividend proposal: +13% to €0.62 per share

Q4/2016:

- Sales: €7.7 billion

(+7%, +6% in constant currency) - EBIT1 €1,235 million

(+11%, +11% in constant currency) - Net income1,2 €439 million

(+6%, +7% in constant currency)

Group guidance 20173:

- Sales growth of 15% to 17% in constant currency

- Net income2 growth of 17% to 20% in constant currency

Targets 20203:

- Group sales4: between €43 billion and €47 billion

- Group net income2,4: between €2.4 billion and €2.7 billion

1 2015 before special items2 Net income attributable to shareholders of Fresenius SE & Co. KGaA3 Guidance according to IFRS; for a detailed overview of 2016 IFRS figures please see p. 14 of the pdf file4 At comparable exchange rates; includes small and mid-size acquisitions; at current IFRS-rules

Stephan Sturm, CEO of Fresenius, said: “Fresenius had another truly outstanding year in 2016, setting new sales and earnings records. All four business segments again developed very successfully. The company’s prospects are excellent, and in the coming years Fresenius is targeting continued, dynamic growth. We never forget that patients are at the center of everything we do. Providing them with high-quality yet affordable healthcare around the world is the key to our business success."

Positive Group guidance for 20171

For 2017, Fresenius projects sales growth of 15% to 17% in constant currency. Net income2 is expected to grow by 17% to 20% in constant currency.

The net debt/EBITDA3 ratio is expected to be within the bottom half of Fresenius’ self-imposed target range of 2.5 to 3.0 at the end of 2017.

New ambitious targets for 20201,4

For 2020, Group sales are expected to reach €43 billion to €47 billion. Calculated on the basis of reported 2016 IFRS sales (€29,471 million) and the mid-point of the target range (€45 billion), this corresponds to a compounded annual growth rate (CAGR) of 11.2%. Based on the very strong guidance for 2017, this would result in a 2018-2020 CAGR of 8.7%.5

Group net income2 is expected to increase to €2.4 billion to €2.7 billion. Calculated on the basis of reported 2016 IFRS net income (€1,560 million) and the mid-point of the target range (€2,550 million) this corresponds to a CAGR of 13.1%. Based on the very strong guidance for 2017, this would result in a 2018-2020 CAGR of 10.5%.6

24th consecutive dividend increase proposed

Based on the strong financial results, the Management Board will propose to the Supervisory Board a dividend increase of 13% to €0.62 per share (2015: €0.55). The expected total dividend distribution is €343 million.

1 Guidance according to IFRS; for a detailed overview of 2016 IFRS figures please see p. 14of the pdf file2 Net income attributable to shareholders of Fresenius SE & Co. KGaA3 Calculated at expected annual average exchange rates, for both net debt and EBITDA; without large unannounced acquisitions4 At comparable exchange rates; including small and mid-size acquisitions; at current IFRS rules5 Based on the mid-point of the 2017 sales guidance, adjusted for current exchange rates (~€35 bn), and the mid-point of the 2020 sales target range (€45 bn)6 Based on the mid-point of the 2017 net income guidance, adjusted for current exchange rates (~€1,890 m), and the mid-point of the 2020 net income target range (€2,550 m)

6% sales growth in constant currency

Group sales increased by 5% (6% in constant currency) to €29,083 million (2015: €27,626 million). Organic sales growth was 6%. Acquisitions contributed 1% and divestitures reduced sales by 1%. Slightly negative currency translation effects (1%) were mainly driven by the devaluation of Latin American currencies and the Chinese yuan against the Euro. In Q4/2016, Group sales increased by 7% (6% in constant currency) to €7,738 million (Q4/2015: €7,257 million). Organic sales growth was 5%. Acquisitions contributed 1%, while divestitures had no major impact on sales.

Group sales by region:

13% net income1,2 growth in constant currency

Group EBITDA2 increased by 8% (9% in constant currency) to €5,500 million (2015: €5,073 million). Group EBIT2 increased by 9% (10% in constant currency) to €4,327 million (2015: €3,958 million). The EBIT margin2 increased to 14.9% (2015: 14.3%).

In Q4/2016, Group EBIT2 increased by 11% (11% in constant currency) to €1,235 million (Q4/2015: €1,109 million), the EBIT margin2 improved to 16.0% (Q4/2015: 15.3%).

Group net interest decreased to -€582 million (2015: -€613 million), mainly due to favourable financing terms and interest savings on lower average debt. In Q4/2016, Group net interest increased to -€149 million (Q4/2015: -€137 million) mainly due to the bridge financing for the Quirónsalud acquisition.

The Group tax rate2 decreased to 28.1% (2015: 29.4%). The decrease is mainly due to released tax liabililities at Fresenius Medical Care in Q3/2016. In Q4/2016, the Group tax rate also decreased to 28.1% (Q4/2015: 28.8%).

Noncontrolling interest was €1,101 million (2015: €939 million), of which 96% was attributable to the noncontrolling interest in Fresenius Medical Care.

Group net income1,2 increased by 12% (13% in constant currency) to €1,593 million (2015: €1,423 million). Earnings per share1,2 increased by 12% (13% in constant currency) to €2.92 (2015: €2.61). In Q4/2016, Group net income1,2 increased by 6% (7% in constant currency) to €439 million (Q4/2015: €414 million). Earnings per share1,2 increased by 7% (8% in constant currency) to €0.81 (Q4/2015: €0.75).

Continued investment in growth

Spending on property, plant and equipment was €1,621 million (2015: €1,512 million), primarily for the modernization and expansion of dialysis clinics, production facilities and hospitals. This corresponds to 5.6% of sales.

Total acquisition spending increased to €926 million (2015: €517 million), mainly related to acquisitions at Fresenius Medical Care.

1 Net income attributable to shareholders of Fresenius SE & Co. KGaA2 2015 before special items

For a detailed overview of special items please see the reconciliation tables on pages 17-18 of the pdf file.

Excellent cash flow development

Operating cash flow increased by 7% to €3,574 million (2015: €3,327 million) with a margin of 12.3% (2015: 12.0%). The excellent cash flow was driven by a strong cash flow generation at Fresenius Medical Care and especially the record cash flow at Fresenius Kabi. Operating cash flow in Q4/2016 increased by 12% to €1,315 million (Q4/2015: €1,176 million) with a margin of 17.0% (Q4/2015: 16.2%).

Free cash flow before acquisitions and dividends increased by 6% to €1,971 million (2015: €1,865 million), with a margin of 6.8% (2015: 6.8%). Free cash flow after acquisitions and dividends was €748 million (2015: €1,194 million).

Solid balance sheet structure

The Group’s total assets increased by 8% (6% in constant currency) to €46,447 million (Dec. 31, 2015: €42,959 million), driven by its growing scale of operations. Current assets grew by 13% (11% in constant currency) to €11,799 million (Dec. 31, 2015: €10,479 million). Non-current assets increased by 7% (5% in constant currency) to €34,648 million (Dec. 31, 2015: € 32,480 million).

Total shareholders’ equity increased by 13% (11% in constant currency) to €20,420 million (Dec. 31, 2015: €18,003 million). The equity ratio increased to 44.0% (Dec. 31, 2015: 41.9%).

Group debt remained nearly unchanged (-2% in constant currency) at €14,780 million (Dec. 31, 2015: € 14,769 million). Group net debt decreased by 4% (-5% in constant currency) to € 13,201 million (Dec. 31, 2015: € 13,725 million). As of December 31, 2016, the net debt/EBITDA ratio was 2.341 (December 31, 2015: 2.682). EBITDA growth and net debt reduction made an about equal contribution to this substantial improvement of the ratio.

Increased number of employees

As of December 31, 2016, the number of employees increased by 5% to 232,873 (Dec. 31, 2015: 222,305).

1 At LTM average exchange rates for both net debt and EBITDA; pro forma acquisitions2 Before special items; at LTM average exchange rates for both net debt and EBITDA

For a detailed overview of special items please see the reconciliation tables on pages 17-18 of the pdf file.

Business Segments

Fresenius Medical Care

Fresenius Medical Care is the world's largest provider of products and services for individuals with renal diseases. As of December 31, 2016, Fresenius Medical Care was treating 308,471 patients in 3,624 dialysis clinics. Along with its core business, the company seeks to expand the range of medical services in the field of care coordination.

- 7% sales growth, 16% net income growth1,2

- Health Care services with positive growth momentum (sales +8%)

- 2017 outlook3: 8% to 10% sales growth in constant currency and 7 to 9% net income growth1,5 in constant currency expected

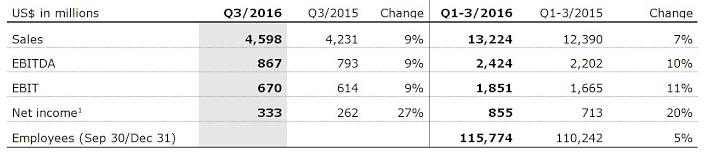

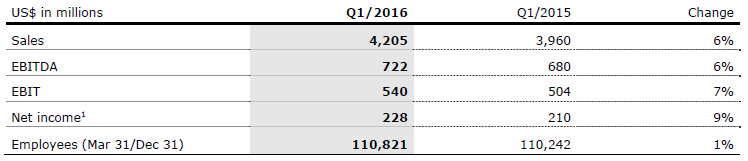

Sales increased by 7% (8% in constant currency) to US$17,911 million (2015: US$16,738 million). Organic sales growth was 7%. Acquisitions and divestitures increased sales by 1%. Currency translation effects reduced sales by 1%. In Q4/2016, sales increased by 8% (9% in constant currency) to US$4,687 million (Q4/2015: US$4,348 million).

Health Care services sales (dialysis services and care coordination) increased by 8% (9% in constant currency) to US$14,519 million (2015: US$13,392 million). Dialysis product sales increased by 1% (4% in constant currency) to US$3,392 million (2015: US$3,346 million).

In North America, sales increased by 9% to US$12,886 million (2015: US$11,813 million). Health Care services sales grew by 10% to US$11,982 million (2015: US$10,932 million). Dialysis product sales increased by 3% to US$904 million (2015: US$881 million).

1 Net income attributable to shareholders of Fresenius Medical Care AG & Co. KGaA2 2016 before acquisitions (US$ 15 million after tax), 2015 before settlement costs for an agreement in principle for GranuFlo® / NaturaLyte® case (- US$ 37 million after tax), and acquisitions (US$ 9 million after tax)3 Guidance according to IFRS and in Euro currency; for a detailed overview of 2016 IFRS figures please see p. 15 of the pdf file4 Based on 2016 sales of €16,570 million. The effects of the agreement with the U.S. Departments of Veterans Affairs and Justice are excluded.5 Based on 2016 net income of €1,144 million. The effects of the agreement with the U.S. Departments of Veterans Affairs and Justice are excluded.

Sales outside North America increased by 2% (7% in constant currency) to US$5,011 million (2015: US$4,897 million). Health Care services sales increased by 3% (9% in constant currency) to US$2,537 million (2015: US$2,459 million). Dialysis product sales increased by 2% (5% in constant currency) to US$2,474 million (2015: US$2,437 million).

EBIT increased by 13% (14% in constant currency) to US$2,638 million (2015: US$2,327 million). The EBIT margin was 14.7% (2015: 13.9%). Adjusted for one-time items1, EBIT increased by 10%. In Q4/2016, EBIT increased by 19% (19% in constant currency) to US$786 million (Q4/2015: US$662 million). The EBIT margin was 16.8% (Q4/2015: 15.2%).

Net income attributable to shareholders of Fresenius Medical Care AG & Co. KGaA excluding one-time items2 increased by 16% to US$1,228 million (2015: US$1,057 million). Net income5 including one-time items increased by 21% (21% in constant currency). Net income attributable to non-controlling interest increased by 8% to US$306 million. In Q4/2016, net income5 increased by 23% to US$388 million (2015: US$317 million).

Operating cash flow increased by 9% to US$2,140 million (2015: US$1,960 million), despite a discretionary cash contribution of US$100 million to Fresenius Medical Care’s pension plan assets in the United States in Q3/2016. The cash flow margin was 11.9% (2015: 11.7%). In Q4/2016, operating cash flow reached an excellent US$844 million (Q4/2015: US$548 million) with a margin of 18.0% (Q4/2015: 12.6%).

For 2017, Fresenius Medical Care expects sales to grow by 8% to 10%3,4 in constant currency. Net income attributable to shareholders of Fresenius Medical Care AG & Co. KGaA is expected to increase by 7% to 9%3,5,6 in constant currency in 2017. The effects of the agreement with the U.S. Departments of Veterans Affairs and Justice are excluded.

For further information, please see Fresenius Medical Care’s Investor News at www.freseniusmedicalcare.com.

1 2016 before acquisitions (US$39 million before tax), 2015 before settlement costs for an agreement in principle for GranuFlo® / NaturaLyte® case (- US$ 60 million before tax), and acquisitions (US$ 16 million before tax)2 2016 before acquisitions (US$ 15 million after tax), 2015 before settlement costs for an agreement in principle for GranuFlo® / NaturaLyte® case (- US$ 37 million after tax), and acquisitions (US$ 9 million after tax)3 Guidance according to IFRS and in Euro currency; for a detailed overview of 2016 IFRS figures please see p. 15 of the pdf file4 Based on 2016 sales of €16,570 million.5 Net income attributable to shareholders of Fresenius Medical Care AG & Co. KGaA6 Based on 2016 net income of €1,144 million.

Fresenius Kabi

Fresenius Kabi offers intravenously administered generic drugs, clinical nutrition and infusion therapies for seriously and chronically ill patients in the hospital and outpatient environments. The company is also a leading supplier of medical devices and transfusion technology products.

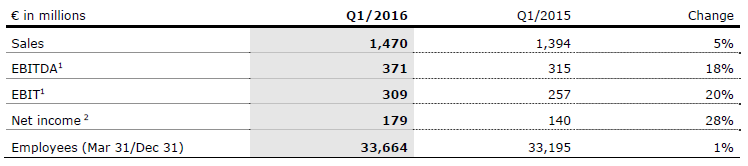

- 5% organic sales growth, 5% EBIT1 growth in constant currency

- Operating cash flow and cash flow margin at all-time high

- 2017 outlook3: 5% to 7% organic sales growth and 5% to 7% EBIT growth in constant currency expected

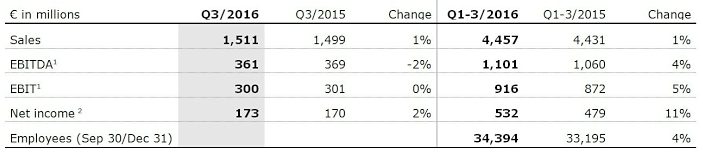

Sales increased by 1% (4% in constant currency) to €6,007 million (2015: €5,950 million). Organic sales growth was 5%. Divestitures reduced sales by 1%. Negative currency translation effects (-3%) were mainly related to the devaluation of Latin American currencies and the Chinese yuan against the Euro. In Q4/2016, sales increased by 2% (3% in constant currency) to €1,550 million (Q4/2015: €1,519 million). Organic sales growth was 3%.

Sales in Europe grew by 1% (organic growth: 3%) to €2,135 million (2015: €2,123 million). Divestments, including the sale of the German oncology compounding business in February 2015, reduced sales by 1%.

Sales in North America increased by 4% (organic growth: 3%) to €2,170 million (2015: €2,093 million), mainly driven by new product launches. Asia-Pacific sales decreased by 3% (organic growth: 8%) to €1,108 million (2015: €1,141 million) due to currency translation effects. With €594 million (2015: €593 million), sales in Latin America/Africa was on prior year level (organic growth: 14%).

EBIT1 increased by 3% (5% in constant currency) to €1,224 million (2015: €1,189 million). The EBIT margin1 improved to 20.4% (2015: 20.0%). In Q4/2016, EBIT1 decreased by 3% ( 1% in constant currency) to €308 million (Q4/2015: €317 million). The EBIT margin1 was 19.9% (Q4/2015: 20.9%).

Net income2 increased by 7% (9% in constant currency) to €716 million (2015: €669 million). In Q4/2016, net income2 decreased by 3% (-2% in constant currency) to €184 million (Q4/2015: €190 million).

Operating cash flow reached an all-time high of €991 million (2015: €913 million). The cash flow margin increased to 16.5% (2015: 15.3%). In Q4/2016, operating cash flow increased by 6% to €345 million (Q4/2015: €324 million) driven by excellent operating results, lower sequential inventory and a reduction of the Days Sales Outstanding (DSO). The margin reached an outstanding 22.3% (Q4/2015: 21.3%).

For 2017, Fresenius Kabi expects organic sales growth of 5% to 7%3 and EBIT growth in constant currency of 5% to 7%3.

1 2015 before special items2 Net income attributable to shareholders of Fresenius Kabi AG; 2015 before special items3 Guidance according to IFRS; for a detailed overview of 2016 IFRS figures please see p. 15 of the pdf fileFor a detailed overview of special items please see the reconciliation tables on pages 17-18 of the pdf file

Fresenius Helios

Fresenius Helios is Europe’s largest private hospital operator. In Germany, HELIOS operates 112 hospitals, thereof 88 acute care clinics (including seven maximum care hospitals in Berlin-Buch, Duisburg, Erfurt, Krefeld, Schwerin, Wiesbaden and Wuppertal) and 24 post-acute care clinics. Through Quirónsalud, Fresenius Helios operates 43 hospitals, 39 outpatient centers and around 300 Occupational Risk Prevention (ORP) centers in Spain.

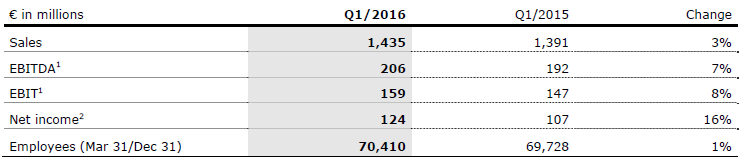

- 4% organic sales growth, €682 million EBIT1

- Acquisition of Quirónsalud closed as of January 31, 2017

- 2017 outlook3: 3% to 5%4 organic sales growth, sales of ~€8.6 bn (thereof Quirónsalud €2.5 bn5) and EBIT of €1,020 to €1,070 million (thereof Quirónsalud €300 to €320 million5,6) expected

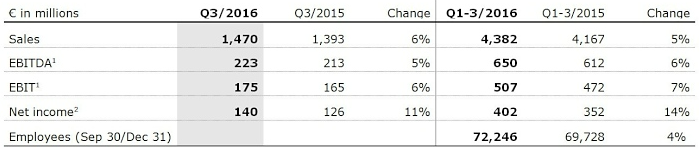

Sales increased by 5% to €5,843 million (2015: €5,578 million). Organic sales growth was 4%. Acquisitions contributed 1%. In Q4/2016, sales increased by 4% to €1,461 million (Q4/2015: €1,411 million), organic sales growth was 2%.

EBIT1 grew by 7% to €682 million (2015: €640 million). The EBIT margin1 increased to 11.7% (2015: 11.5%). In Q4/2016, EBIT1 increased by 4% to €175 million (Q4/2015: €168 million) with a margin1 of 12.0% (Q4/2015: 11.9%).

Net income2 increased by 12% to €543 million (2015: €483 million). In Q4/2016, net income2 increased by 8% to €141 million (Q4/2015: €131 million).

Operating cash flow increased by 1% to €622 million (2015: €618 million) with a margin of 10.6% (2015: 11.1%). In Q4/2016, operating cash flow reached a strong €185 million, but could not match the exceptional prior-year quarter (Q4/2015: €232 million). The same applies to the cash flow margin of 12.7% (Q4/2015: 16.4%).

For 2017, Fresenius Helios expects organic sales growth of 3% to 5%3,4 and sales of ~€8.6 bn3 (thereof Quirónsalud ~€2.5 bn5). EBIT is expected to increase to €1,020 to €1,070 million3 (thereof Quirónsalud €300 to €320 million5,6).

1 2015 before special items2 Net income attributable to shareholders of HELIOS Kliniken GmbH; before special items3 Guidance according to IFRS; for a detailed overview of 2016 IFRS figures please see p. 15 of the pdf file4 Helios Kliniken Germany, excluding Quirónsalud5 Quirónsalud consolidated for 11 months6 EBITDA of €480 to €500 million, Amortization of €80 million and depreciation of €100 million

For a detailed overview of special items please see the reconciliation tables on pages 17-18 of the pdf file.

Fresenius Vamed

Fresenius Vamed manages projects and provides services for hospitals and other health care facilities worldwide. The portfolio ranges along the entire value chain: from project development, planning, and turnkey construction, via maintenance and technical management, to total operational management.

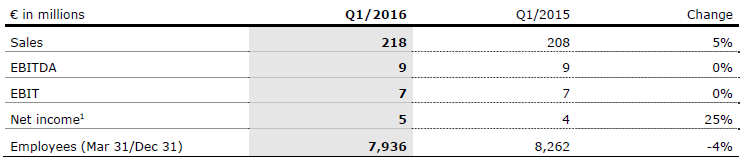

- 5% organic sales growth, 8% EBIT growth

- Order intake of €1,017 million at all-time high

- 2017 outlook1: 5% to 10% organic sales growth and 5% to 10% EBIT growth expected

Sales increased by 4% (4% in constant currency) to €1,160 million (2015: €1,118 million). Organic sales growth was 5%. Sales in the project business increased by 3% to €594 million (2015: €575 million). Sales in the service business grew by 4% to €566 million (2015: €543 million). In Q4/2016, sales increased to €420 million (Q4/2015: €387 million). Organic sales growth was 10%.

EBIT grew by 8% to €69 million (2015: €64 million). The EBIT margin increased to 5.9% (2015: 5.7%). In Q4/2016, EBIT increased by 12% to €38 million (Q4/2015: €34 million). The EBIT margin increased to 9.0%.

Net income2 grew by 2% to €45 million (2015: €44 million). In Q4/2016, net income2 remained unchanged at €24 million (Q4/2015: €24 million).

Order intake increased to €1,017 million (2015: €904 million), reaching an all-time high. As of December 31, 2016, order backlog was €1,961 million (Dec. 31, 2015: €1,650 million).

For 2017, Fresenius Vamed expects organic sales growth in the range of 5% to 10%1 and EBIT growth of 5% to 10%1.

1 Guidance according to IFRS; for a detailed overview of 2016 IFRS figures please see p. 15 of the pdf file2 Net income attributable to shareholders of VAMED AG

Conference Call

As part of the publication of the results for fiscal year 2016, a conference call will be held on February 22, 2017 at 2 p.m. CET (8 a.m. EST). All investors are cordially invited to follow the conference call in a live broadcast over the Internet at www.fresenius.com/investors. Following the call, a replay will be available on our website.

This release contains forward-looking statements that are subject to various risks and uncertainties. Future results could differ materially from those described in these forward-looking statements due to certain factors, e.g. changes in business, economic and competitive conditions, regulatory reforms, results of clinical trials, foreign exchange rate fluctuations, uncertainties in litigation or investigative proceedings, and the availability of financing. Fresenius does not undertake any responsibility to update the forward-looking statements in this release.

Fresenius SE & Co. KGaA (“Fresenius”) will focus its reporting on financial statements in accordance with International Financial Reporting Standards (IFRS) starting with the 2017 fiscal year on January 1, 2017. The company will then no longer provide U.S. GAAP financial information.

Fresenius, as a publicly traded company based in a European Union member country, is required to prepare and publish its consolidated financial statements in accordance with International Financial Reporting Standards (IFRS) pursuant to Section 315a of the German Commercial Code (HGB).

In addition to this compulsory IFRS accounting, Fresenius also publishes consolidated financial statements in accordance with U.S. GAAP. This has provided comparability with the Group’s largest subsidiary, Fresenius Medical Care, which was required to report in accordance with U.S. GAAP under a so-called Pooling Agreement. However, Fresenius Medical Care’s 2016 Annual General Meeting has lifted this obligation.

In the interest of harmonizing the management and accounting of the Fresenius Group and all of its business segments, the Fresenius Group and all of its business segments will report solely in accordance with IFRS starting with the 2017 fiscal year on January 1, 2017.

For the 2016 fiscal year, Fresenius will as in past years provide both U.S. GAAP and IFRS consolidated financial statements.