Q2/2025: Ongoing strong revenue and EPS growth, guidance for organic revenue growth raised

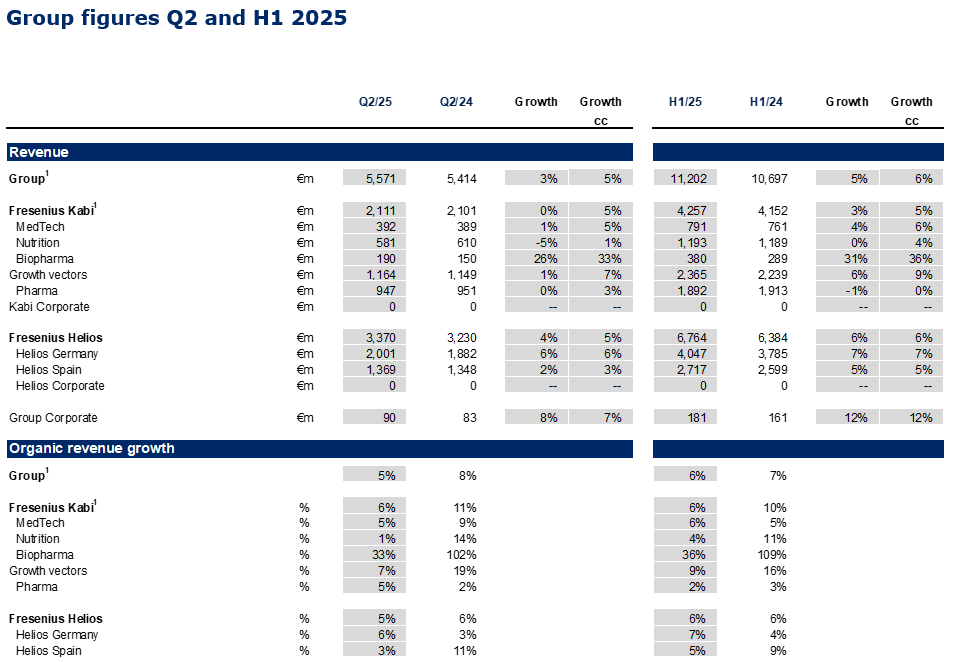

- Group revenue1 at €5,571 million with organic growth of 5%1,2 driven by consistent delivery across the core businesses Fresenius Kabi and Fresenius Helios as well as ongoing execution of #FutureFresenius.

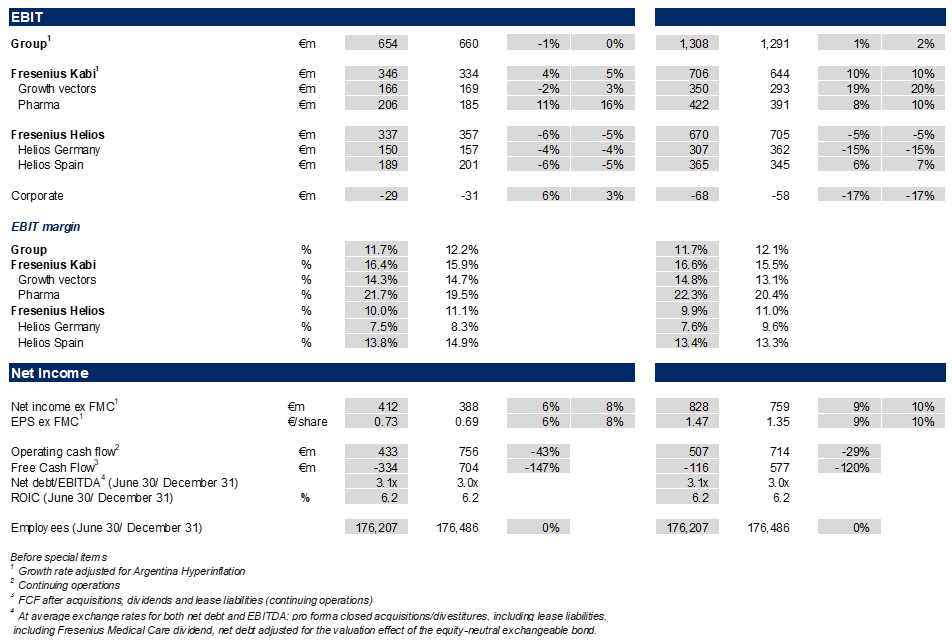

- Group EBIT1 broadly stable3 in constant currency at €654 million impacted by the headwinds from ceased energy relief payments at Helios Germany and the loss of the volume-based procurement tender for the nutrition product Ketosteril in China at Fresenius Kabi; Group EBIT margin1 at 11.7%.

- Net income1,4 with strong 8%3 growth in constant currency to €412 million outpacing revenue growth.

- EPS1,4 rose by strong 8%3 in constant currency to €0.73 demonstrating continued bottom-line delivery based on operating strength and significantly decreased interest expenses.

- Net debt/EBITDA ratio at 3.1x1,5 driven by resumed dividend payment in Q2/25.

- Pro rata sale of Fresenius Medical Care shares to maintain current stake in response to the announced Fresenius Medical Care share buyback program.

1Before special items

2Organic growth rate adjusted for accounting effects related to Argentina hyperinflation

3Growth rate adjusted for Argentina hyperinflation

4Excluding Fresenius Medical Care

5At average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures, including lease liabilities, including Fresenius Medical Care dividend, net debt adjusted for the valuation effect of the equity-neutral exchangeable bond

Michael Sen, CEO of Fresenius: “Fresenius has demonstrated a resilient and consistent performance in the first half of 2025, with another quarter of strong momentum reflected by 8% Core EPS growth. Fresenius Kabi and Fresenius Helios continue to deliver strong results despite macroeconomic challenges, thanks to our focused strategy and disciplined execution. This performance enables us to raise our guidance, increasing our full-year expectations for revenue growth to between 5% and 7%. #FutureFresenius is paying off.

Our ambitions remain unchanged: Our current strategy phase Rejuvenate will focus on organic growth through disciplined capital allocation - upgrading our core, and scaling our platforms to enhance performance further. We are committed to delivering profitable growth through targeted investments in health and digital innovation, which together will create and enhance value for our stakeholders."

Guidance raised for Fiscal Year 20251

Based on the consistent growth at the top-end of the 2025 guidance in H1/25, organic revenue guidance was raised:

Fresenius Group2: organic revenue growth3 now expected in the range of 5 to 7% (previous: 4 to 6%); constant currency EBIT growth4 in the range of 3% to 7%

Fresenius Kabi5: organic revenue growth3 in the mid- to high-single-digit percentage range; EBIT margin of 16.0% to 16.5%

Fresenius Helios6: organic revenue growth in the mid-single-digit percentage range; EBIT margin around 10%

Assumptions to guidance: When Fresenius gave guidance in February, the company acknowledged the fast-moving macro-economic and geopolitical environment, resulting in a higher level of operational uncertainty. Fresenius’ guidance continues to reflect current factors and known uncertainties such as impacts from tariffs to the extend they can currently be assessed. The guidance does not take into account potential extreme scenarios that could affect the company, its peers, and the healthcare sector as a whole.

1Before special items

22024 base: €21,526 million (revenue) and €2,489 million (EBIT)

3Organic growth rate adjusted for accounting effects related to Argentina hyperinflation

4Growth rate adjusted for Argentina hyperinflation

52024 base: €8,414 million (revenue) and €1,319 million (EBIT)

62024 base: €12,739 million (revenue) and €1,288 million (EBIT)

Fresenius Group – Business development Q2/25

In Q2/2025, the good operating performance of Fresenius Kabi and Fresenius Helios led to a 5%1 Group organic revenue increase to €5,571 million.

As expected, Group EBIT before special items was broadly stable3 in constant currency, and amounted to €654 million. This is related to the headwinds from the absence of energy relief payments at Helios Germany and the Volume Based Procurement of the nutrition product Ketosteril in China at Fresenius Kabi. Despite the negative effects, Group EBIT margin was 11.7% (Q2/24: 12.2%). The Helios Performance Programme is advancing with increasing contributions expected in the second half of the year.

Earnings per share2,4 rose by a strong 8%3 in constant currency to €0.73, driven by the operating strength and the significantly decreased interest expenses.

Following the announcement of Fresenius Medical Care AG (FME) in June 2025 to initiate a share buyback program, Fresenius intends to sell shares of FME on a pro rata basis to maintain its current stake of around 28.6% in FME. The final size and tranching of the sale of shares will be determined based on the structure of the share buyback program of FME. As previously announced, Fresenius remains a committed shareholder and will retain no less than 25 per cent plus one share of FME.

Fresenius will use the proceeds to invest in its core business in line with the #FutureFresenius strategy and Fresenius' stated capital allocation priorities, including further strengthening the balance sheet, reducing leverage, and delivering shareholder value and long-term growth.

1Organic growth rate adjusted for accounting effects related to Argentina hyperinflation

2Before special items

3Growth rate adjusted for Argentina hyperinflation

4Excluding Fresenius Medical Care

Operating Companies – Business development Q2/25

Fresenius Kabi delivered a strong performance; Growth Vectors with ongoing momentum, continued Biopharma strength; licensing agreement to commercialize a proposed vedolizumab biosimilar candidate

Organic revenue growth of 6%3 mainly driven by the Growth Vectors and the good contribution from Pharma; reflecting the less pronounced positive Argentina pricing effects; revenue was broadly flat at €2,111 million due to currency effects; increased by 5%2 in constant currency.

- Growth Vectors with good organic revenue3 increase of 7%: MedTech 5%, Nutrition 1%, Biopharma 33%.

- Nutrition revenue: €581 million, growth clearly influenced by the tender impact from the Volume Based Procurement (VBP) on Ketosteril in China (ex Ketosteril healthy organic growth in line with ambition range), good development in Latin America and Europe; in the U.S. ongoing successful roll-out of lipid emulsions.

- Biopharma revenue: €190 million, positive development mainly driven by the Tyenne biosimilar ramp up in Europe and the U.S. as well as Idacio; denosumab biosimilars Conexxence® (denosumab-bnht) and Bomyntra® (denosumab-bnht) launched in the U.S. and approved in Europe; expansion of autoimmune biosimilars portfolio: licensing agreement with Polpharma Biologics to commercialize a proposed vedolizumab biosimilar candidate (excluding region MENA).

- MedTech revenue: €392 million, increase driven by the expansion in Cell Therapy in the U.S., and solid growth in Europe.

- Pharma revenue: €947 million, strong organic revenue development3 with 5% growth based on good volumes including I.V. fluids in the U.S., and Europe with favourable pricing.

- EBIT1 of Fresenius Kabi with 5%2 constant currency increase to €346 million, driven by the strong margin development of the Pharma, MedTech and Biopharma business and ongoing improvements in the cost base. The EBIT margin1 was at the upper end of the guidance range at 16.4% despite transaction exchange rate effects and headwinds on the Nutrition business in China.

- EBIT1 of the Growth Vectors increased 3%2 in constant currency against the backdrop of the Ketosteril effect, and amounted to €166 million; EBIT margin1 at 14.3%.

- EBIT1 of Pharma increased 16%2 in constant currency to €206 million. EBIT margin1 was strong at 21.7% due to ongoing cost savings and some one-timers.

Fresenius Helios with solid organic revenue growth; expected softness in profitability at Helios Germany partially offset by good development at Helios Spain; Helios Performance Programme is advancing.

Strong 5% organic revenue growth driven by Helios Germany (6% organic growth); Helios Spain at 3% organic growth (H1/25: 5%) linked to the Easter effect, which resulted into less activity at the beginning of Q2/25 and impacted growth predominantly at Helios Spain; revenue before special items increased by 5% in constant currency to €3,370 million.

- Helios Germany with revenue1 of €2,001 million; growth mainly driven by price effects, as well as good activity levels and case mix.

- Helios Spain with revenue of €1,369 million, impacted by the Easter timing and currency translation effects related to the clinics in Latin America. The clinics in Latin America showed a good operational performance.

- EBIT1 of Fresenius Helios as expected declined -5% in constant currency to €337 million impacted by the absence of energy relief funds in Germany. This expected softness was partially compensated by the excellent profitability at Helios Spain. EBIT margin1 of Fresenius Helios was resilient at 10.0%.

- EBIT1 of Helios Germany decreased by -4% to €150 million against the high prior-year base which included energy relief funds; EBIT margin at 7.5% improved by 90 bps compared to Q4/24 (6.6%), the first quarter without energy relief funds.

- EBIT1 of Helios Spain decreased by -5% in constant currency to €189 million related to a very strong prior-year base and the Easter effect; EBIT margin1 at a strong 13.8%.

- Helios performance programme is advancing; ramp-up in H2/25 expected with more meaningful EBIT contributions, as some of the levers are process-related and will take time to deliver and realize benefits.

1Before special items

2Growth rate adjusted for Argentina hyperinflation.

3Organic growth rate adjusted for accounting effects related to Argentina hyperinflation

Conference call and Audio webcast

As part of the publication of the Q2/2025 results, a conference call will be held on August 6, 2025 at

1:30 p.m. CEST / 7:30 a.m. EDT. All investors are cordially invited to follow the conference call in a live audio webcast at https://www.fresenius.com/investors. Following the call, a replay will be available on our website.

Contact for shareholders

Investor Relations

Telephone: + 49 61 72 6 08-24 87

Telefax: + 49 61 72 6 08-24 88

E-mail: ir-fre@fresenius.com

Information on Fresenius share and ADRs

Note on the presentation of financial figures

- If no timeframe is specified, information refers to Q2/2025.

- Consolidated results for Q2/25 as well as for Q2/24 include special items. An overview of the results for Q2/2025 - before and after special items – is available on our website.

- Growth rates in constant currency of Fresenius Kabi are adjusted. Adjustments relate to the hyperinflation in Argentina. Accordingly, constant currency growth rates of the Fresenius Group are also adjusted.

- The results of Fresenius Helios and accordingly of the Fresenius Group for Q2/24 are adjusted by the sale of the fertility services group Eugin and the divestment of the majority stake in the hospital Clínica Ricardo Palma hospital in Lima, Peru.

- Information on the performance indicators is available on our website at https://www.fresenius.com/alternative-performance-measures.

This release contains forward-looking statements that are subject to various risks and uncertainties. Future results could differ materially from those described in these forward-looking statements due to certain factors, e.g. changes in business, economic and competitive conditions, regulatory reforms, results of clinical trials, foreign exchange rate fluctuations, uncertainties in litigation or investigative proceedings, the availability of financing and unforeseen impacts of international conflicts. Fresenius does not undertake any responsibility to update the forward-looking statements in this release.

Fresenius Kabi, part of the global healthcare company Fresenius, has entered a licensing agreement with Polpharma Biologics S.A., a developer and manufacturer of biosimilar products, based in Poland. Under the agreement, Fresenius Kabi will exclusively commercialize Polpharma Biologics’ vedolizumab biosimilar candidate PB016 globally, except the Middle East and North Africa, pending approval by respective regulatory authorities.

PB016 is a biosimilar candidate to Entyvio®*, an integrin receptor antagonist used in the treatment of moderately to severely active ulcerative colitis and Crohn’s disease.

“Today marks a significant milestone in our journey to provide patients with access to affordable, high-quality biosimilar treatments,” said Dr. Sang-Jin Pak, President Biopharma at Fresenius Kabi. “The in-licensing of PB016 from Polpharma Biologics underscores our commitment to expanding our autoimmune biosimilars portfolio and addressing the unmet needs of patients with chronic inflammatory diseases.”

This agreement builds on Fresenius Kabi’s successful track record in the biosimilars market, including the recent FDA and EC approvals of its denosumab and ustekinumab biosimilars. This milestone underscores Fresenius Kabi’s commitment to broadening access to essential, high-quality biosimilar therapies. Through this agreement, Fresenius is strengthening its (Bio)Pharma platform, which is a key pillar of the #FutureFresenius strategy.

*Entyvio® is a registered trademark of Takeda.

Fresenius Kabi, part of the global healthcare company Fresenius, has entered a licensing agreement with Polpharma Biologics S.A., a developer and manufacturer of biosimilar products, based in Poland. Under the agreement, Fresenius Kabi will exclusively commercialize Polpharma Biologics’ vedolizumab biosimilar candidate PB016 globally, except the Middle East and North Africa, pending approval by respective regulatory authorities.

PB016 is a biosimilar candidate to Entyvio®*, an integrin receptor antagonist used in the treatment of moderately to severely active ulcerative colitis and Crohn’s disease.

“Today marks a significant milestone in our journey to provide patients with access to affordable, high-quality biosimilar treatments,” said Dr. Sang-Jin Pak, President Biopharma at Fresenius Kabi. “The in-licensing of PB016 from Polpharma Biologics underscores our commitment to expanding our autoimmune biosimilars portfolio and addressing the unmet needs of patients with chronic inflammatory diseases.”

This agreement builds on Fresenius Kabi’s successful track record in the biosimilars market, including the recent FDA and EC approvals of its denosumab and ustekinumab biosimilars. This milestone underscores Fresenius Kabi’s commitment to broadening access to essential, high-quality biosimilar therapies. Through this agreement, Fresenius is strengthening its (Bio)Pharma platform, which is a key pillar of the #FutureFresenius strategy.

*Entyvio® is a registered trademark of Takeda.

Fresenius announced today that the European Commission has granted approval for their denosumab biosimilars Conexxence®* and Bomyntra®* in Europe.

The two approvals cover all indications of the reference products including osteoporosis in postmenopausal women and at-risk men, treatment-related bone loss, prevention of skeletal complications from cancer metastasis to bone, and giant cell tumor of bone.

This milestone marks a significant advancement in Fresenius Kabi’s mission to expand access to high-quality biosimilar therapies. It also reinforces the business’ commitment to strengthening its Biopharma platform, a key pillar of the #FutureFresenius strategy.

*Conexxence and *Bomyntra are registered trademarks of Fresenius Kabi Deutschland GmbH in selected countries.

Fresenius announced today that the European Commission has granted approval for their denosumab biosimilars Conexxence®* and Bomyntra®* in Europe.

The two approvals cover all indications of the reference products including osteoporosis in postmenopausal women and at-risk men, treatment-related bone loss, prevention of skeletal complications from cancer metastasis to bone, and giant cell tumor of bone.

This milestone marks a significant advancement in Fresenius Kabi’s mission to expand access to high-quality biosimilar therapies. It also reinforces the business’ commitment to strengthening its Biopharma platform, a key pillar of the #FutureFresenius strategy.

*Conexxence and *Bomyntra are registered trademarks of Fresenius Kabi Deutschland GmbH in selected countries.