- Helios Germany is increasing number of intensive care beds by two thirds

- Law to ease financial burden on hospitals likely to offset large part of sales losses and cost increases

- Digital healthcare offerings facilitate continuous medical care for chronically ill and rehabilitation patients

Helios Germany, Germany’s largest private hospital operator and part of the Fresenius Group, is undertaking comprehensive measures to combat the COVID-19 pandemic. In accordance with the German government’s request, surgical procedures are being delayed whenever medically justifiable. The freed-up capacity is reserved for the imminent treatment of COVID-19 patients. Postponed operations should be performed later this year and next. In parallel, Helios Germany will increase the number of ICU beds in its network by two-thirds, from 900 to more than 1,500. This will be accomplished by deploying centrally held equipment reserves across its network as well as by selectively upgrading intermediate care beds and converting operation theatres with already installed ventilator systems.

In order to utilize the incremental capacity most effectively, Helios Germany has selectively adjusted shift models and is prepared to deploy specialist staff across its network to hospitals with particular needs.

Helios Germany is closely monitoring its inventories of important hospital supplies – including disinfectants and protective clothing – and building additional reserves.

Stephan Sturm, CEO of Fresenius, said: “Society is facing very challenging weeks and months ahead. Commitment, sound judgement and close cooperation will all be needed to contain the spread of the coronavirus. At the same time, the best possible care must be provided to patients. Our deepest thanks go to doctors, nurses and care personnel, whether they work at Fresenius or elsewhere: They are needed more than ever, and show tremendous dedication day after day. As a healthcare Group we have a special responsibility in this situation. We must, and we will, meet this responsibility.”

To ease the financial burden on the country’s hospitals during the COVID-19 pandemic, Germany’s Federal Ministry of Health submitted earlier this week a draft law, which was passed by the Bundestag on Wednesday. Among its key provisions:

- Compensation payment of €560 per foregone treatment day compared to 2019.

- Reimbursement of care costs with a flat-rate payment of at least €185 per treatment day.

- Reimbursement of increased costs for protective clothing and other supplies with a flat-rate payment of €50 per patient.

- Public health insurers will settle all treatment invoices in 2020 within five days.

- Significant reduction of health insurers’ (MDK) audit quota and abolition of minimum fines for this year and 2021.

- Co-investment of €50,000 for each new intensive care bed; costs above this amount may be reimbursed by individual state governments.

Fresenius Helios generally welcomes these measures. Assuming the pandemic substantially subsides by the summer, management currently estimates that the financial impact on Helios Germany in 2020, although negative, will not be very significant.

Dr. Francesco De Meo, CEO of Fresenius Helios, said: “It is our approach to combine ethically responsible care for our patients with a high degree of efficiency. To this end, we have invested heavily in our clinics, in our medical technology and also in strengthening our staff in recent years. This is paying off now. The close networking of our hospitals gives us the necessary flexibility to deploy personnel and materials exactly where patients need them most. And we gain insights very swiftly by sharing experiences with our colleagues, through the European exchange that is embedded in Fresenius‘ global network. We are therefore ideally positioned in the joint fight against COVID-19.”

Fresenius is committed to the care of patients with a high infection risk. Given the current treatment restrictions and infection risks, there are significant challenges for the chronically ill to visit local medical practices and get the treatment and support they need. Particularly for these patients, digital healthcare offerings can be a suitable alternative. Following its acquisition of Digitale Gesundheitsgruppe, Fresenius’ subsidiary Curalie now offers an even wider range of digital healthcare services for patients with chronic illnesses such as diabetes, kidney disease and heart disease, through to rehabilitation patients in orthopedic aftercare. For the duration of the current COVID-19 pandemic, Curalie will make its digital healthcare services available free of charge. Thus, Fresenius and Curalie are helping to ensure continuous medical care to these vulnerable patients.

This release contains forward-looking statements that are subject to various risks and uncertainties. Future results could differ materially from those described in these forward-looking statements due to certain factors, e.g. changes in business, economic and competitive conditions, regulatory reforms, results of clinical trials, foreign exchange rate fluctuations, uncertainties in litigation or investigative proceedings, and the availability of financing. Fresenius does not undertake any responsibility to update the forward-looking statements in this release.

With virtually all of Fresenius Kabi’s manufacturing staff in China returning to work post government-imposed COVID-19 quarantine restrictions, the company is ramping-up production back to normal levels. With a further stabilization of the situation, Fresenius Kabi also expects a gradual resumption of its sales force activities in China. Even though Fresenius Kabi faced challenges due to the COVID-19 pandemic and the quarantine measures, there was no major interruption of production. Thus, the company can supply the Chinese population with essential pharmaceuticals and medical devices.

- All Quirónsalud hospitals are fully operational and managed by Quirónsalud in close coordination with the health authorities

- Rumors about a “nationalization” are without any basis

Quirónsalud, the largest private hospital group in Spain and part of Fresenius Helios, is fully committed to supporting the national effort against COVID-19 with all available resources. Since the start of the crisis, Quirónsalud has worked in close and trustful cooperation with national and regional healthcare authorities to provide the best possible treatment to the greatest possible number of patients.

Quirónsalud’s network currently comprises about 400 ICU beds for adults in almost 50 hospitals across Spain. The company is undertaking significant efforts to further increase this number in the short term, while continuing to treat other patients who urgently need medical support such as for chemotherapy, giving birth, and other emergencies.

Despite the high number of suspected and confirmed COVID-19 cases entering Quirónsalud’s hospitals, the company has kept every hospital fully operational. This is to a large extent due to the outstanding commitment of Quirónsalud’s medical and nursing staff, who deserve the utmost recognition and gratitude. So far, Quirónsalud has also been able to secure sufficient quantities of medical materials for all its hospitals, despite rapidly rising demand for critical supplies.

In the course of the formal declaration of a ‘State of Alarm’, the Spanish government has temporarily obtained the right to direct all hospitals in the country, allowing the healthcare authorities to leverage all available resources to treat COVID-19 patients as effectively as possible. Such an option is embedded in the established crisis management plans of many other European countries as well. Quirónsalud fully supports this measure, as it allows centralized capacity management, and hence rapid responses to changing circumstances and a full dedication of the entire system to fight the coronavirus.

Rumors about a “nationalization” of Spain’s private hospital system are clearly wrong and without any basis. Quirónsalud continues to manage its hospitals, and is already operating the additional beds requested by the authorities, in the joint effort against the COVID-19 threat for the benefit of Spain and the broader society.

This release contains forward-looking statements that are subject to various risks and uncertainties. Future results could differ materially from those described in these forward-looking statements due to certain factors, e.g. changes in business, economic and competitive conditions, regulatory reforms, results of clinical trials, foreign exchange rate fluctuations, uncertainties in litigation or investigative proceedings, and the availability of financing. Fresenius does not undertake any responsibility to update the forward-looking statements in this release.

Our Annual Report 2019 is now available as a full-content PDF download and as an online short-version with the highlights. Annual Report (PDF) Online short-version

Curalie, a subsidiary of Fresenius, has acquired Digitale Gesundheitsgruppe (DGG), one of its main competitors in Germany. Curalie and DGG both develop digital healthcare offerings to help patients with chronic illnesses. DGG targets family and specialist physicians with its “TeLiPro” telemedicine platform, while Curalie develops digital solutions for rehabilitation and aftercare. Combining the two companies creates the first provider that in all sectors of healthcare can digitally support patients during outpatient and inpatient care and through to aftercare.

The market research institute Potentialpark has honored the global healthcare group Fresenius for the ninth consecutive year as the German company with the best overall Internet offering for job applicants.

In Potentialpark’s 2020 study, Fresenius not only took first place in the overall category for all career-relevant online activities but won in three of the four individual categories: Online Application Management, Mobile, and Career Website. The company was second in the Social Media category.

Potentialpark has carried out an annual study of German companies’ online offerings for job applicants since 2002. For this year’s study, Potentialpark assessed the online activities of 140 German companies according to more than 300 criteria. More than 46,000 students and graduates around the world were surveyed about their preferences.

“We are delighted to once again receive confirmation of the high quality of our Internet offering for job applicants,” said Michael Lehmann, Senior Vice President Corporate Human Resources of Fresenius. “In the past year we have expanded it with a digital onboarding portal, and are already at work on our next enhancements: We are internationalizing some of our social media channels for potential applicants. And we’re developing a construction kit for the web, so that country units of the Fresenius Group can put together their own career portals, set up to meet their specific requirements.”

This release contains forward-looking statements that are subject to various risks and uncertainties. Future results could differ materially from those described in these forward-looking statements due to certain factors, e.g. changes in business, economic and competitive conditions, regulatory reforms, results of clinical trials, foreign exchange rate fluctuations, uncertainties in litigation or investigative proceedings, and the availability of financing. Fresenius does not undertake any responsibility to update the forward-looking statements in this release.

-

Press conference on the 2019 financial results on February 20, 2020 at the Fresenius headquarters in Bad Homburg, Germany. Download Image (JPG 2.08 MB) -

![]()

Stephan Sturm, CEO of Fresenius Download Image (JPEG 1.95 MB) -

![]()

Stephan Sturm, CEO of Fresenius. Download Image (JPEG 2.05 MB) -

![]()

Helen Giza, CFO Fresenius Medical Care, and Rice Powell, CEO Fresenius Medical Care. Download Image (JPG 897 KB) -

![]()

From left: Stephan Sturm (CEO Fresenius), Rachel Empey (CFO Fresenius), Helen Giza (CFO Fresenius Medical Care, Rice Powell (CEO Fresenius Medical Care). Download Image (JPEG 1.72 MB) -

![]()

Stephan Sturm, CEO of Fresenius, and Rachel Empey, CFO of Fresenius Download Image (JPG 1.78 MB) -

![]()

Filling of glass bottles with liquid pharmaceuticals at the Fresenius Kabi plant in Friedberg, Germany. Download Image (JPG 838 KB) -

![]()

Logo at the Fresenius corporate head office in Bad Homburg. Download Image (JPG 18.63 MB) -

![]()

Operating room at a HELIOS clinic. More press photos can be found in our media center. Download Image (JPG 1.30 MB) -

![]()

A nurse prepares an intravenously administered (I.V.) drug. Fresenius Kabi is a leading supplier of I.V. generic drugs. More press photos can be found in our media center. Download Image (V 1.95 MB) -

![]()

Fresenius Medical Care: Production of dialyzers at St. Wendel. More press photos can be found in our media center. Download Image (JPG 3.42 MB)

• Good organic sales growth across all business segments

• Fresenius Kabi’s excellent Emerging Markets growth partially offsets softer development in North America

• Fresenius Helios shows continued stabilization in Germany and strong growth in Spain

• Fresenius Medical Care expects to show strong growth in 2020

• 27th consecutive dividend increase proposed

If no timeframe is specified, information refers to Q4/2019

1 Adjusted for IFRS 16

2 Q4/18 and FY/18 before special items and adjusted for divestitures of Care Coordination activities at Fresenius Medical Care (FMC)

3 Net income attributable to shareholders of Fresenius SE & Co. KGaA

For a detailed overview of special items and adjustments please see the reconciliation tables on pages 20-28 of the PDF document.

Stephan Sturm, CEO of Fresenius, said: “2019 was a good year for Fresenius. A year of challenges, but also of many successes. We have treated even more patients, launched new products, and increased our sales to more than 35 billion euros. We made the planned, significant investments in our future growth, yet have still achieved a slight increase in earnings. Fresenius is well positioned to stay successful into the future. We can look ahead with confidence, and confirm our ambitious medium-term targets.”

Group guidance for FY/20

For FY/20, Fresenius projects sales growth1 of 4% to 7% in constant currency. Net income2,3 growth is expected to be in a 1% to 5% range in constant currency. Contributions from signed, but not yet closed acquisitions are included in this guidance.

The FY/20 guidance does not include any effects from the coronavirus (Covid-19) outbreak, since it is too early to quantify those. From the current perspective Fresenius does not expect a significant negative financial impact4.

Fresenius expects net debt/EBITDA5 to be towards the top-end of the self-imposed target corridor of 3.0x to 3.5x at the end of 2020.

Growth targets for 2020 – 2023 confirmed

Fresenius continues to expect Group sales to grow organically with a compounded annual growth rate (CAGR) of 4% to 7% during 2020 to 2023. Group net income2 is projected to increase organically with a CAGR of 5% to 9% during 2020 to 2023. Fresenius expects its sales growth and efficiency improvement initiatives as well as Fresenius Kabi’s biosimilars business to drive an acceleration of Group earnings growth over that period. Small and medium-sized acquisitions are expected to contribute an incremental CAGR of approx. 1%-point to both sales and net income growth.

27th consecutive dividend increase proposed

The Management Board of Fresenius will propose to the Supervisory Board a dividend increase of 5% to €0.84 per share for FY/19 (FY/18: €0.80). The proposed total dividend payout to Fresenius SE & Co. KGaA shareholders amounts to €468 million (FY/18: €445 million).

1 FY/19 base: €35,409 million, including IFRS 16 effect

2 Net income attributable to shareholders of Fresenius SE & Co. KGaA

3 FY/19 base: €1,879 million, including IFRS 16 effect; FY/19 before special items (transaction-related expenses, revaluations of biosimilars contingent purchase price liabilities, gain related to divestitures of Care Coordination activities at FMC, expenses associated with the cost optimization program at FMC); FY/20: before special items

4 Taking into account minority interest structures across the Group

5 Both net debt and EBITDA including IFRS 16 effect and calculated at expected annual average exchange rates; excluding further potential acquisitions

For a detailed overview of special items and adjustments please see the reconciliation tables on pages 20-28 of the PDF document.

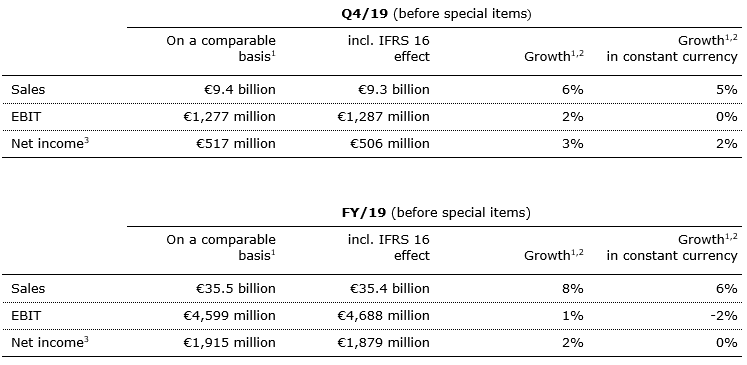

5% sales growth1 in constant currency

In Q4/19, Group sales were €9,311 million including an IFRS 16 effect of -€40 million. Group sales1 on a comparable basis increased by 6% (5% in constant currency) to €9,351 million in Q4/19 (Q4/18: €8,830 million). Organic sales growth was 4%. Acquisitions/divestitures contributed net 1% to growth. In FY/19, Group sales were €35,409 million including an IFRS 16 effect of -€115 million. On a comparable basis, Group sales1 increased by 8% (6% in constant currency) to €35,524 million (FY/18: €33,009 million). Organic sales growth was 5%. Acquisitions/divestitures contributed net 1% to growth. Positive currency translation effects of 2% were mainly driven by the U.S. dollar strengthening against the euro.

2% net income2,3 growth in constant currency

In Q4/19, Group EBITDA before special items was €1,937 million including an IFRS 16 effect of €235 million. On a comparable basis, Group EBITDA2 increased by 1% (0% in constant currency) to €1,702 million (Q4/18: €1,680 million). Reported Group EBITDA4 was €1,937 million. In FY/19, Group EBITDA before special items was €7,104 million including an IFRS 16 effect of €934 million. On a comparable basis, Group EBITDA2 increased by 2% (0% in constant currency) to €6,170 million (FY/18: €6,032 million). Reported Group EBITDA4 was €7,083 million.

In Q4/19, Group EBIT before special items was €1,287 million including an IFRS 16 effect of €10 million. On a comparable basis, Group EBIT2 increased by 2% (0% in constant currency) to €1,277 million (Q4/18: €1,250 million). The EBIT margin2 on a comparable basis was 13.7% (Q4/18: 14.2%). Reported Group EBIT4 was €1,269 million.

In FY/19, Group EBIT before special items was €4,688 million including an IFRS 16 effect of €89 million. On a comparable basis, Group EBIT2 increased by 1% (-2% in constant currency) to €4,599 million (FY/18: €4,547 million). The EBIT margin2 on a comparable basis was 12.9% (FY/18: 13.8%). Reported Group EBIT4 was €4,631 million. Adjustments on accounts receivable in legal dispute paired with reduced patient attribution and a decreasing savings rate for ESCOs at Fresenius Medical Care weighed on earnings. In addition, the missing tailwinds from drug shortages in North America triggered a softer development at Fresenius Kabi. Moreover, investments to counter the regulatory headwinds at Helios Germany continued to weigh on Group EBIT. These effects were partially offset by the remeasurement effect of the fair value of Fresenius Medical Care’s investment on Humacyte, Inc.

1 On a comparable basis: Q4/18 and FY/18 adjusted for divestitures of Care Coordination activities at FMC; Q4/19 and FY/19 adjusted for IFRS 16 effect

2 On a comparable basis: Q4/19 and FY/19 before special items and adjusted for IFRS 16 effect; Q4/18 and FY/18 before special items and adjusted for divestitures of Care Coordination activities at FMC

3 Net income attributable to shareholders of Fresenius SE & Co. KGaA

4 After special items and including IFRS 16 effect

For a detailed overview of special items and adjustments please see the reconciliation tables on pages 20-28 of the PDF document.

In Q4/19, Group net interest before special items was -€182 million including an IFRS 16 effect of -€51 million. On a comparable basis, net interest1 increased to -€131 million in Q4/19 (Q4/18: -€129 million). Reported Group net interest2 was -€184 million. In FY/19, Group net interest before special items was -€714 million including an IFRS 16 effect of -€204 million. On a comparable basis, net interest1 improved to -€510 million (FY/18: -€549 million) mainly due to successful refinancing activities and lower interest rates. Reported Group net interest2 was -€719 million.

In Q4/19, the Group tax rate before special items and adopting IFRS 16 was 23.8%, in FY/19 it was 23.3%. On a comparable basis, the Group tax rate1 was 24.0% in Q4/19 and 23.4% in FY/19 (Q4/18: 22.7%; FY/18: 22.1%). The YoY increase was driven by positive one-time effects in the prior-year relating to the US tax reform.

In Q4/19, Noncontrolling interest before special items was -€336 million including an IFRS 16 effect of €18 million. On a comparable basis, noncontrolling interest1 was -€354 million (Q4/18: -€363 million). In FY/19, noncontrolling interest before special items was -€1,170 million including an IFRS 16 effect of €49 million. On a comparable basis, noncontrolling interest1 was -€1,219 million (FY/18: -€1,243 million), of which 96% was attributable to the noncontrolling interest in Fresenius Medical Care.

In Q4/19, Group net income3 before special items was €506 million including an IFRS 16 effect of -€11 million. On a comparable basis, Group net income1,3 increased by 3% (2% in constant currency) to €517 million (Q4/18: €504 million). Reported Group net income2,3 was €515 million.

In FY/19, Group net income3 before special items was €1,879 million including an IFRS 16 effect of -€36 million. On a comparable basis, Group net income1,3 increased by 2% (0% in constant currency) to €1,915 million (FY/18: €1,872 million). Reported Group net income2,3 was €1,883 million.

1 On a comparable basis: Q4/19 and FY/19 before special items and adjusted for IFRS 16 effect; Q4/18 and FY/18 before special items and adjusted for divestitures of Care Coordination activities at FMC

2 After special items and including IFRS 16 effect

3 Net income attributable to shareholders of Fresenius SE & Co. KGaA

For a detailed overview of special items and adjustments please see the reconciliation tables on pages 20-28 of the PDF document.

In Q4/19, Earnings per share1 before special items were €0.90 including an IFRS 16 effect of -€0.03. On a comparable basis, Earnings per share1,2 increased by 2% (1% in constant currency) to €0.93 (Q4/18: €0.91). Reported Earnings per share1,3 were €0.92. In FY/19, Earnings per share1 before special items were €3.37 including an IFRS 16 effect of -€0.07. On a comparable basis, earnings per share1,2 increased by 2% (0% in constant currency) to €3.44 (FY/18: €3.37). Reported Earnings per share1,3 were €3.38.

Continued investment in growth

2019 was an investment year for the Fresenius Group with a variety of initiatives to secure long-term sustainable growth. In Q4/19, spending on property, plant and equipment was €871 million corresponding to 9% of sales (Q4/18: €793 million; 9%). In FY/19, spending on property, plant and equipment was €2,463 million corresponding to 7% of sales (FY/18: €2,163 million; 6%). The 2019 investments served primarily for the modernization and expansion of dialysis clinics, production facilities as well as hospitals, and day clinics.

In Q4/19, total acquisition spending was €331 million (Q4/18: €210 million). In FY/19, total acquisition spending was €2,623 million (FY/18: €1,086 million), mainly for the acquisition of NxStage by Fresenius Medical Care.

Cash flow development

In Q4/19, Group operating cash flow was €1,286 million including an IFRS 16 effect of €211 million. On a comparable basis, Group operating cash flow was €1,075 million (Q4/18: €1,193 million) with a margin of 11.5% (Q4/18: 13.5%). Free cash flow before acquisitions and dividends adjusted for IFRS 16 was €231 million (Q4/18: €472 million). Free cash flow after acquisitions and dividends adjusted for IFRS 16 was -€122 million (Q4/18: €202 million). The IFRS 16 effect amounts to €211 million. Correspondingly, cash flow from financing activities decreased by €211 million.

In FY/19, Group operating cash flow was €4,263 million including an IFRS 16 effect of €749 million. On a comparable basis, Group operating cash flow was €3,514 million

(FY/18: €3,742 million) with a margin of 9.9% (FY/18: 11.2%). The decrease was primarily driven by the FCPA-related charge of €206 million at Fresenius Medical Care. As a consequence, and in combination with the increased investments, free cash flow before acquisitions and dividends adjusted for IFRS 16 of €1,081 million was below the previous year (FY/18: €1,665 million). Free cash flow after acquisitions and dividends adjusted for IFRS 16 was -€2,294 million (FY/18: €1,374 million). The IFRS 16 effect amounts to €749 million. Correspondingly, cash flow from financing activities decreased by €749 million.

1 Net income attributable to shareholders of Fresenius SE & Co. KGaA

2 On a comparable basis: Q4/19 and FY/19 before special items and adjusted for IFRS 16 effect; Q4/18 and FY/18 before special items and adjusted for divestitures of Care Coordination activities at FMC

3 After special items and including IFRS 16 effect

For a detailed overview of special items and adjustments please see the reconciliation tables on pages 20-28 of the PDF document.

Solid balance sheet structure

The Group’s total assets were €67,006 million including an IFRS 16 effect of €5,769 million. Adjusted for IFRS 16, Group total assets increased by 8% (7% in constant currency) to €61,237 million (Dec. 31, 2018: €56,703 million). Current assets increased by 3% (3% in constant currency) to €15,264 million (Dec. 31, 2018: €14,790 million). Non-current assets1 increased by 10% (9% in constant currency) to €45,973 million (Dec. 31, 2018: € 41,913 million).

Total shareholders’ equity was €26,580 million including an IFRS 16 effect of -€256 million. Adjusted for IFRS 16, total shareholders’ equity increased by 7% (6% in constant currency) to €26,836 million (Dec. 31, 2018: €25,008 million). The equity ratio was 39.7%. Adjusted for IFRS 16, the equity ratio was 43.8% (Dec. 31, 2018: 44.1%).

Group debt was €27,258 million including an IFRS 16 effect of €6,025 million. Adjusted for IFRS 16, Group debt increased by 12% to €21,233 million (11% in constant currency) (Dec. 31, 2018: € 18,984 million). Group net debt was €25,604 million including an IFRS 16 effect of €6,025 million. Adjusted for IFRS 16, Group net debt increased by 20% (20% in constant currency) to € 19,579 million (Dec. 31, 2018: € 16,275 million) mainly due to the acquisition of NxStage by Fresenius Medical Care.

As of December 31, 2019, the reported net debt/EBITDA ratio was 3.61x2,3,4. Adjusted for IFRS 16, the net debt/EBITDA ratio was 3.14x1,2,3,4 (Dec. 31, 2018: 2.71x2,4).

1 Adjusted for IFRS 16

2 At LTM average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures

3 Including acquisition of NxStage

4 Before special items

For a detailed overview of special items and adjustments please see the reconciliation tables on pages 20-28 of the PDF document.

Increased number of employees

As of December 31, 2019, the number of employees was 294,134 (Dec. 31, 2018: 276,750).

Business Segments

Fresenius Medical Care (Financial data according to Fresenius Medical Care press release)

Fresenius Medical Care is the world's largest provider of products and services for individuals with renal diseases. As of December 31, 2019, Fresenius Medical Care was treating 345,096 patients in 3,994 dialysis clinics. Along with its core business, the company provides related medical services in the field of Care Coordination.

• 5 % organic sales growth in Q4/19

• Investments in home dialysis and growth markets in 2019

• FY/20 outlook : Sales4 and net income5 growth6 within a mid to high single digit percentage range expected

Adjusted for IFRS 16, the contribution from the divested Care Coordination activities and NxStage, sales increased by 6% (4% in constant currency) to €4,546 million in Q4/19 (Q4/18: €4,294 million). Organic sales growth was 5%. Positive currency translation effects of 2% were mainly related to the U.S. dollar strengthening against the euro. In FY/19, sales adjusted for IFRS 16, the contributions from the divested Care Coordination activities and NxStage increased by 8% (5% in constant currency) to €17,329 million (FY/18: €16,026 million). Organic sales growth was 5%.

In Q4/19, EBIT7 increased by 3% (0% in constant currency) to €655 million (Q4/18: €636 million). The EBIT6 margin was 14.4% (Q4/18: 14.8%).

1 On an adjusted basis: before special items (transaction-related expenses, gain related to divestitures of Care Coordination activities, expenses associated with the cost optimization program), adjusted for IFRS 16 effect, excluding effects from NxStage transaction

2 Q4/18 and FY/18 before special items and adjusted for divestitures of Care Coordination activities

3 Net income attributable to shareholders of Fresenius Medical Care AG & Co. KGaA

4 FY/19 base: €17,477 million, including IFRS 16 effect

5 FY/19 base: €1,236 million, before special items, including IFRS 16 effect; FY/20: before special items

6 In constant currency

7 Q4/18 and FY/18 before special items items and after adjustments

Q4/19 and FY/19 before special items (transaction-related expenses, gain related to divestitures of Care

Coordination activities, expenses associated with the cost optimization program), adjusted for IFRS 16 effect,

excluding effects from NxStage transaction

For a detailed overview of special items and adjustments please see the reconciliation tables on pages 20-28 of the PDF document.

In FY/19, EBIT1 of €2,296 million remained at prior-year’s level (decreased by 4% in constant currency; FY/18: €2,292 million). The EBIT1 margin decreased to 13.2% (FY/18: 14.3%). Adjustments on accounts receivable in legal dispute paired with reduced patient attribution and a decreasing savings rate for ESCOs weighed on earnings. These effects were partially offset by the remeasurement effect of the fair value of the investment on Humacyte, Inc.

In Q4/19, net income1,2 increased by 3% (0% in constant currency) to €408 million (Q4/18: €395 million). In FY/19, net income1,2 increased by 2% (-2% in constant currency) to €1,369 million (FY/18: €1,341 million).

In Q4/19, operating cash flow was €597 million3 (Q4/18: €698 million) with a margin of 13.1% (Q4/18: 16.2%). In FY/19, operating cash flow was €1,947 million4 (FY/18: €2,062 million) with a margin of 11.2% (FY/18: 12.5%).

For FY/20, Fresenius Medical Care expects sales5 to grow within a mid to high single digit percentage range in constant currency. Net income2,6 is also expected to grow within a mid to high single digit percentage range in constant currency.

For further information on the IFRS 16 reconciliation of Fresenius Medical Care, please see page 18 of the PDF document.

For further information, please see Fresenius Medical Care’s press release at www.freseniusmedicalcare.com.

1 Q4/18 and FY/18 before special items and after adjustments;

Q4/19 and FY/19 before special items (transaction-related expenses, gain related to divestitures of care coordination activities, expenses associated with the cost optimization program), adjusted for IFRS 16 effect, excluding effects from NxStage transaction

2 Net income attributable to shareholders of Fresenius Medical Care AG & Co. KGaA

3 €771 million including an IFRS 16 effect of €174 million

4 €2,567 million including an IFRS 16 effect of €620 million

5 FY/19 base: €17,477 million, including IFRS 16 effect

6 FY/19 base: €1,236 million, before special items (transaction-related expenses, gain related to divestitures of care coordination activities, expenses associated with the cost optimization program), including IFRS 16 effect;

FY/20: before special items

For a detailed overview of special items and adjustments please see the reconciliation tables on pages 20-28 of the PDF document.

Fresenius Kabi

Fresenius Kabi offers intravenously administered generic drugs, clinical nutrition and infusion therapies for seriously and chronically ill patients in the hospital and outpatient environments. The company is also a leading supplier of medical devices and transfusion technology products. In the biosimilars business, Fresenius Kabi develops products with a focus on oncology and autoimmune diseases.

• 4% organic sales growth in Q4/19

• Excellent Emerging Markets growth partially offsets softer development in North America

• FY/20 outlook: organic sales3 growth of 3% to 6% and EBIT development4 of -4% to 0% expected

In Q4/19, sales of Fresenius Kabi increased by 5% (4% in constant currency) to €1,766 million (Q4/18: €1,687 million). Organic sales growth was 4%. In FY/19, sales increased by 6% (4% in constant currency) to €6,919 million (FY/18: €6,544 million). Organic sales growth was 4%. Positive currency translation effects of 2% were mainly related to the U.S. dollar strengthening against the euro.

In Q4/19, sales in North America increased by 2% (organic growth: 1%; Q4/18: €599 million) to €609 million. In FY/19, sales in North America increased by 3% (organic growth: -2%) to €2,424 million (FY/18: €2,359 million). Intensified competition on selected molecules, missing tailwinds from drug shortages as well as a shift in clinical practice towards non-opiods in the hospital-based pain management weighed on the sales development.

In Q4/19, sales in Europe grew by 2% (organic growth: 2%) to €604 million (Q4/18: €590 million). In FY/19, sales in Europe increased by 3% (organic growth: 2%) to €2,313 million

(FY/18: €2,248 million).

1 On a comparable basis: before special items and adjusted for IFRS 16 effect

2 Net income attributable to shareholders of Fresenius SE & Co. KGaA

3 FY/19 base: €6,919 million, including IFRS 16 effect

4 FY/19 base: €1,205 million; FY/19 before special items (transaction-related expenses, revaluations of biosimilars contingent purchase price liabilities), including IFRS 16 effect; FY/20: before special items, in constant currency

For a detailed overview of special items and adjustments please see the reconciliation tables on pages 20-28 of the PDF document.

In Q4/19, sales in Asia-Pacific increased by 15% (organic growth: 13%) to €385 million (Q4/18: €336 million). In FY/19, sales in Asia-Pacific increased by 16% (organic growth: 14%) to €1,506 million (FY/18: €1,300 million).

In Q4/19, sales in Latin America/Africa increased by 4% (organic growth: 10%) to €168 million (Q4/18: €162 million). In FY/19, sales in Latin America/Africa increased by 6% (organic growth: 14%) to €676 million (FY/18: €637 million).

In Q4/19, EBIT1 decreased by 1% (-1% in constant currency) to €283 million (Q4/18: €285 million) with an EBIT margin of 16.0% (Q4/18: 16.9%). In FY/19, EBIT1 increased by 5% (3% in constant currency) to €1,200 million (FY/18: €1,139 million) with an EBIT margin of 17.3% (FY/18: 17.4%).

In Q4/19, net income1,2 decreased by 2% (-3% in constant currency) to €184 million (Q4/18: €188 million). In FY/19, net income1,2 increased by 8% (5% in constant currency) to €802 million (FY/18: €742 million).

In Q4/19, operating cash flow3 was €273 million (Q4/18: €220 million) with a margin3 of 15.5% (Q4/18: 13.0%). In FY/19, operating cash flow3 was €968 million (FY/18: €1,040 million) with a margin3 of 14.0% (FY/18: 15.9%).

For FY/20, Fresenius Kabi expects organic sales growth4 of 3% to 6% and an EBIT development5 of -4% to 0% in constant currency.

For further information on the IFRS 16 reconciliation of Fresenius Kabi, please see page 18 of the PDF document of the PDF document.

1 On a comparable basis: before special items and adjusted for IFRS 16

2 Net income attributable to shareholders of Fresenius SE & Co. KGaA

3 Adjusted for IFRS 16 (operating cash flow after special items)

4 FY/19 base: €6,919 million, including IFRS 16 effect

5 FY/19 base: €1,205 million; FY/19 before special items (transaction-related expenses, revaluations of biosimilars contingent purchase price liabilities), including IFRS 16 effect; FY/20: before special items

For a detailed overview of special items and adjustments please see the reconciliation tables on pages 20-28 of the PDF document.

Fresenius Helios

Fresenius Helios is Europe's leading private hospital operator. The company comprises Helios Germany and Helios Spain (Quirónsalud). Helios Germany operates 86 hospitals, ~125 outpatient centers and 8 prevention centers. Quirónsalud operates 47 hospitals, 71 outpatient centers and around 300 occupational risk prevention centers. In addition, the company is active in Latin America with 4 hospitals and as a provider of medical diagnostics.

• Helios Germany with solid organic sales growth of 3% in Q4/19; return to EBIT growth in Q4/19

• Helios Spain with excellent organic sales growth of 7% in Q4/19; acquisitions in Latin America support further growth

• FY/20 outlook: organic sales4 growth of 3% to 6% and EBIT growth of 3% to 7% (in constant currency) expected

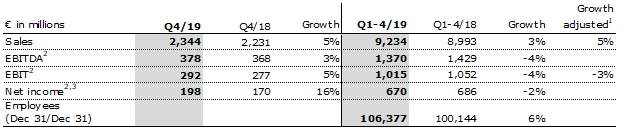

In Q4/19, sales increased by 5% (organic growth: 4%) to €2,344 million (Q4/18: €2,231 million). In FY/19, sales increased by 3% (5%1; organic growth: 5%) to €9,234 million (FY/18: €8,993 million).

In Q4/19, sales of Helios Germany increased by 3% (organic growth: 3%) to €1,475 million (Q4/18: €1,439 million). Organic sales growth was positively influenced by pricing effects and slight admissions growth. In FY/19, sales of Helios Germany decreased by 1% (increased by 3%1; organic growth: 3%) to €5,940 million (FY/18: €5,970 million). The reclassification of nursing staff funding from other income to sales also contributed to growth.

In Q4/19, sales of Helios Spain increased by 9% (organic growth: 7%) to €867 million (Q4/18: €792 million). Organic sales growth was positively influenced by admission growth and excellent execution within the existing hospital and service offerings. In FY/19, sales of Helios Spain increased by 9% (organic growth: 7%) to €3,292 million (FY/18: €3,023 million).

1 Adjusted for the post-acute care business transferred to Fresenius Vamed as of July 1, 2018

2 Adjusted for IFRS 16 effect

3 Net income attributable to shareholders of Fresenius SE & Co. KGaA

4 FY/19 base: €9,234 million, including IFRS 16 effect

5 FY/19 base: €1,025 million, including IFRS 16 effect

For a detailed overview of special items and adjustments please see the reconciliation tables on pages 20-28 of the PDF document.

In Q4/19, EBIT1 of Fresenius Helios increased by 5% to €292 million (Q4/18: €277 million) with an EBIT margin of 12.5% (Q4/18: 12.4%). In FY/19, EBIT1 decreased by 4% (-3% ) to €1,015 million (FY/18: €1,052 million) with an EBIT margin of 11.0% (FY/18: 11.7%).

In Q4/19, EBIT1 of Helios Germany increased by 4% to €143 million (Q4/18: €137 million) with an EBIT margin of 9.7% (Q4/18: 9.5%). In FY/19, EBIT1 of Helios Germany decreased by 8% (-6%2) to €576 million (FY/18: €625 million) with an EBIT margin of 9.7% (FY/18: 10.5%). Ongoing investments to counter regulatory headwinds continued to weigh on Helios Germany’s financial performance.

In Q4/19, EBIT1 of Helios Spain increased by 6% to €134 million (Q4/18: €127 million) with an EBIT margin of 15.5% (Q4/18: 16.0%). In FY/19, EBIT1 of Helios Spain increased by 5% to €434 million (FY/18: €413 million) with an EBIT margin of 13.2% (FY/18: 13.7%).

In Q4/19, net income1,3 increased by 16% to €198 million (Q4/18: €170 million). In FY/19, net income1,3 decreased by 2% to €670 million (FY/18: €686 million).

In Q4/19, operating cash flow1 increased to €212 million (Q4/18: €167 million) with a margin of 9.0% (Q4/18: 7.5%). In FY/19, operating cash flow1 increased to €683 million (FY/18: €554 million) with a margin of 7.4% (FY/18: 6.2%).

For FY/20, Fresenius Helios expects organic sales4 growth of 3% to 6% and EBIT5 growth of 3% to 7% in constant currency.

For further information on the IFRS 16 reconciliation of Fresenius Helios, please see page 18 of the PDF document.

1 Adjusted for IFRS 16 effect

2 Adjusted for the post-acute care business transferred to Fresenius Vamed as of July 1, 2018

3 Net income attributable to shareholders of Fresenius SE & Co. KGaA

4 FY/19 base: €9,234 million, including IFRS 16 effect

5 FY/19 base: €1,025 million, including IFRS 16 effect

For a detailed overview of special items and adjustments please see the reconciliation tables on pages 20-28 of the PDF document.

Fresenius Vamed

Fresenius Vamed manages projects and provides services for hospitals and other health care facilities worldwide and is a leading post-acute care provider in Central Europe. The portfolio ranges along the entire value chain: from project development, planning, and turnkey construction, via maintenance and technical management to total operational management.

• Dynamic sales growth of service business of 11% in Q4/19

• Record order backlog supports future sales development of the project business

• FY/20 outlook: organic sales4 growth of 4% to 7% and EBIT5 growth of 5% to 9% (in constant currency) expected

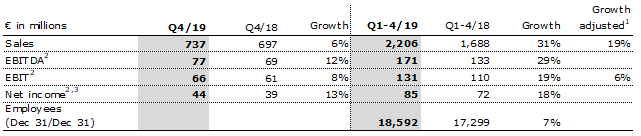

In Q4/19, sales of Fresenius Vamed increased by 6% to €737 million (Q4/18: €697 million). Organic sales growth was 4%. Acquisitions and currency translation effects contributed each 1% to growth. In FY/19, sales increased by 31% (19%1) to €2,206 million (FY/18: €1,688 million). Organic sales growth was 16%. Acquisitions contributed 14% and currency translation effects contributed 1% to growth. Both the service and the project business showed strong growth momentum.

In Q4/19, sales in the service business grew by 11% to €374 million (Q4/18: €337 million). Sales of the project business increased by 1% to €363 million (Q4/18: €360 million).

In Q4/19, EBIT2 increased by 8% to €66 million (Q4/18: €61 million) with an EBIT margin of 9.0% (Q4/18: 8.8%). In FY/19, EBIT2 increased by 19% (6%1) to €131 million (FY/18: €110 million) with an EBIT margin of 5.9% (FY/18: 6.5%).

In Q4/19, net income2,3 increased by 13% to €44 million (Q4/18: €39 million). In FY/19, net income2,3 increased by 18% to €85 million (FY/18: €72 million).

1 Adjusted for German post-acute care business acquired from Fresenius Helios as of July 1, 2018

2 Adjusted for IFRS 16 effect

3 Net income attributable to shareholders of VAMED AG

4 FY/19 base: €2,206 million, including IFRS 16 effect

5 FY/19 base: €134 million, including IFRS 16 effect

For a detailed overview of special items and adjustments please see the reconciliation tables on pages 20-28 of the PDF document.

In Q4/19, order intake was €576 million (Q4/18: €660 million). FY/19 order intake increased by 7% to €1,314 million (FY/18: €1,227 million). As of December 31, 2019, order backlog reached an all-time high at €2,865 million (December 31, 2018: €2,420 million).

In Q4/19, operating cash flow1 decreased to -€8 million (Q4/18: €108 million) with a margin of -1.1% (Q4/18: 15.5%). In FY/19, operating cash flow1 decreased to -€46 million (FY/18: €106 million) with a margin of -2.1% (FY/18: 6.3%) given timing of payments in the project business as well as increased working capital.

For FY/20, Fresenius Vamed expects organic sales2 growth of 4% to 7% and EBIT3 growth of 5% to 9% in constant currency.

For further information on the IFRS 16 reconciliation of Fresenius Vamed, please see page 18 of the PDF document.

1 Adjusted for IFRS 16 effect

2 FY/19 base: €2,206 million, including IFRS 16 effect

3 FY/19 base: €134 million, including IFRS 16 effect

For a detailed overview of special items and adjustments please see the reconciliation tables on pages 20-28 of the PDF document.

Press Conference

As part of the publication of the results for FY 2019, a press conference will be held on February 20, 2020 at 10 a.m. CET. You are cordially invited to follow the press conference in a live broadcast over the Internet at www.fresenius.com/media-calender. Following the press conference, a replay will be available on our website.

This release contains forward-looking statements that are subject to various risks and uncertainties. Future results could differ materially from those described in these forward-looking statements due to certain factors, e.g. changes in business, economic and competitive conditions, regulatory reforms, results of clinical trials, foreign exchange rate fluctuations, uncertainties in litigation or investigative proceedings, and the availability of financing. Fresenius does not undertake any responsibility to update the forward-looking statements in this release.

- Solid Q4 performance

- Full year guidance achieved

- Investments in home dialysis and growth markets as planned

- Cost optimization initiatives as planned

- 23rd dividend increase proposed

- Outlook 2020 confirmed

Rice Powell, Chief Executive Officer of Fresenius Medical Care, said: “2019 was a successful year for Fresenius Medical Care. We achieved our revenue and net income targets and are therefore proposing our 23rd consecutive dividend increase. Last year we also invested more strongly in our future growth, particularly in the area of home dialysis and in developing economies. In addition, our measures to increase efficiency and optimize our cost base are progressing according to plan. As a consequence, we expect growth to accelerate, and confirm the 2020 outlook that we issued early last year.”

2020 guidance confirmed: mid to high single digit growth rates

Fresenius Medical Care expects both revenue and net income to grow at a mid to high single digit rate in 2020. These targets are in constant currency and exclude special items3 and are based on the adjusted results 2019 including the effects of the operations of the NxStage acquisition and the IFRS 16 implementation.

Investment year 2019

The continued expansion of home dialysis in the U.S. is a key growth area for Fresenius Medical Care. As announced at the beginning of 2019, our investments focused on home training facilities, educational staff and materials along with scaling the distribution infrastructure to support both products and services. The closing of the acquisition of NxStage Medical, Inc. in February 2019 marked a milestone in our home dialysis strategy. In 2019, Fresenius Medical Care reported record growth with more than 25,000 patients being treated at home in North America.

The second major focus of investment were developing economies. In China, the world’s fastest-growing dialysis market, Fresenius Medical Care invested in expanding production capacities, research and development activities as well as in strengthening its services business, that has almost doubled with now 11 clinics. In September 2019, we launched the 4008A dialysis machine in China, laying an important foundation for the further development of the market.

In addition, Fresenius Medical Care invested EUR 91 million (EUR 83 million in North America) to sustainably improve the cost base of our clinical infrastructure. This 2019 cost optimization program is expected to be accretive to net income from the current financial year onwards. In 2019, we achieved further sustained cost improvements as part of our Global Efficiency Program (GEP II), in line with the originally anticipated contribution.

Creating shareholder value

Based on the solid results for 2019, the General Partner and the Supervisory Board will propose a new record dividend of EUR 1.20 per share, corresponding to a total payout of EUR 358 million, to the Annual General Meeting in May 2020. This proposal would result in the 23rd consecutive dividend increase.

In order to create additional shareholder value, Fresenius Medical Care launched a share buy-back program in 2019. Between March and December 2019, 8.9 million own shares were bought back at a total purchase price of EUR 600 million. The Company intends to use its residual authorization of EUR 400 million over the course of 2020.

Patients, Clinics and Employees

As of December 31, 2019, Fresenius Medical Care treated 345,096 patients in 3,994 dialysis clinics worldwide. At the end of 2019, Fresenius Medical Care had 120,659 employees (full-time equivalents) worldwide, compared to 112,658 employees as of December 31, 2018.

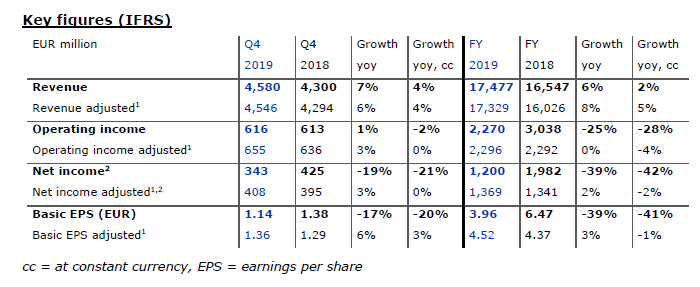

Strong organic revenue growth continued

Revenue for the fourth quarter of 2019 increased by 7% (+4% at constant currency) to EUR 4,580 million. Organic growth remained strong at 5%4. Adjusted revenue increased by 6% (+4% at constant currency) to EUR 4,546 million. For a detailed reconciliation, please refer to the table at the end of the press release.

Health Care Services revenue rose by 6% to EUR 3,607 million (+3% at constant currency), while Health Care Products revenue grew by 10% to EUR 973 million (+8% at constant currency). This includes the negative effect from a revenue recognition adjustment of EUR 86 million (FY 2019: EUR 170 million) for accounts receivable in legal dispute in North America.

Revenue for the full year 2019 rose by 6% to EUR 17,477 million (+2% at constant currency). Organic growth amounted to 5%. Adjusted revenue increased by 8% (+5% at constant currency) to EUR 17,329 million. Health Care Services revenue grew by 5% (+1% at constant currency) to EUR 13,872 million. Growth in same market treatments, contributions from acquisitions and increases in organic revenue per treatment were partly offset by decreases attributable to prior year revenue from divested activities of Sound Physicians and closed or sold clinics. Health Care Products revenue for the full year 2019 rose by 10% to EUR 3,605 million (+8% at constant currency). This increase was mainly driven by higher sales of home dialysis products as a result of the NxStage acquisition and by higher sales of dialyzers. This was partially offset by lower sales of machines as a result of changes in the accounting treatment for sale-leaseback transactions due to the IFRS 16 implementation.

In the fourth quarter operating income increased by 1% to EUR 616 million (-2% at constant currency), resulting in a margin of 13.5% (Q4 2018: 14.3%). Adjusted operating income grew by 3% to EUR 655 million (stable at constant currency), resulting in a margin of 14.4% (Q4 2018: 14.8%). The included negative effect from a revenue recognition adjustment for accounts receivable in legal dispute in North America is EUR 86 million (FY 2019: EUR 170 million). For a detailed reconciliation, please refer to the table at the end of the press release.

Operating income for the full year decreased by 25% to EUR 2,270 million (-28% at constant currency), resulting in a margin of 13.0% (FY 2018: 18.4%). The 2018 basis includes the gain from the divestiture of Care Coordination activities including Sound Physicians. On an adjusted basis, operating income remained stable at EUR 2,296 million (-4% at constant currency), resulting in a margin of 13.2% (FY 2018: 14.3%).

Net income2 for the fourth quarter decreased by 19% to EUR 343 million (-21% at constant currency). Adjusted net income2 increased by 3% to EUR 408 million (+0% at constant currency). For a detailed reconciliation, please refer to the table at the end of the press release. Basic earnings per share (EPS) decreased by 17% to EUR 1.14 (-20% at constant currency). On an adjusted basis, EPS increased by 6% to EUR 1.36 (+3% at constant currency).

For the full year, net income decreased by 39% to EUR 1,200 million (-42% at constant currency). EPS decreased by 39% to EUR 3.96 (-41% at constant currency). Here, too, the 2018 basis includes the gain from the divestiture of Care Coordination activities including Sound Physicians. On an adjusted basis, net income grew by 2% to EUR 1,369 million (-2% at constant currency). This resulted in a 3% increase in adjusted EPS to EUR 4.52 (-1% at constant currency).

Strong Cash-flow development

In the fourth quarter, Fresenius Medical Care generated EUR 771 million of operating cash flow (Q4 2018: EUR 698 million) resulting in a margin of 16.8% (Q4 2018: 16.2%). The increase was largely driven by the IFRS 16 implementation. Free cash flow (net cash used in operating activities, after capital expenditures, before acquisitions and investments) amounted to EUR 434 million (Q4 2018: EUR 397 million) resulting in a margin of 9.5% (Q4 2018: 9.2%).

In the full year, we generated operating cash flow of EUR 2,567 million resulting in a margin of 14.7% (FY 2018: EUR 2,062 million, 12.5%). The increase was mainly due to the IFRS 16 implementation. Free cash flow for the full year 2019 amounted to EUR 1,454 million resulting in a margin of 8.3% (FY 2018: EUR 1,059 million, 6.4%).

Regional developments

In North America, revenue in the fourth quarter of 2019 increased by 6% to EUR 3,174 million (+3% at constant currency, +5% organic growth). For the full year 2019, North America revenue rose by 5% to EUR 12,195 million (stable at constant currency, +4% organic).

Operating income for the fourth quarter grew by 5% to EUR 515 million (+2% at constant currency). For the full year, operating income decreased by 33% to EUR 1,794 million (-36% at constant currency). The 2018 basis includes the gain from the divestiture of Care Coordination activities including Sound Physicians.

In EMEA, revenue in the fourth quarter increased by 4% to EUR 709 million (+4% at constant currency, +3% organic). For the full year, EMEA revenue rose by 4% to EUR 2,693 million (+4% at constant currency, +4% organic).

Operating income for the fourth quarter rose by 17% to EUR 114 million (+17% at constant currency). For the full year, operating income grew by 12% to EUR 448 million (+13% at constant currency) resulting in a margin of 16.6% (FY 2018: 15.4%). This improvement was mainly driven by a reduction of a contingent consideration liability related to Xenios and a positive impact from the IFRS 16 implementation.

In Asia-Pacific, revenue in the fourth quarter 2019 grew by 10% to EUR 499 million (+7% at constant currency, +6% organic). For the full year, revenue increased by 10% to EUR 1,859 million (+7% at constant currency, +7% organic).

Operating income for the fourth quarter decreased by 13% to EUR 75 million (-14% at constant currency). The decline in margin in the fourth quarter was mainly due to investments in business growth and expenses for the cost optimization program. For the full year, operating income grew by 8% to EUR 329 million (+6% at constant currency).

Regarding the coronavirus (nCoV) outbreak the first priority is to ensure continuation of treatments for our patients and the safety of our employees. It is too early to quantify the potential impact to our Asia-Pacific operations.

In Latin America, revenue for the fourth quarter increased by 6% to EUR 193 million (+24% at constant currency, +19% organic). For the full year, Latin America revenue increased by 3% (+21% at constant currency, +17% organic) to EUR 709 million.

Operating income for the fourth quarter increased by 189% to EUR 15 million (+201% at constant currency). For the full year, operating income increased by 47% to EUR 43 million (+35% at constant currency). The improved margin was mainly due to favorable foreign currency transaction effects.

1 For a detailed reconciliation, please refer to the table at the end of the press release.

2 Net income attributable to shareholders of Fresenius Medical Care AG & Co. KGaA

3 Special items are effects that are unusual in nature and have not been foreseeable or not foreseeable in size or impact at the time of giving guidance.

4 Definition of organic growth excludes effects such as out of period adjustments or effects from IFRS 16 implementation.

Press conference

Fresenius Medical Care will hold a press conference at its headquarters in Bad Homburg, Germany to discuss the results of the fourth quarter and full year tomorrow on Thursday, February 20, 2020, at 10:00 a.m. CET / 4:00a.m. EST. The press conference will be webcasted on the company’s website www.freseniusmedicalcare.com in the “Media” section. A replay will be available shortly after the conference.

Conference call

We will also host a conference call to discuss the results of the fourth quarter tomorrow on Thursday, February 20, 2020, at 3:30 p.m. CET / 09:30 a.m. EST. Details will be available on the company’s website www.freseniusmedicalcare.com in the “Investors” section. A replay will be available shortly after the call.

Please refer to our statement of earnings included at the end of this news and to the attachments as separate PDF-files for a complete overview of the results for the fourth quarter and full year 2019. Our 20-F disclosure provides more details.

Disclaimer: This release contains forward-looking statements that are subject to various risks and uncertainties. Actual results could differ materially from those described in these forward-looking statements due to various factors, including, but not limited to, changes in business, economic and competitive conditions, legal changes, regulatory approvals, results of clinical studies, foreign exchange rate fluctuations, uncertainties in litigation or investigative proceedings, and the availability of financing. These and other risks and uncertainties are detailed in Fresenius Medical Care AG & Co. KGaA's reports filed with the U.S. Securities and Exchange Commission. Fresenius Medical Care AG & Co. KGaA does not undertake any responsibility to update the forward-looking statements in this release.

Quirónsalud, the largest private hospital group in Spain and part of Fresenius Helios, has signed an agreement to acquire Clínica de la Mujer in Bogotá, further expanding the company’s presence in Colombia’s attractive private hospital market. Following the acquisitions in Medellin and Cali in the two previous years, this is the company’s first acquisition in Colombia’s capital city.

Clínica de la Mujer is located in a prime residential area of Bogotá, Colombia’s largest city, with a population of 7.4 million. The hospital puts a special focus on gynecology, pediatrics and obstetrics, helping mothers to deliver about 3,000 babies annually, while also offering a broad range of other medical specialties and services. It has approximately 80 beds and five operating rooms, and generated sales of about €20 million in 2019.

Both parties have agreed not to disclose the terms of the acquisition. The transaction is expected to close in the second quarter of 2020, pending antitrust clearance. Fresenius expects the acquisition of Clínica de la Mujer to be accretive to Group net income in fiscal year 2020.

This release contains forward-looking statements that are subject to various risks and uncertainties. Future results could differ materially from those described in these forward-looking statements due to certain factors, e.g. changes in business, economic and competitive conditions, regulatory reforms, results of clinical trials, foreign exchange rate fluctuations, uncertainties in litigation or investigative proceedings, and the availability of financing. Fresenius does not undertake any responsibility to update the forward-looking statements in this release.

The information and documents contained on the following pages of this website are for information purposes only. These materials do neither constitute an offer nor an invitation to subscribe to or to purchase securities, nor any investment advice or service, and are not meant to serve as a basis for any kind of obligation, contractual or otherwise. Securities may not be offered or sold in the United States of America (“US”) absent registration under the US Securities Act of 1933, as amended, or an exemption from registration. The securities described on the following pages are not offered for sale in the US or to "US persons" (as defined in Regulation S under the US Securities Act of 1933, as amended).

THE FOLLOWING INFORMATION AND DOCUMENTS ARE NOT DIRECTED AT AND ARE NOT INTENDED FOR USE BY (I) PERSONS WHO ARE RESIDENTS OF OR LOCATED IN THE US, CANADA, JAPAN OR AUSTRALIA OR WHO ARE US PERSONS (AS DEFINED IN REGULATION S UNDER THE US SECURITIES ACT OF 1933, AS AMENDED), OR (II) PERSONS IN ANY OTHER JURISDICTION WHERE THE COMMUNICATION OR RECEIPT OF SUCH INFORMATION IS RESTRICTED IN SUCH A WAY THAT PROVIDES THAT SUCH PERSONS SHALL NOT RECEIVE IT. SUCH PERSONS, OR PERSONS ACTING FOR THE BENEFIT OF ANY SUCH PERSONS, ARE NOT PERMITTED TO VISIT THE FOLLOWING PAGES OF THE WEBSITE.

To visit the following parts of this website you must confirm that

(i) you are not a resident of the United States of America, Canada, Japan or Australia or a "US person" (as defined in Regulation S under the US Securities Act of 1933, as amended),

(ii) you are not a person to whom the communication of the information contained on the website is restricted,

(iii) you will not distribute any of the information and documents contained thereon to any such person, and

(iv) you are not acting for the benefit of any such person.

By clicking on the "Accept" button below, you will be deemed to have made this confirmation.

NOT FOR RELEASE, PUBLICATION OR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES OF AMERICA, AUSTRALIA, CANADA OR JAPAN.

Fresenius today successfully placed bonds with a volume of €750 million. The bonds have a maturity of 8 years and an annual coupon of 0.750%. The issue price is 99.514% and the resulting yield amounts to 0.813%.

The proceeds will be used for general corporate purposes, including refinancing of existing financial liabilities.

The bonds were drawn under the Fresenius European Medium Term Note (EMTN) Program and issued by Fresenius SE & Co. KGaA.

Fresenius has applied to the Luxembourg Stock Exchange to admit the bonds to trading on its regulated market.

This announcement does not contain or constitute an offer of, or the solicitation of an offer to buy or subscribe for, securities to any person in Australia, Canada, Japan, or the United States of America (the “United States”) or in any jurisdiction to whom or in which such offer or solicitation is unlawful. The securities referred to herein may not be offered or sold in the United States or to, or for the account or benefit of, U.S. persons, absent registration under the U.S. Securities Act of 1933, as amended (the “Securities Act”) except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the Securities Act. Subject to certain exceptions, the securities referred to herein may not be offered or sold in Australia, Canada or Japan or to, or for the account or benefit of, any national, resident or citizen of Australia, Canada or Japan. The offer and sale of the securities referred to herein has not been and will not be registered under the Securities Act or under the applicable securities laws of Australia, Canada or Japan. There will be no public offer of the securities in the United States.

This announcement is an advertisement and not a prospectus. Investors should not purchase or subscribe for any securities referred to in this announcement except on the basis of information in the prospectus to be issued by the company in connection with the offering of such securities. Copies of the prospectus will, following publication, be available free of charge from Fresenius SE & Co. KGaA at Else-Kröner Strasse 1, 61352 Bad Homburg, Germany.

This announcement has been prepared on the basis that any offer of securities in any Member State of the European Economic Area (EEA) will be made pursuant the prospectus prepared by Fresenius SE & Co. KGaA, Fresenius Finance Ireland Public Limited Company and Fresenius Finance Ireland II Public Limited Company in combination with the relevant final terms relating to such securities or pursuant to an exemption under Regulation (EU) 1129/2017 (the Prospectus Regulation) from the requirement to publish a prospectus for offers of securities. Neither Fresenius SE & Co. KGaA, Fresenius Finance Ireland Public Limited Company nor Fresenius Finance Ireland II Public Limited Company have authorized, nor do they authorize, the making of any offer of securities in circumstances in which an obligation arises for Fresenius SE & Co. KGaA, Fresenius Finance Ireland Public Limited Company and Fresenius Finance Ireland II Public Limited Company or any other person to publish or supplement a prospectus for such offer.

This announcement is directed at and/or for distribution in the United Kingdom only to (i) persons who have professional experience in matters relating to investments falling within article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the “Order”) or (ii) high net worth entities falling within article 49(2)(a) to (d) of the Order (all such persons are referred to herein as “relevant persons”). This announcement is directed only at relevant persons. Any person who is not a relevant person should not act or rely on this announcement or any of its contents. Any investment or investment activity to which this announcement relates is available only to relevant persons and will be engaged in only with relevant persons.

This announcement contains forward-looking statements that are subject to various risks and uncertainties. Future results could differ materially from those described in these forward-looking statements due to certain factors, e.g. changes in business, economic and competitive conditions, regulatory reforms, results of clinical trials, foreign exchange rate fluctuations, uncertainties in litigation or investigative proceedings, and the availability of financing. Neither Fresenius SE & Co. KGaA, Fresenius Finance Ireland Public Limited Company nor Fresenius Finance Ireland II Public Limited Company undertake any responsibility to update the forward-looking statements in this announcement.

Fresenius SE & Co. KGaA

Registered Office: Bad Homburg, Germany

Commercial Register: Amtsgericht Bad Homburg, HRB 11852

Chairman of the Supervisory Board: Dr. Gerd Krick

General Partner: Fresenius Management SE

Registered Office: Bad Homburg, Germany

Commercial Register: Amtsgericht Bad Homburg, HRB 11673

Management Board: Stephan Sturm (Chairman), Dr. Francesco De Meo, Rachel Empey, Dr. Jürgen Götz, Mats Henriksson, Rice Powell, Dr. Ernst Wastler

Chairman of the Supervisory Board: Dr. Gerd Krick